The common assumption that debt relief requires the forfeiture of your primary residence is a fundamental misunderstanding of federal and state statutes. In reality, the strategic application of the Illinois Code of Civil Procedure often allows Northbrook homeowners to maintain their property while restructuring or discharging their liabilities. If you're currently facing financial instability, the primary question on your mind is likely: can you file bankruptcy and keep your house? Under current Illinois law, specifically 735 ILCS 5/12-901, individuals may exempt up to $15,000 of equity in their primary residence, a figure that doubles to $30,000 for married couples filing jointly.

You've worked hard to establish your life in the Northbrook area, and the prospect of losing that foundation to a lender is understandably distressing. We'll demonstrate how these exemptions and the automatic stay provision work in tandem to halt foreclosure proceedings immediately. This guide details the precise legal pathways available in 2026 to eliminate unsecured debt while preserving your home's title. We'll analyze the structural benefits of Chapter 13 repayment plans versus Chapter 7 asset protection to ensure your financial future remains stable and predictable.

Key Takeaways

- Evaluate how the 2026 Illinois homestead exemption thresholds provide a robust legal shield for your primary residence's equity.

- Gain clarity on the essential question—can you file bankruptcy and keep your house—by examining the specific criteria for asset protection in Northbrook.

- Compare Chapter 7 and Chapter 13 strategies to determine which filing method optimally balances debt elimination with property retention.

- Address mortgage delinquency and the strategic implications of reaffirmation agreements to secure your home’s future within the bankruptcy estate.

- Recognize the strategic advantage of local legal counsel when navigating the unique procedural requirements of the Cook County court system.

Understanding Your Rights: Can You File Bankruptcy and Keep Your House in Illinois?

The prospect of losing a primary residence often deters Northbrook homeowners from seeking the debt relief they require. To address the most pressing concern: yes, you can you file bankruptcy and keep your house in Illinois through the strategic application of statutory exemptions or structured repayment schedules. Success depends on the specific chapter filed and the amount of equity held within the property. While the law is complex, it's designed to provide a fresh start rather than leave individuals destitute.

When a petition is submitted to the U.S. Bankruptcy Court for the Northern District of Illinois, a legal entity known as the "bankruptcy estate" is created. This estate technically includes all your assets. However, Illinois law provides specific protections that allow you to "exempt" certain property from this estate. For many Northbrook residents, the Homestead Exemption is the most vital tool in this process. Unlike some states that allow for federal exemptions, Illinois requires residents to use state-specific limits to protect their equity.

It's important to distinguish between a primary residence and investment properties. Illinois law prioritizes the preservation of a debtor's home. While your house in Northbrook may be protected, secondary properties or rental units in Cook County are treated as non-essential assets. These are much more likely to be liquidated to satisfy creditors unless a Chapter 13 plan is utilized to pay back the arrears over a three to five-year period.

