The cheapest option for filing for bankruptcy is often the most expensive mistake you can make. When you're already facing harassing calls from creditors and the constant fear of losing your home, the last thing you need is a legal "bargain" that puts your assets at risk. Understanding the true bankruptcy attorney chicago Suburbs cost isn't just about looking at a price tag; it's about protecting your equity and your future. It's completely normal to feel hesitant about spending money when you're trying to get out of debt, but gaining clarity is the first step toward reclaiming your financial freedom.

You likely want to know exactly how much cash you'll need to stop wage garnishments and finally wipe out those medical bills or credit card balances. We understand that the confusion between Chapter 7 and Chapter 13 costs can feel like another burden on an already full plate. That's why we've put together this guide to give you a clear, honest breakdown of the financial commitment involved. We'll walk through the mandatory court filing fees, explain the recent 2026 Illinois exemption updates that help protect your car and home, and show you how professional representation works to secure your long-term stability.

Key Takeaways

- Learn why mandatory court filing fees in the Northern District of Illinois are non-negotiable and how to budget for the required credit counseling courses.

- Get a realistic look at the bankruptcy attorney chicago Suburbs cost and why a transparent flat-fee model is usually the best way to avoid hidden surprises.

- Compare the upfront costs of a Chapter 7 "Fresh Start" against the long-term payment structure of a Chapter 13 plan to see which fits your current budget.

- Understand the hidden risks of choosing "discount" legal services, which often lead to paperwork errors that could cost you your home or car.

- Discover how to use the 2026 Illinois exemption increases to protect your property while finally stopping wage garnishments and creditor calls.

What Does a Bankruptcy Attorney in the Chicago Suburbs Actually Cost?

When you start searching for a bankruptcy attorney chicago Suburbs cost, you'll likely notice that most firms in 2026 operate within a fairly specific range. While the financial pressure of debt makes every dollar feel significant, it's helpful to view these costs as an investment in protecting your remaining assets. In the Chicago suburbs, particularly for those filing in Northbrook or elsewhere in Lake and Cook Counties, most legal professionals prefer a flat-fee model for Chapter 7 cases. This approach is popular because it offers you a predictable ceiling on your expenses. You won't have to worry about a ticking clock every time you call with a question regarding your car or your home's equity.

The total amount you pay is rarely just one single number. It's actually a combination of several different requirements. It's helpful to distinguish between the money that goes to your lawyer for their expertise and the money that goes directly to the federal government to process your case. Understanding how attorney's fees are structured in the Northern District of Illinois will help you spot "discount" offers that might actually leave out essential services or court costs.

