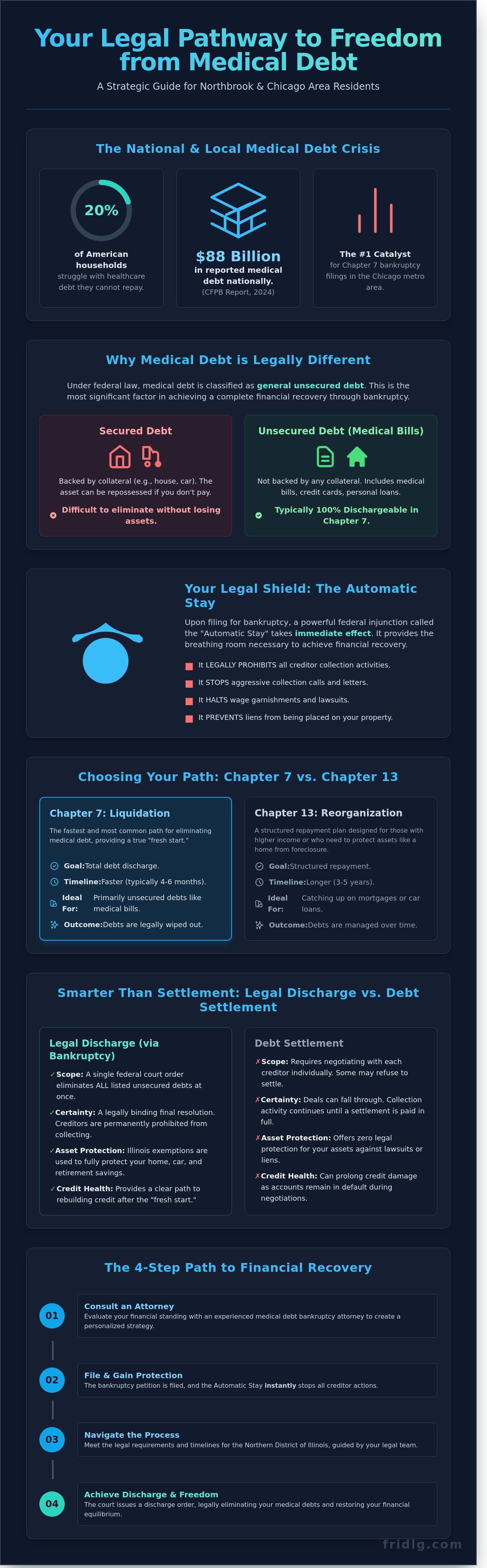

Data from the 2024 Consumer Financial Protection Bureau reports confirms that nearly 20% of American households struggle with healthcare-related liabilities that they can't realistically repay. In Northbrook and the surrounding Cook County area, these obligations often lead to aggressive collection calls and the immediate threat of wage garnishment from local providers. Consulting with experienced medical debt bankruptcy attorneys provides a structured, legal pathway to terminate these intrusive actions. It's a strategic move to restore your financial equilibrium through the professional application of federal bankruptcy protections and the preservation of your personal dignity.

You've likely felt that these mounting bills are a permanent weight that will eventually compromise your home equity or your future stability. It's understandable to feel overwhelmed when Illinois creditors prioritize their bottom line over your recovery. This guide explains how you can legally discharge medical debt while ensuring your Northbrook residential assets remain fully protected from liens. We'll examine the specific 2026 legal framework for debt elimination and provide a clear, sophisticated roadmap for your long-term financial restoration.

Key Takeaways

- Understand why medical debt is legally classified as unsecured debt and how this classification facilitates a total discharge under federal law.

- Learn how experienced medical debt bankruptcy attorneys evaluate your unique financial standing to secure a "fresh start" through the Chapter 7 process.

- Navigate the specific legal requirements and filing timelines for the Northern District of Illinois to ensure a seamless transition to financial stability.

- Analyze the critical differences between debt settlement and legal discharge to protect your assets and long-term credit health in Cook and Lake Counties.

- Discover a personalized, strategic approach to bankruptcy that prioritizes professional discretion and nearly twenty years of litigation expertise.