The Definition of Home Equity in Bankruptcy

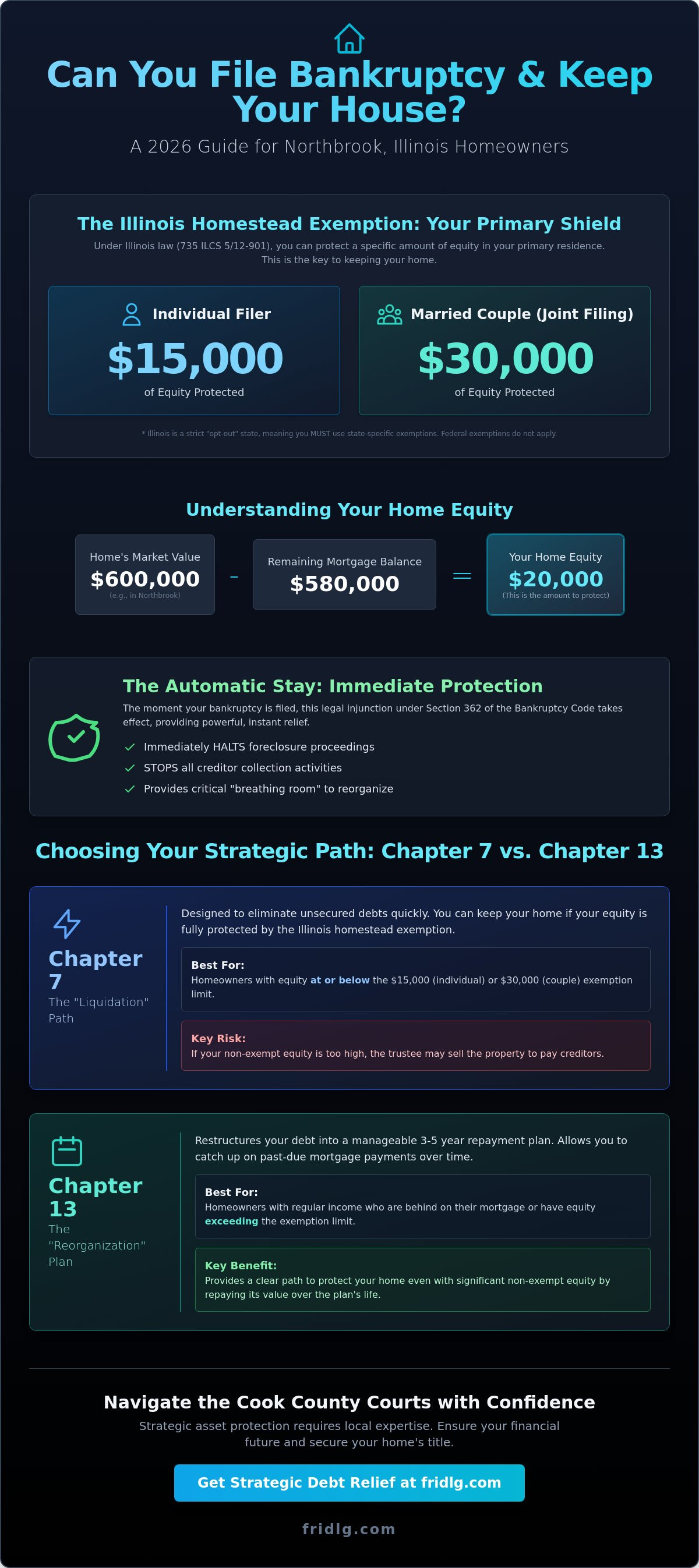

The formula for determining your risk is straightforward: Market Value minus Mortgage Balance equals Equity. In the Northbrook real estate market, where median home prices often exceed $600,000, precise valuation is mandatory. A professional appraisal is a critical first step because even a $10,000 discrepancy in valuation can determine whether a trustee attempts to sell the home. Negative equity occurs when the outstanding mortgage balance exceeds the property's current market value, which often makes the home an unattractive target for liquidation by a bankruptcy trustee.

The Automatic Stay: Immediate Protection for Northbrook Homeowners

The moment your attorney files the bankruptcy petition, the Automatic Stay goes into effect under Section 362 of the Bankruptcy Code. This legal injunction immediately halts all collection activities, including pending foreclosure auctions at the Cook County Clerk's office. It provides a necessary breathing room to reorganize finances. You should recognize that the stay is a temporary procedural shield, whereas the eventual discharge provides the permanent legal relief from debt. For those considering their options, understanding Chapter 7 Bankruptcy in Northbrook, IL: A Strategic Guide to Debt Relief is the next logical step in evaluating asset protection strategies.

The Illinois Homestead Exemption: Protecting Your Equity in 2026

Illinois law dictates specific parameters for asset protection through the Illinois Compiled Statutes (ILCS). Unlike many jurisdictions that allow a choice between state and federal systems, Illinois remains a strict "opt-out" state. This legal framework means homeowners in Northbrook must rely exclusively on state-defined protections when evaluating can you file bankruptcy and keep your house. The state legislature has determined that federal bankruptcy exemptions do not apply to Illinois residents, making the local statutes the sole source of relief.

Under 735 ILCS 5/12-901, the homestead exemption serves as the primary mechanism for shielding home equity from creditors. For the 2026 calendar year, the individual exemption remains established at $15,000. This figure represents the specific amount of equity a single owner can protect from the bankruptcy estate. When reviewing Chapter 7 Bankruptcy Basics, it becomes evident that any equity exceeding this statutory threshold may be subject to liquidation by a court-appointed trustee to satisfy outstanding creditor claims.

Individual vs. Joint Filing Protection

The statutory framework provides a distinct strategic advantage for married couples who choose to file a joint petition. If both spouses hold title to the Northbrook property and occupy it as their primary residence, they're permitted to aggregate their individual exemptions. This doubling effect increases the total protected equity to $30,000. This calculation is a foundational element for families determining if they can maintain their home while seeking debt relief.

- Single Owner: $15,000 equity protection.

- Joint Owners (Both on Title): $30,000 equity protection.

- Wildcard Exemption: Illinois provides a $4,000 "wildcard" under 735 ILCS 5/12-1001(b) for personal property; however, this cannot be applied to real estate.

For a precise assessment of how these figures impact your specific financial position, a strategic legal consultation can provide the necessary procedural clarity.