The Components of Your Total Bill

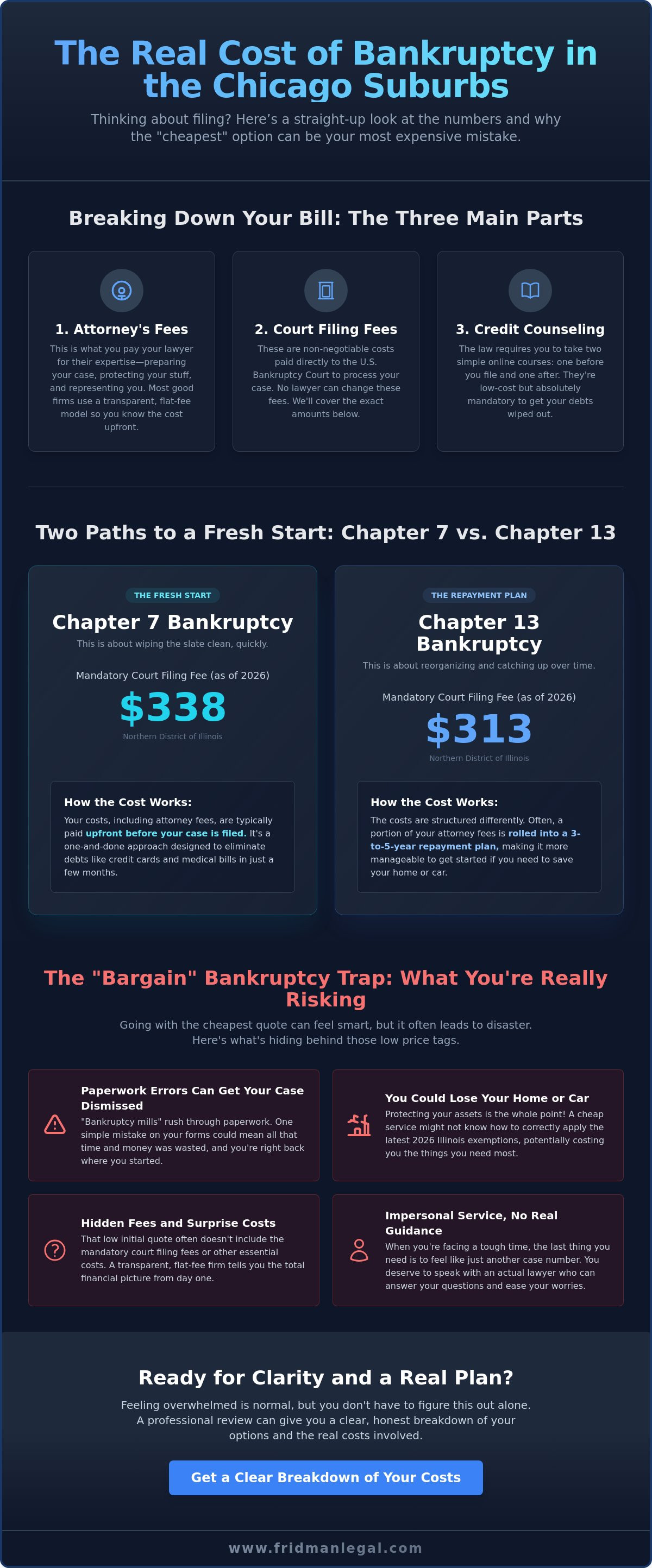

Your total financial commitment consists of three main parts. First, there are the mandatory court filing fees set by the U.S. Bankruptcy Court. As of 2026, the national filing fee for a Chapter 7 is $338, while a Chapter 13 is $313. These are non-negotiable and must be paid to the clerk. Second, you have the legal representation fees. This covers the work of preparing your petition, attending the 341 meeting of creditors, and ensuring your exemptions are applied correctly. Finally, there are small fees for the two mandatory credit counseling and financial management courses required by federal law before your debts can be discharged.

Why Pricing Varies Between Firms

You'll find that a bankruptcy attorney chicago Suburbs cost can fluctuate based on the complexity of your situation. A person with a single house and standard credit card debt will likely pay less than a small business owner with complex assets and multiple properties. Choosing the cheapest possible option often leads to "bankruptcy mills" where you rarely speak to an actual lawyer. This is risky because a simple mistake in your paperwork can lead to a dismissed case or, worse, the loss of property that could have been protected under the new 2026 Illinois exemption limits. High-quality bankruptcy representation focuses on precision and asset protection rather than just filing the forms as quickly as possible.

Breaking Down the Mandatory Costs of Filing in Illinois

When you sit down to calculate the bankruptcy attorney chicago Suburbs cost, it's easy to focus solely on the legal fee. However, filing for bankruptcy involves several "hard costs" that aren't paid to your lawyer at all. These are external expenses mandated by federal law and the court system. Even if you were to file without professional help, you would still be responsible for these specific charges. Understanding these numbers upfront prevents the frustration of seeing unexpected line items on your final bill. It's best to think of your total cost as two separate buckets: the professional fee for your legal protection and the administrative fees required to move your case through the system.

Transparency is key here. Some firms might quote a lower starting rate but then add on these mandatory costs later. You should always ask if your initial quote includes the court filing fee and the administrative expenses for pulling your records. If you're feeling overwhelmed by these numbers, reaching out for a professional case review can help clarify exactly what your specific situation will require.