Navigating the Medical Debt Crisis in Northbrook and Greater Chicago

The systemic nature of healthcare costs in the United States creates a structural financial burden that even high-income households in Northbrook cannot always absorb. A 2024 report by the Consumer Financial Protection Bureau (CFPB) indicates that medical bills account for approximately $88 billion in reported debt nationally. In the Chicago metropolitan area, medical liabilities remain the primary catalyst for Chapter 7 filings, often surpassing credit card debt or mortgage defaults. Utilizing Bankruptcy in the United States as a legal framework allows individuals to address these obligations through structured discharge or reorganization. It is a precise legal mechanism designed to reset a balance sheet that has been compromised by unpredictable health crises.

Professional medical debt bankruptcy attorneys serve as the necessary bridge between financial collapse and long-term solvency. They don't just file paperwork; they provide a strategic shield against aggressive creditors who often initiate litigation within 90 days of a missed payment. By defining the process as a strategic tool rather than a last resort, families can preserve their assets while legally extinguishing unmanageable healthcare costs. This approach requires a calm, analytical assessment of one's total liability profile to ensure the filing provides the maximum possible relief under the current Illinois exemptions.

The Local Landscape: Northbrook Healthcare and Debt

Major providers such as North Shore University HealthSystem and Northwestern Medicine maintain rigorous internal collection departments. Residents in Cook and Lake Counties frequently face the reality of "underinsurance" where high deductibles, often exceeding $6,500 per individual in 2025, lead to rapid debt accumulation even for those with employer-sponsored plans. Under federal law, medical debt is classified strictly as an unsecured obligation, meaning it lacks collateral and is typically dischargeable in a Chapter 7 proceeding. This classification is vital for Northbrook residents who need to protect their home equity while liquidating medical arrears.

Understanding Your Rights as a Debtor in Illinois

The Fair Debt Collection Practices Act (FDCPA) provides specific protections for Chicago residents against harassment. A patient legally transitions to a "debtor" once a healthcare provider assigns the account to a third-party agency or files a summons in the Cook County Circuit Court. This shift changes the legal dynamic, requiring the expertise of medical debt bankruptcy attorneys to manage communications. Upon filing for bankruptcy, the "Automatic Stay" takes immediate effect; this is a powerful injunction that legally prohibits all collection activities, including phone calls, letters, and wage garnishments. It provides the breathing room necessary to finalize a comprehensive financial recovery plan without the pressure of constant creditor interference.

The Mechanics of Discharging Medical Bills Through Illinois Bankruptcy Law

The U.S. Bankruptcy Code classifies medical liabilities as general unsecured debt. This category lacks the priority status assigned to domestic support obligations or certain governmental claims. For those consulting medical debt bankruptcy attorneys, this classification is the most significant factor in achieving financial recovery. Unlike secured loans, medical bills aren't backed by collateral, making them prime candidates for total elimination. A 2014 study on medical debt and bankruptcy published by the University of Maine School of Law indicates that medical expenses are a leading driver of filings, yet the law provides a robust mechanism for their removal.

A legal discharge differs fundamentally from a settlement. While debt settlement requires negotiating with individual creditors for a partial payment, a bankruptcy discharge is a federal court order that permanently prohibits creditors from taking any collection action. In a standard Chapter 7 case in Northbrook, medical debt is typically 100% dischargeable. Success depends on precision. Every healthcare provider, diagnostic lab, and ambulance service must be listed in the official bankruptcy schedules. If a debt isn't scheduled, it might survive the bankruptcy, leaving the petitioner vulnerable to post-filing litigation.

Illinois Exemptions: Protecting Your Assets

Illinois residents don't lose everything when filing. The Illinois Homestead Exemption (735 ILCS 5/12-901) protects $15,000 of equity in a Northbrook residence, or $30,000 for married couples filing jointly. Beyond real estate, 735 ILCS 5/12-1001(e) provides specific exemptions for professionally prescribed health aids for the debtor or a dependent. The Wildcard exemption allows for an additional $4,000 in protection for any personal property. These statutes ensure that medical debt bankruptcy attorneys can shield essential assets while liquidating the underlying debt.

