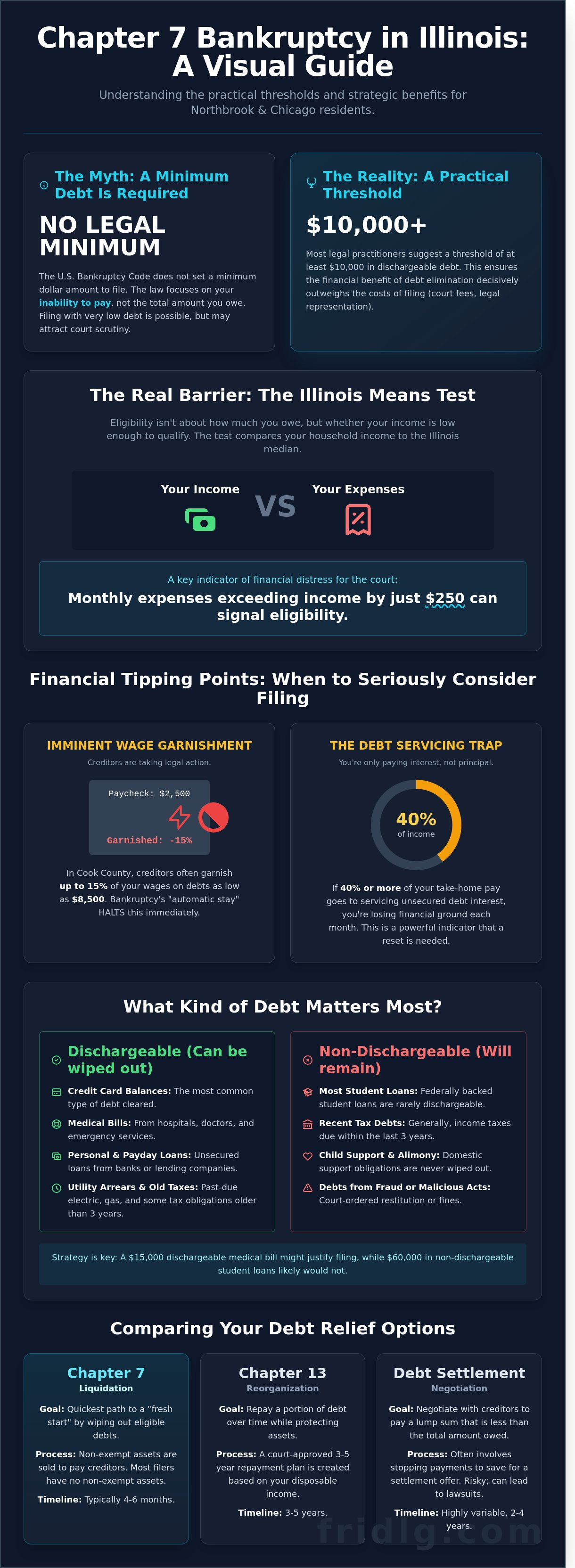

The U.S. Bankruptcy Code contains no minimum dollar amount required to seek relief, meaning the question of how much debt do u need to file chapter 7 is governed by strategic utility rather than a rigid statutory floor. You've likely been told that bankruptcy is a last resort reserved for six-figure catastrophes, yet this misconception often leads to unnecessary financial exhaustion. In Cook County, creditors frequently initiate wage garnishments of up to 15% on debts as low as $8,500, which quickly transforms a manageable balance into a direct threat to your household's stability.

We understand that you're seeking a definitive threshold to justify the legal investment. This analysis provides that clarity by examining the Illinois Means Test and the practical cost-benefit ratios specific to the Northbrook and Chicago legal landscapes. You'll discover exactly when the protection of the automatic stay outweighs the filing costs, offering a calculated path toward debt discharge. We'll outline the current 2024 filing requirements and the specific indicators that signal it's time to transition from struggling with payments to executing a structured financial recovery.