Court Filing Fees: The Non-Negotiables

The U.S. Bankruptcy Court for the Northern District of Illinois has a set price list that applies to everyone. For a Chapter 7 case in 2026, the filing fee is $338. If you're filing a Chapter 13, the fee is slightly lower at $313. You can verify these amounts by checking the Official Bankruptcy Filing Fees in Illinois schedule. These fees are usually paid via money order or through your attorney's trust account. If your income is below 150% of the Illinois poverty guidelines, you may be eligible for a fee waiver through an "In Forma Pauperis" application, though these are typically reserved for those in extreme financial hardship.

The "Hidden" Extras You Need to Know

Beyond the court's fee, there are a few other small but mandatory expenses. Federal law requires you to complete two educational courses. The first is a credit counseling session that must happen before you file. The second is a financial management course that you'll take after your case is in the system. Most of these courses cost between $15 and $50. Additionally, your attorney will need to pull your official credit reports and potentially your tax transcripts from the IRS. While some firms include these in their bankruptcy attorney chicago Suburbs cost, others pass these small administrative charges directly to the client. It's a small detail, but knowing whether your firm uses specialized software to track your debts can make a big difference in how smoothly your paperwork is handled.

Chapter 7 vs. Chapter 13: Comparing the Financial Commitment

Choosing between Chapter 7 and Chapter 13 is the single most significant factor in determining your total bankruptcy attorney chicago Suburbs cost. It isn't just about which option has a lower price tag today. It's about which legal structure aligns with your income and your long term goals for your property. In Illinois, the "Means Test" acts as the gatekeeper for these two paths. As of April 1, 2026, if you're a single person earning less than $73,180 annually, you'll likely qualify for Chapter 7. If your income exceeds these thresholds, or if you're trying to save a home in Northbrook from foreclosure, Chapter 13 becomes the strategic choice. Each path handles legal fees differently, which changes how you'll need to manage your cash flow during the process.

For suburban filers, the logistics can also vary. While most clients in the Northbrook area will have their cases heard in the Eastern Division of the Northern District of Illinois in downtown Chicago, those further west may fall under the Western Division in Rockford. Understanding these jurisdictional nuances is part of what you're paying for when you hire a local expert. It ensures your paperwork is filed in the correct division from day one, preventing costly delays or dismissals.

Chapter 7: Quick Relief, Upfront Costs

Often called a "Fresh Start" bankruptcy, Chapter 7 is designed to wipe out unsecured debts like credit cards and medical bills in just a few months. Because the case moves so quickly, most attorneys require their fees to be paid in full before the petition is officially filed with the court. This is because any unpaid legal fees could technically be discharged along with your other debts once the case starts. While this requires a larger upfront investment, it offers the highest "ROI" for many people because it eliminates debt almost entirely without a multi-year payment plan. If you can't pay the full amount at once, many firms allow you to pay in installments while they prepare your paperwork, though they won't "push the button" on the filing until the balance is settled.

Chapter 13: Long-term Protection, Deferred Fees

Chapter 13 works very differently and is often the preferred route for homeowners who have fallen behind on mortgage payments. Instead of an immediate discharge, you enter a three to five year repayment plan. The financial benefit here is that a large portion of your Chapter 13 legal fees can often be rolled into your monthly plan payments. This means your initial "out of pocket" cost to get the case filed is usually much lower than in a Chapter 7. The court uses a "no-look" fee schedule in the Chicago area, which sets a standard, reasonable fee for these cases. This structure provides a massive advantage for families trying to stop a foreclosure or protect a vehicle, as it allows them to get legal protection immediately while spreading the cost of that protection over several years.

The Danger of "Cheap" Bankruptcy Lawyers: What’s the Catch?

It is entirely natural to look for the lowest possible quote when you are already struggling with debt. You might see ads online for legal services that seem significantly lower than the average bankruptcy attorney chicago Suburbs cost. However, in the legal world, a "bargain" often comes with hidden risks that can jeopardize your financial recovery. Most low-cost firms operate as "bankruptcy mills." These businesses rely on high volume and standardized templates rather than personalized strategy. While a template might work for a very simple case, it rarely accounts for the nuances of suburban property ownership or complex financial histories.