The Automatic Stay: Instant Relief from Collectors

The filing of a petition triggers 11 U.S.C. § 362, known as the automatic stay. This federal injunction halts all collection activity in Cook County immediately. It stops pending lawsuits, prevents medical-related wage garnishments, and freezes bank levies. Attorney O. Allan Fridman prioritizes the enforcement of this stay to ensure creditors cease all communication. If a hospital or collection agency ignores the stay, they may face sanctions in federal court. This protection allows clients to focus on a strategic legal trajectory without the pressure of constant harassment.

Comparing Chapter 7 and Chapter 13 for Healthcare-Related Debt

Selecting the appropriate bankruptcy chapter requires a rigorous analysis of your current liquidity and projected cash flow. The "Means Test" serves as the primary filter for Northbrook residents. This calculation compares your average monthly income over the preceding six months against the Illinois median income. For a household of four in 2026, this threshold often sits near $115,000; however, significant healthcare costs allow for specific deductions that may qualify higher earners for relief who would otherwise be excluded.

Medical debt bankruptcy attorneys analyze the interplay between state exemptions and federal law to maximize the discharge of healthcare liabilities. While the Illinois Medical Debt Relief Program signals a shift in state policy toward consumer protection, it doesn't offer the permanent federal injunction against creditors provided by the bankruptcy code. Determining which chapter aligns with your long-term financial stability involves assessing whether you need a total exit from debt or a structured window to protect significant assets.

Chapter 7: The Liquidation Path for Medical Relief

To qualify for Chapter 7 in the Northern District of Illinois, your disposable income must fall below the statutory limit after accounting for essential living expenses. The process is efficient and designed for speed. Most petitioners receive their formal discharge within 90 to 120 days of the initial filing date. This timeline provides a rapid transition from insolvency to financial recovery, effectively halting all collection efforts from hospital billing departments and third-party agencies.

Chapter 7 is the most common choice for medical debt because it categorizes healthcare expenses as general unsecured debt, which is typically discharged in full without any requirement to pay back a percentage of the balance.

Chapter 13: The Repayment Strategy

Chapter 13 functions as a structured reorganization rather than a total liquidation. It's designed for Northbrook professionals or business owners who possess non-exempt assets, such as high-value real estate or equity in a private practice, that they wish to shield from creditors. Under a 3-to-5-year court-mandated plan, medical bills are prioritized alongside other unsecured debts. Medical debt bankruptcy attorneys use this chapter to create a manageable payment environment while the client continues to earn a high income.

- Repayment plans are calculated based on "disposable income" after necessary medical maintenance and insurance costs are deducted.

- It protects non-exempt property that would otherwise be sold in a Chapter 7 liquidation.

- Strategic filing stops aggressive litigation and wage garnishments from local healthcare networks like NorthShore or Northwestern Medicine.

- High-earners can use this path to consolidate various liabilities into one predictable monthly payment.

For Northbrook business owners, Chapter 13 offers a strategic advantage by allowing the business to remain operational while the individual reorganizes their personal liability for medical costs. This approach ensures that a temporary health crisis doesn't lead to the permanent dissolution of a professional practice or commercial enterprise.

The Legal Timeline: Filing for Medical Debt Relief in Cook and Lake Counties

The path to financial restructuring via Chapter 7 or Chapter 13 begins with a forensic examination of the petitioner's medical ledger. Skilled medical debt bankruptcy attorneys analyze every line item to ensure all qualifying unsecured obligations are captured. Following this audit, the formal petition is filed within the U.S. Bankruptcy Court for the Northern District of Illinois. This filing triggers the automatic stay; it immediately halts collection actions from Northbrook healthcare providers and Chicago-based hospital systems. Creditors can't legally contact you or garnish wages once the court issues this stay.

Pre-Filing Requirements and Credit Counseling

Filers must complete a credit counseling course from an approved agency within 180 days before filing. This federal mandate ensures participants understand the alternatives to liquidation. Document collection remains the most intensive phase. It requires tax returns from the previous two years, six months of income stubs, and comprehensive medical billing statements. Fridman Legal utilizes a centralized digital portal to aggregate these records. This system reduces the administrative burden on busy professionals by approximately 40 percent compared to traditional manual methods.