Key Takeaways

- Understand that while the U.S. Bankruptcy Code imposes no legal minimum debt floor, identifying the practical threshold where filing becomes a strategic advantage is essential for Northbrook residents.

- Evaluate your eligibility based on the Illinois Means Test, which prioritizes household income levels over total liability amounts to determine your qualification for debt liquidation.

- Learn how much debt do u need to file chapter 7 by analyzing the cost-benefit ratio between professional legal fees and the total volume of dischargeable debt to ensure a positive financial outcome.

- Compare the efficacy of Chapter 7 liquidation against Chapter 13 reorganization and debt settlement within the 2026 economic climate to select the most robust path to solvency.

- Discover the benefits of a localized legal strategy tailored to the specific procedural nuances of Cook and Lake County courts through expert professional guidance.

Is There a Legal Minimum Debt to File Chapter 7 in Illinois?

The U.S. Bankruptcy Code contains no specific dollar amount required to initiate a Chapter 7 liquidation. While many assume a $10,000 floor exists, the law focuses on your inability to pay rather than a gross total. If you're wondering how much debt do u need to file chapter 7, the answer is technically any amount. However, filing for negligible sums is a strategic error. In the Northern District of Illinois, court filing fees alone cost $338. When you include mandatory credit counseling and legal representation, the cost of filing can exceed the debt itself for small balances. Our firm analyzes your good faith because the court expects petitioners to seek relief from genuine insolvency, not to avoid minor obligations they could resolve through standard budgeting.

The Bankruptcy Code and Debt Thresholds

Under 11 U.S.C. § 109, eligibility hinges on the Means Test and residency rather than a debt ceiling. A filing with very low debt is legally possible but attracts immediate scrutiny from the U.S. Trustee. The court examines whether your petition constitutes an abuse of the system. In Cook County, judges look for a clear pattern of financial distress. If your monthly expenses exceed your income by even $250, you might qualify. The 2005 BAPCPA amendments reinforced this focus on income-to-debt ratios rather than raw numbers. It's a matter of professional strategy to ensure the benefits of a discharge outweigh the impact on your credit profile.

Why "How Much" Matters Less Than "What Kind"

The composition of your liabilities dictates the success of your filing. Dischargeable debts are the primary targets for relief. According to 2022 court statistics, medical debt and credit card balances remain the most common drivers for Chapter 7 petitions in the Northern District of Illinois. These include:

- Unsecured credit card balances

- Medical bills from Northbrook or Chicago providers

- Personal loans and payday loans

- Utility arrears and certain older tax obligations

Conversely, non-dischargeable debts offer no relief. If your $60,000 debt consists entirely of IRS tax obligations from the last 36 months or federally backed student loans, filing Chapter 7 provides little benefit. When assessing how much debt do u need to file chapter 7, we prioritize the dischargeable portion of your balance sheet. We look for a scenario where the eliminated debt improves your monthly cash flow by at least $400. A $15,000 medical bill might justify a filing, while $15,000 in non-dischargeable child support arrears would not.

When Does Filing Chapter 7 Make Financial Sense?

Determining the precise moment to initiate a Chapter 7 proceeding requires a rigorous analysis of your balance sheet rather than a simple adherence to a fixed number. While the bankruptcy code doesn't define a specific floor, many Chicago-area practitioners suggest a $10,000 threshold as the point where the benefit outweighs the administrative burden. You must weigh the total dischargeable debt against the immediate costs of legal representation and court fees to ensure the intervention is mathematically sound.

The psychological weight of insolvency often persists regardless of the specific dollar amount. If 40% or more of your monthly net income is dedicated to servicing unsecured interest without reducing the principal, you're trapped in a cycle of diminishing returns. Continuing to pay minimums represents a significant opportunity cost; those funds could instead be directed toward retirement accounts or stable investments. Deciding how much debt do u need to file chapter 7 often depends on your ability to regain financial equilibrium within a three-year window without court intervention.