The true cost of a cheap lawyer often reveals itself when a case is dismissed due to a missed deadline or a simple paperwork error. If your case is dismissed, you lose the protection of the automatic stay. This means creditors can immediately resume harassing calls, and wage garnishments can start again. You may even be barred from filing again for several months. When you consider the bankruptcy attorney chicago Suburbs cost, you must factor in the value of the assets you are trying to protect. Saving a few hundred dollars on a fee is a poor trade if it results in the loss of property that could have been saved with a more diligent approach.

Asset Protection is Not a DIY Project

Protecting your property requires a deep understanding of the 2026 Illinois exemption updates. For example, as of January 1, 2026, you can protect up to $50,000 in equity in your primary residence, or $100,000 for a married couple. You also have a $3,600 motor vehicle exemption and a $4,000 wildcard exemption. These protections are not automatic. They must be specifically claimed and defended on your bankruptcy schedules. If a lawyer miscalculates the value of your household goods or fails to apply the wildcard exemption correctly, the Trustee has the legal right to seize and sell those items to pay your creditors. Local knowledge of the trustees in the Northern District of Illinois is vital because some are far more aggressive than others regarding property valuations.

Communication and Peace of Mind

One of the most common complaints about discount firms is the lack of direct access to a lawyer. You might find yourself exclusively speaking with paralegals, only to have a "coverage attorney" you've never met show up at your Meeting of Creditors. This lack of continuity can lead to conflicting information and increased anxiety during an already stressful time. Learn more about our personalized bankruptcy services to see the difference that 20 years of experience and direct attorney communication can make. You deserve to have the person who prepared your file actually standing next to you when you face the Trustee. If you want to ensure your filing is handled with the precision it requires, you can reach out to our team for a professional evaluation of your case.

How Fridman Legal Handles Bankruptcy Fees and Filings

We understand that the decision to file for bankruptcy is often the result of months, or even years, of intense financial pressure. This is why we prioritize flat-fee transparency for every client we serve. When you're trying to figure out the bankruptcy attorney chicago Suburbs cost, the last thing you need is a vague estimate that grows once the process starts. We provide a clear, upfront breakdown of our fees so you can plan your recovery with confidence. Our goal is to replace your current financial uncertainty with a structured, professional path forward that protects your long-term interests.

With over 20 years of experience, O. Allan Fridman provides the kind of strategic guidance that "bankruptcy mills" simply can't offer. We don't just file forms; we build a shield around your assets. Once you retain our firm, you can immediately direct those harassing creditor calls to our office. We take over the heavy lifting of the legal process, from the complex asset valuations to the mandatory court appearances in the Northern District of Illinois. This professional buffer allows you to stop worrying about the phone ringing and start focusing on your future.

A Human-Centric Approach to Debt Relief

We believe that financial distress is a legal challenge to be solved, not a personal failure. Our local presence in Northbrook and across the Chicago suburbs means we understand the specific property values and trustee expectations in our community. We treat every person who walks through our doors with the professional respect they deserve, regardless of their current balance sheet. If you're looking for more specific details on the process itself, you can read our Chapter 7 Bankruptcy in Northbrook, IL: A Strategic Guide for a deeper look at the logistics of filing.

Ready for a Fresh Start?

Taking the first step is often the hardest part of the journey. To get an accurate quote for your bankruptcy attorney chicago Suburbs cost, it's helpful to have your recent pay stubs, tax returns, and a general list of your debts ready for review. This allows us to determine whether a Chapter 7 discharge or a Chapter 13 repayment plan is the most effective tool for your situation. Remember that the "automatic stay" goes into effect the moment we file your petition, which can stop wage garnishments and foreclosure proceedings in their tracks. If you're ready to explore your options and regain control of your finances, contact us today for a confidential consultation to discuss your specific needs.

Take the First Step Toward Financial Stability

Filing for bankruptcy is a significant legal move, but it shouldn't be a confusing one. We've explored how mandatory court fees and legal representation costs work together, and why the lowest bankruptcy attorney chicago Suburbs cost isn't always the best value if it leaves your home or car unprotected. Whether you qualify for a Chapter 7 discharge or need the long-term protection of a Chapter 13 plan, understanding the total financial commitment is the first step toward reclaiming your peace of mind. Gaining this clarity allows you to stop the cycle of debt and start building a stable foundation.