The Role of the Bankruptcy Trustee

The United States Trustee Program appoints a trustee to oversee the case. Their primary objective is to identify non-exempt assets that could be liquidated to satisfy creditors. In Cook County, trustees scrutinize transfers made within the 90 days preceding the filing. Expert representation is vital during the Section 341 Meeting of Creditors. At this stage, the trustee conducts a recorded examination of the debtor under oath. Common pitfalls in Northbrook filings often involve the undervaluation of personal property or failure to disclose secondary income streams. These errors can lead to case dismissal or allegations of fraud.

The process culminates in the discharge order. This document is typically issued 60 to 90 days after the 341 Meeting. It's the legal instrument that permanently prohibits creditors from pursuing the discharged medical debts. Post-discharge, the focus shifts to credit restoration and strategic financial management. Most filers see a stabilized credit score within 12 months of their discharge date if they follow a disciplined recovery plan. If you require a structured approach to liability management, consult with our strategic advisory team to begin your financial recovery.

Strategic Debt Solutions: Why Northbrook Residents Choose Fridman Legal

Northbrook residents facing escalating healthcare costs require more than a standard filing. They need a representative who understands the nuances of the local judicial landscape. Fridman Legal brings nearly 20 years of bankruptcy and litigation experience to the Chicago suburbs. This tenure ensures that every strategic decision rests on a foundation of established case law and procedural precision. We don't rely on generic templates; we build frameworks designed to withstand the scrutiny of trustees and creditors alike.

The firm's advocacy prioritizes client discretion and professional distance. We understand that medical insolvency often intersects with other complex legal areas. By integrating real estate expertise and civil litigation knowledge, we provide a holistic defense of your assets. This multidimensional approach is essential for Northbrook homeowners and professionals who must protect their equity while addressing unsustainable liabilities. Our strategy focuses on long-term stability rather than temporary relief.

A Boutique Approach to Complex Debt

Large-scale firms often treat insolvency as a volume business, prioritizing turnover over meticulous detail. Fridman Legal operates as a boutique practice where clients maintain direct access to principal attorney O. Allan Fridman. This structure eliminates the risk of a case being delegated to inexperienced associates or administrative staff. Professional integrity remains our primary metric for success, ensuring that every filing is technically perfect and strategically sound.

Our medical debt bankruptcy attorneys analyze how a filing impacts your broader financial portfolio. We identify potential risks to non-exempt assets and develop preemptive solutions. This level of personalized attention is rarely found in high-volume bankruptcy mills. We focus on the following core pillars:

- Direct accountability from senior counsel throughout the process.

- Rigorous analysis of creditor claims to identify inaccuracies or violations.

- Protection of professional reputations through discreet, efficient legal action.

- Integration of 20 years of litigation experience to handle contested matters.

Scheduling Your Strategic Consultation

The path toward financial recovery begins with a rigorous evaluation of your current liabilities. During a consultation at our Northbrook office, we assess your eligibility for Chapter 7 or Chapter 13 relief based on current 2026 standards. To ensure a productive session, please provide the following documentation:

- Comprehensive medical billing statements from the last 24 months.

- Federal and state tax returns for the previous two years.

- Proof of current income and recurring household expenses.

- Documentation regarding any pending lawsuits or collection notices.

We don't just file paperwork; we engineer a transition toward financial equilibrium. Our team identifies the most efficient legal mechanisms to discharge or restructure your obligations while maintaining your privacy. You can schedule a confidential medical debt consultation with Fridman Legal to review your options under Illinois statutes. Taking this step replaces uncertainty with a structured, legally sound strategy for debt resolution in the Chicago suburbs.

Navigate Your Path to Financial Restoration

Navigating the 2026 healthcare landscape requires more than just basic paperwork; it demands a calculated approach to debt restructuring. Whether you're pursuing a complete discharge under Chapter 7 or a structured repayment through Chapter 13, the legal timeline in Cook and Lake counties remains rigid. Success hinges on precise filing and an intimate understanding of specific Illinois exemptions. Missteps in the documentation process can lead to dismissed cases or unprotected assets, making professional oversight a necessity rather than an option.