Calculating the Cost of a Fresh Start in Northbrook

Strategic financial planning requires transparency in pricing. The standard Chapter 7 filing fee for 2026 is $338, which must be paid to the court regardless of attorney involvement. When you factor in mandatory credit counseling and administrative costs, filing for less than $5,000 in debt is rarely a sound strategic move. At that level, the cost of the fresh start consumes too high a percentage of the total relief. Flat-fee arrangements provide the predictability necessary for a structured recovery, allowing you to budget for the transition with precision.

The Impact of Wage Garnishment and Lawsuits

The equation changes immediately if you face an active Illinois lawsuit or a citation to discover assets. Under Illinois law, a creditor can garnish up to 25% of your disposable earnings. For a professional earning $60,000 annually, a single garnishment can result in $15,000 of lost wages over a year. In this scenario, the how much debt do u need to file chapter 7 question becomes secondary to the immediate protection offered by the Automatic Stay. This legal injunction halts all collection actions instantly, often saving more in a single month than the entire cost of the bankruptcy process. If you're facing such aggressive measures, seeking strategic legal counsel becomes a matter of asset preservation.

- Automatic Stay: Stops all lawsuits and phone calls the moment the case is filed.

- Asset Protection: Prevents the seizure of bank accounts and personal property.

- Debt Elimination: Clears credit cards, medical bills, and personal loans entirely.

The Real Barrier: The Illinois Means Test and Eligibility

The question of how much debt do u need to file chapter 7 is technically secondary to your financial capacity. The United States Bankruptcy Code doesn't mandate a minimum debt floor; instead, it imposes a ceiling on your income. This screening mechanism, known as the Means Test, determines if you're truly unable to satisfy your obligations. If the court determines you possess sufficient disposable income to pay creditors, your filing will likely be rejected or converted to a reorganization plan.

The 2026 Means Test operates through a rigorous two-part analysis. First, your average monthly income from the past six months is compared against the Illinois median. If you fall below that line, you qualify automatically. If you're above it, the second phase involves deducting standardized expenses to see if any disposable cash remains. When this calculation shows more than $165 to $275 in monthly surplus, Chapter 13 becomes the mandatory path. It's a binary system designed to prevent high-income earners from liquidating debts they could reasonably repay.

Understanding Illinois Median Income Limits

Eligibility hinges on household size and geographic location. For 2026, the projected median income for a single person in Illinois is $71,200. A household of four sees this threshold rise to approximately $122,500. While Northbrook residents face higher local costs, the court uses IRS National and Local Standards for many expense categories. High balances on credit cards or medical bills won't bypass these income requirements. You must prove that your income, not just the total figure of how much debt do u need to file chapter 7, necessitates a fresh start.

Navigating the Northern District of Illinois Court System

Northbrook residents fall under the jurisdiction of the Northern District of Illinois. All formal proceedings and meetings of creditors are processed through the Everett M. Dirksen Courthouse at 219 South Dearborn Street in Chicago. Once you file, a Chapter 7 Trustee is appointed to oversee your estate. Their primary role is to identify non-exempt assets and ensure your debt list is exhaustive. Precision is vital. You must list every creditor, from a $25,000 personal loan to a $40 utility balance. Omissions can lead to allegations of fraud or the dismissal of your case. Professional legal counsel ensures that every entry meets the court's strict transparency standards.

- Median Income Thresholds: Updated twice annually to reflect economic shifts.

- Disposable Income: Calculated after deducting mandatory costs like taxes, insurance, and secured debt payments.

- Trustee Review: A neutral party who examines your financial history for any preferential payments made to friends or family within 365 days of filing.