Eligibility Requirements for the Homestead Exemption

To qualify for these protections, the property must function as your primary residence. Investment properties, commercial real estate, or secondary vacation homes don't receive homestead protection under Illinois law. The "730-day rule" established by federal law requires debtors to have resided in Illinois for at least two years prior to filing to utilize these specific state exemptions. If you haven't met this 730-day residency duration, the court may require the application of exemptions from your previous state of residence.

Temporary absences from the property don't necessarily disqualify a Northbrook homeowner from claiming the exemption. The law recognizes an "intent to return" rule, where the exemption remains valid if the owner is away for medical treatment or temporary work assignments but maintains the residence as their permanent legal domicile. Can you file bankruptcy and keep your house if you're currently working out of state? The answer depends on your ability to prove this intent through tax records, voter registration, and utility bill maintenance.

Chapter 7 vs. Chapter 13: Choosing the Right Strategic Path for Your Home

The choice between Chapter 7 and Chapter 13 defines the ultimate security of your primary residence. While both chapters provide an automatic stay to halt foreclosure actions, their mechanisms for long-term retention differ significantly. Chapter 7 offers a swift resolution, typically concluding within 120 to 180 days. It's a liquidation process that requires precise equity management. Chapter 13 functions as a structured reorganization, spanning 36 to 60 months, designed specifically for those facing mortgage arrears.

Keeping Your House in Chapter 7

To answer the question, can you file bankruptcy and keep your house under Chapter 7, you must meet two primary conditions. First, your mortgage payments must be current at the time of filing. Second, your home equity must fall within the Illinois homestead exemption limits. As of 2026, Illinois law protects up to $15,000 of equity for a single filer and $30,000 for a married couple filing jointly.

If your equity exceeds these thresholds, a court-appointed trustee may liquidate the property to satisfy creditors. This makes the valuation process critical for Northbrook homeowners. You'll also need to pass specific income requirements to qualify for this chapter. For a detailed breakdown of these eligibility rules, consult our guide on What is the Means Test for Chapter 7? A Northbrook, IL Guide (2026).

Saving a Foreclosed Home in Chapter 13

Chapter 13 provides a robust mechanism for homeowners who've fallen behind on payments. The "cure and maintain" strategy allows you to keep your home by paying the regular monthly mortgage while simultaneously resolving arrears through a court-approved repayment plan. This plan lasts three to five years, providing a predictable path to full ownership.

Key advantages of this strategic path include:

- Zero Interest on Arrears: You repay missed payments over the life of the plan without additional interest charges, which can save thousands of dollars compared to private bank negotiations.

- Lien Stripping: If your home's current market value is lower than the balance of your first mortgage, it's often possible to strip second mortgages or HELOCs. This reclassifies them as unsecured debt, which you might only pay back in part.

- Immediate Foreclosure Halts: The filing triggers an immediate stay, stopping a scheduled sale even if it's only 24 hours away.

While Chapter 7 focuses on debt elimination, Chapter 13 is a recovery tool. It's the preferred choice for Northbrook residents who have significant equity but face temporary cash flow disruptions. It ensures that can you file bankruptcy and keep your house remains a viable reality even when a bank has already initiated legal action.

Common Obstacles: Past-Due Payments and Mortgage Reaffirmation

Many Northbrook homeowners hesitate to seek relief because they've already fallen three or four months behind on their mortgage payments. This delay often stems from the misconception that arrears disqualify you from retention. In reality, the automatic stay triggered by a filing immediately halts foreclosure proceedings initiated by lenders like Chase or BMO. While a Chapter 7 filing provides only temporary relief from a pending sale, a Chapter 13 filing allows you to cure these defaults over a three to five-year period. The question of can you file bankruptcy and keep your house often depends on your ability to maintain current payments while systematically addressing the past-due balance through a court-approved repayment plan.

Strategic oversight is also required for Cook County property tax obligations. If you have outstanding taxes, the Cook County Treasurer's office may sell those debts to third-party buyers. Bankruptcy can stop a tax sale or provide a mechanism to redeem the taxes, but failing to disclose these liens during your filing creates a significant risk to your title. Your relationship with institutional lenders remains strictly contractual; they're generally satisfied as long as the plan addresses their secured interest and insurance requirements are maintained.

Should You Sign a Reaffirmation Agreement?

A reaffirmation agreement is a voluntary legal contract where you waive the bankruptcy discharge for a specific debt, remaining personally liable for the mortgage. While signing this document ensures the lender continues reporting your on-time payments to credit bureaus, it also means you're not protected from a deficiency judgment if you default later. Bankruptcy judges in the Northern District of Illinois scrutinize these agreements closely. They'll only approve them if your income remains sufficient to cover the expense without causing undue hardship. For many, the risk of future personal liability outweighs the benefit of a slightly faster credit score recovery.