Fridman Legal provides this level of strategic guidance from our professional suites on Skokie Blvd in the heart of Northbrook. Our principal attorney leverages nearly 20 years of experience to guide clients through complex Chapter 7, 11, and 13 proceedings with surgical precision. When you engage our firm, you aren't just hiring medical debt bankruptcy attorneys; you're securing a partnership focused on professional integrity and long-term financial stability. We manage the intricate mechanics of federal law so you can regain control of your personal narrative. It's time to replace uncertainty with a definitive, legally sound strategy.

Secure your financial future—contact Fridman Legal for a strategic consultation today.

Your path to a debt-free future is achievable with the right counsel by your side.

Frequently Asked Questions

Can medical debt be wiped out in bankruptcy in Illinois?

Medical debt is categorized as general unsecured debt and is fully dischargeable under Chapter 7 or Chapter 13 of the U.S. Bankruptcy Code. In Illinois, debtors who pass the means test can eliminate 100% of their qualifying healthcare obligations. This legal mechanism provides a strategic exit from insolvency. Our medical debt bankruptcy attorneys ensure that every healthcare provider is properly listed in the petition to prevent post-filing collection attempts.

Will I lose my Northbrook home if I file for bankruptcy due to medical bills?

You likely won't lose your Northbrook residence due to the Illinois homestead exemption. Current state law protects up to $15,000 of equity for a single filer and $30,000 for a married couple. If your home equity falls below these specific thresholds, the property remains exempt from liquidation. This protection allows for a structured financial recovery without sacrificing your primary asset or family stability during the legal process.

How much does a medical debt bankruptcy attorney cost in Chicago?

Professional fees for a Chapter 7 filing in Chicago typically range from $1,500 to $3,500, depending on the complexity of your asset structure. Additionally, the U.S. Bankruptcy Court for the Northern District of Illinois requires a $338 filing fee. These costs represent a strategic investment in long-term solvency. We provide transparent fee structures that reflect the precision and specialized expertise required for high-stakes financial restructuring and debt elimination.

What happens to my credit score after discharging medical debt?

Your credit score will experience an immediate decline of 100 to 200 points following the discharge. A Chapter 7 filing remains on your credit report for 10 years, while Chapter 13 is removed after 7 years. However, eliminating a debt-to-income ratio of 40% or higher often facilitates a faster recovery than struggling with delinquent accounts. Many filers see significant score improvements within 12 to 24 months of their final decree.

Can I file for bankruptcy if I am still receiving medical treatment?

You can file while receiving treatment, but timing is a critical strategic consideration. Debts incurred after the filing date aren't included in the discharge, so filing too early might leave you liable for future surgical or rehabilitative costs. Our medical debt bankruptcy attorneys analyze your treatment timeline to ensure the petition captures the maximum amount of liability. You must also complete a credit counseling course within 180 days before submitting your petition.

Is there a limit to how much medical debt I can discharge in Chapter 7?

There's no statutory limit on the amount of medical debt you can discharge in a Chapter 7 liquidation. Whether the liability is $50,000 or $500,000, the court treats it as an unsecured claim. In contrast, Chapter 13 filings are subject to a total debt limit of approximately $2.75 million under the Bankruptcy Threshold Adjustment and Technical Corrections Act. This lack of a ceiling makes Chapter 7 a powerful tool for catastrophic health events.

How long does the medical debt bankruptcy process take in Cook County?

A standard Chapter 7 case in Cook County typically concludes within 4 to 6 months. The process begins with the initial filing and includes a mandatory 341 meeting of creditors, usually scheduled within 30 days. Creditors then have a 60-day window to object to the discharge. Once this period closes, the court issues a final order. This predictable timeline allows for an efficient transition toward a stabilized financial position and professional peace of mind.

Can a hospital sue me after I have filed for bankruptcy?

Hospitals and collection agencies are legally prohibited from pursuing litigation once the automatic stay is in effect. Under Section 362 of the Bankruptcy Code, all collection activity must cease immediately upon filing. If a healthcare provider initiates a lawsuit or continues garnishment after notification, they face sanctions from the federal court. This protection ensures that your focus remains on recovery rather than managing aggressive litigation from medical institutions or third-party collectors.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.