Comparing Chapter 7 to Other Debt Relief Options

The "do nothing" approach is a high-risk gamble in the 2026 economic environment. Under Illinois law (735 ILCS 5/13-206), the statute of limitations for written contracts is 10 years. Creditors have a decade to initiate litigation, which often leads to the garnishment of 25% of your disposable earnings. Waiting for a debt to "expire" isn't a viable strategy for those with stable employment or bank assets. Bankruptcy provides an immediate, legally binding conclusion to these liabilities that passive waiting cannot achieve.

Chapter 7 vs. Debt Settlement

Debt settlement lacks the structural integrity of a federal court order. When a creditor agrees to settle for less than the full balance, the IRS views the forgiven portion as taxable income. You'll likely receive a 1099-C form, which can create a sudden, non-dischargeable tax bill. Chapter 7 discharges are not considered taxable income. Furthermore, bankruptcy triggers the "Automatic Stay" under 11 U.S.C. § 362. This halts all lawsuits and phone calls instantly. Debt settlement companies have no such power; creditors can, and often do, sue you while you're in the middle of a settlement program.

Protecting Your Northbrook Property

Asset protection is the cornerstone of a successful filing. For the 2026 fiscal year, the Illinois Homestead Exemption protects $15,000 of equity in your primary residence, or $30,000 for married couples. If your home's value hasn't spiked beyond these limits, you'll likely keep your property. Additionally, the $4,000 "Wildcard" exemption covers personal assets like jewelry or electronics. When analyzing how much debt do u need to file chapter 7, you must view your total liabilities in the context of these exemptions. If your debt exceeds your exemptable assets, filing becomes the most logical choice for wealth preservation.

Strategic Debt Relief with Fridman Legal in Northbrook

Determining how much debt do u need to file chapter 7 depends less on a specific dollar amount and more on your unique financial ratio. Attorney O. Allan Fridman takes a forensic approach to every case; he analyzes your assets against your liabilities to ensure a Chapter 7 filing is the most efficient path forward. Based in Northbrook, the firm serves clients throughout Cook and Lake Counties. This local presence is vital. Filing in the Northern District of Illinois requires a nuanced understanding of local court trustees and specific regional exemptions that a distant firm might overlook.

Financial distress creates enough stress without the burden of hidden legal costs. Fridman Legal utilizes a transparent flat-fee structure. You'll know exactly what the representation costs before the first document is filed. This clarity allows you to budget for your fresh start without fearing billable hour surprises. The process follows a strict, logical progression:

- Initial Document Review: A deep dive into your 6-month income history and total liabilities.

- Petition Preparation: Precise drafting of all schedules to protect your exempt assets.

- The Filing: Immediate activation of the Automatic Stay to stop creditor harassment.

- Meeting of Creditors: Professional representation during the 341 meeting, typically held 30 to 45 days after filing.

While there's no statutory minimum, the question of how much debt do u need to file chapter 7 is usually answered by your inability to pay down balances within a reasonable 60-month window. If your unsecured debt exceeds your annual take-home pay, the strategic benefits of a discharge become undeniable.

Why Experience Matters in Chapter 7 Filings

Precision is mandatory in bankruptcy law. O. Allan Fridman brings 19 years of experience to the Illinois bankruptcy courts. One minor error in reporting income or valuing an asset can lead to a case dismissal or the unnecessary loss of property. The firm maintains a 100% focus on professional integrity. We ensure every line of your petition is accurate. This level of dedication provides a sense of security that only comes from veteran advocacy in the local court system.

Schedule Your Confidential Consultation

Take the first step toward solvency at our Northbrook office located on Skokie Blvd. Please bring your most recent tax returns and all current debt statements for a comprehensive review. This data allows for an immediate, accurate assessment of your eligibility. You don't have to face creditors alone. Speak with a Northbrook Bankruptcy Lawyer Today to define your strategy and regain control of your financial future.