At Fridman Legal, we're committed to complete transparency. With nearly 20 years of local legal experience, O. Allan Fridman provides the personalized attention you need to navigate the 2026 Illinois exemption updates. Our flat-fee pricing models are designed to eliminate guesswork, allowing you to focus on your recovery rather than billable hours. You deserve a partner who prioritizes your equity and your future. Get a Transparent Quote for Your Fresh Start today. Better days are ahead, and we're here to help you reach them.

Frequently Asked Questions

Is there a "low cost" bankruptcy option for Chicago residents?

You'll often see advertisements for very low rates, but these typically come from "bankruptcy mills" that rely on high volume rather than personal attention. While the initial bankruptcy attorney chicago Suburbs cost might look like a bargain, these services often skip the deep analysis needed to protect your assets under the 2026 Illinois exemption rules. Saving a few hundred dollars on fees isn't worth it if you end up losing property that a more experienced lawyer could have saved.

Can I pay my bankruptcy attorney in installments?

Yes, most firms in the Chicago suburbs allow you to pay your legal fees in installments while they prepare your paperwork. For a Chapter 7 case, the full fee is usually required before the attorney "pushes the button" to file your case with the court. This is because any unpaid legal fees could technically be wiped out in the bankruptcy itself. In a Chapter 13 case, you can often pay a large portion of the legal fees through your monthly repayment plan over three to five years.

Do I have to pay the court filing fee all at once?

The court generally expects the filing fee at the time of your petition, but you can apply to pay it in up to four installments. As of May 2026, the fee is $338 for Chapter 7 and $313 for Chapter 13. If your household income is below 150% of the Illinois poverty guidelines, you can also apply for a fee waiver, though the Northern District of Illinois judges review these requests with a high level of scrutiny.

What happens if I file for bankruptcy without an attorney to save money?

Filing "pro se" or without a lawyer is extremely risky and often ends in a dismissed case. You're held to the same standards as a professional attorney, meaning any missed deadline or incorrectly valued asset can lead to the loss of your property. Trustees are very thorough, and if you don't correctly apply the $4,000 wildcard exemption or the $50,000 homestead exemption, you could lose your belongings or even your home equity to pay back creditors.

Are there different costs for filing in Cook County vs. Lake County?

The mandatory court filing fees are identical regardless of which county you live in because bankruptcy is handled in federal court. Whether you're in Northbrook or downtown Chicago, you're filing in the Northern District of Illinois. While the bankruptcy attorney chicago Suburbs cost might fluctuate slightly between different law firms based on their local overhead, the $338 and $313 court fees remain the same for everyone in the region.

How much debt do I need to have to make the cost of a lawyer worth it?

There isn't a magic number, but the decision usually depends on how the debt is affecting your life. If you're facing a wage garnishment, a frozen bank account, or a pending foreclosure, the cost of a lawyer is an investment in stopping those actions immediately. Most people find that if their unsecured debt, like medical bills or credit cards, is significantly higher than the cost of filing, the "return on investment" for their future peace of mind is well worth it.

Does the cost of bankruptcy include my credit counseling certificates?

Most attorneys treat credit counseling as a separate out of pocket expense that you pay directly to the provider. These mandatory courses usually cost between $15 and $50 each. You'll need to complete one session before you file and a second financial management course before you receive your final discharge. It's a good idea to ask your lawyer during your first meeting if these administrative costs are bundled into their flat fee or if you'll need to pay them separately.

Will I have to pay more if my case goes to an adversary proceeding?

Yes, an adversary proceeding is essentially a separate lawsuit within your bankruptcy case and almost always requires an additional fee. These situations are relatively rare and usually happen if a creditor claims you committed fraud or if there's a serious dispute over a specific debt. Because these proceedings involve litigation and court hearings, they aren't covered by the standard flat-fee agreements used for typical Chapter 7 or Chapter 13 filings.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.