Navigate Your Path to Financial Recovery

Determining how much debt do u need to file chapter 7 requires a focus on eligibility criteria rather than a specific dollar threshold. While Illinois law doesn't mandate a minimum debt balance, the Illinois Means Test serves as the primary structural barrier for those seeking a total discharge of unsecured liabilities. Fridman Legal applies nearly 20 years of Illinois bankruptcy experience to help you evaluate if liquidation is the most efficient instrument for your recovery. We provide these services from our professional office on Skokie Blvd in Northbrook, offering a discreet environment for strategic planning. Our firm utilizes a transparent flat-fee billing model for Chapter 7 filings, which eliminates financial ambiguity for our clients. It's essential to move beyond the stress of collection calls and toward a legally sound resolution. You don't have to manage these complex federal filings without expert guidance. Contact Fridman Legal for a Debt Relief Strategy Session to secure a fresh start and restore your professional peace of mind today.

Frequently Asked Questions

Is there a minimum debt required for Chapter 7 in Illinois?

The U.S. Bankruptcy Code does not mandate a specific minimum debt level to qualify for Chapter 7 relief. Debtors in Northbrook may file regardless of the total amount owed, provided they pass the Illinois means test. Most legal professionals suggest that filing becomes economically viable when unsecured liabilities exceed $10,000, as court fees and professional costs must be weighed against the potential discharge.

Can I file for Chapter 7 if I only have $10,000 in debt?

You can legally file for Chapter 7 with $10,000 in debt because the law establishes no lower limit for eligibility. When evaluating how much debt do u need to file chapter 7, you should consider that the $338 court filing fee and attorney fees might consume a significant portion of the potential relief. If this $10,000 consists of high-interest predatory loans, the long-term savings often justify the strategic decision to seek a discharge.

What debts cannot be discharged in an Illinois Chapter 7 bankruptcy?

Debts including child support, alimony, most student loans, and recent tax obligations are non-dischargeable under 11 U.S.C. § 523. Obligations resulting from fraud, embezzlement, or willful and malicious injury also remain the debtor's responsibility after the case closes. Approximately 25% of tax-related debts fail the "three-year rule," meaning they stay on your balance sheet regardless of the bankruptcy filing.

How much does it cost to hire a bankruptcy lawyer in Northbrook?

Hiring a bankruptcy attorney in Northbrook typically requires a flat fee ranging from $1,500 to $2,500 for a standard consumer case. This investment covers the preparation of the 50-page petition, the mandatory means test calculation, and representation at the Meeting of Creditors. Complex cases involving business assets or multiple real estate holdings may incur higher costs based on an hourly rate of $350.

Will I lose my house if I file for Chapter 7 in Cook County?

You won't lose your home if the equity is protected by the $15,000 Illinois homestead exemption. Married couples filing a joint petition in Cook County can double this protection to $30,000 under 735 ILCS 5/12-901. If your property's market value exceeds the mortgage balance and the applicable exemption by more than 10%, the trustee might liquidate the asset to pay your creditors.

How long does the Chapter 7 process take in the Northern District of Illinois?

The Chapter 7 process generally concludes within 120 to 180 days from the initial filing date. You'll attend the 341 Meeting of Creditors approximately 30 days after your attorney submits the petition to the court. Most debtors receive their final discharge order 60 days after that meeting, provided no parties in interest file a timely objection to the proceedings.

Can I file for bankruptcy again if I have done so in the past?

You can file for Chapter 7 again if 8 years have passed since the filing date of your previous successful discharge. If your prior case was a Chapter 13, the waiting period is typically reduced to 6 years under specific conditions. These statutory timelines prevent the abuse of the system while ensuring that individuals can access a fresh start after significant life changes or economic shifts.

What happens to my credit score after a Chapter 7 discharge?

Your credit score will likely experience an immediate reduction of 100 to 200 points following the filing of your petition. While the bankruptcy remains on your public record for 10 years, many debtors see their scores begin to recover within 12 months of the discharge. By maintaining a debt-to-income ratio below 30% on new accounts, you can often qualify for standard financing within 24 months.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.