Dealing with Junior Liens and HELOCs

Homeowners with multiple loans or Home Equity Lines of Credit (HELOCs) may utilize specific Chapter 13 provisions to reduce their debt burden. Lien stripping allows a debtor to reclassify a second or third mortgage as unsecured debt, which is then discharged at the end of the case. A junior lien is eligible for stripping only if the fair market value of the residence, as determined by a professional appraisal, is lower than the total balance owed on the first mortgage. This process effectively removes the secondary lienholder's claim against the property title. To determine if your current home valuation supports this strategy, contact our legal team for a detailed asset evaluation.

- Chapter 13 provides a structured environment to pay back mortgage arrears without the threat of immediate foreclosure.

- Reaffirmation agreements should be evaluated based on long-term financial stability rather than short-term credit reporting.

- Cook County property tax liens must be integrated into the filing to prevent third-party loss of title.

Strategic Debt Relief with Fridman Legal in Northbrook

Legal proceedings in the Northern District of Illinois demand a level of precision that national firms rarely provide. National debt relief conglomerates often operate through high-volume call centers, where cases are processed with minimal attention to the specific procedural rules of the Cook County court system. O. Allan Fridman has spent 20 years navigating the Illinois bankruptcy landscape; this localized expertise is the foundation of our practice. When clients ask if they can you file bankruptcy and keep your house, the answer depends on the strategic application of state exemptions within the local court framework. Our firm integrates real estate law with debt relief strategies to ensure your home remains protected from liquidation.

Predictability is a core pillar of our service. We utilize a flat-fee structure to eliminate the anxiety of billable hours. This allows you to focus on your financial recovery without fearing hidden costs or unexpected invoices. Every petition we draft is a product of rigorous analysis, designed to withstand the scrutiny of the United States Trustee. O. Allan Fridman personally oversees the coordination of your bankruptcy filing with real estate valuation data to provide a comprehensive defense of your assets. This tailored approach ensures that your specific financial circumstances are handled with the professional integrity they deserve.

Navigating the Northbrook Bankruptcy Process

The Meeting of Creditors, or 341 Meeting, often creates stress for debtors, yet it's a standard procedural step. Our role is to ensure you're fully prepared for the trustee's inquiries regarding your assets and liabilities. We focus on maximizing equity protection through the Illinois homestead exemption, which currently protects up to $15,000 of equity for an individual. By carefully documenting your home's value, we provide a definitive path to debt relief. If you're concerned about expenses, explore our Low Cost Bankruptcy Chapter 7 options for Northbrook residents.

Your Next Steps Toward Financial Stability

A free initial consultation serves as the diagnostic phase of your recovery. We analyze your specific equity and income to determine the most effective chapter for your situation. Whether you choose Chapter 7 for a fresh start or Chapter 13 to cure mortgage arrears, we remain your strategic partner. Our commitment includes post-bankruptcy planning to help you rebuild your credit score and maintain long term stability. The question of whether can you file bankruptcy and keep your house is answered through meticulous preparation and deep legal knowledge. Don't leave your home's future to chance. Schedule a consultation with Fridman Legal today to begin your transition toward financial freedom.

Securing Your Northbrook Property Through Strategic Debt Relief

Navigating the intersection of federal bankruptcy law and Illinois property exemptions requires a calculated approach. Whether you're leveraging the Chapter 13 repayment structure to cure mortgage arrears or utilizing the Illinois Homestead Exemption to protect equity, the path to financial stability is defined by precision. Understanding the nuances of 2026 regulations ensures that your primary residence remains protected while you discharge unsecured liabilities. A central question for many Northbrook residents remains: can you file bankruptcy and keep your house? The answer is often affirmative when you align your filing with current local statutes and court precedents.

Fridman Legal brings nearly 20 years of specialized Illinois bankruptcy experience to every case, providing the technical oversight needed to manage complex reaffirmation agreements. Our firm provides local expertise across Northbrook and Chicago, offering flat-fee bankruptcy services for transparent, affordable relief. By addressing past-due payments through a structured legal framework, you're not just resolving debt; you're preserving your family's future. Protect your home and reset your finances; contact Fridman Legal for a Northbrook bankruptcy consultation. You've worked hard for your home, and the right legal strategy ensures it stays yours.

Frequently Asked Questions

Is the Illinois homestead exemption enough to protect my Northbrook home?

Under 735 ILCS 5/12-901, the Illinois homestead exemption protects up to $15,000 of equity for an individual or $30,000 for a married couple filing jointly. Whether this is sufficient depends entirely on your property's current market value minus your outstanding mortgage balance. If your equity exceeds these statutory limits, a Chapter 7 trustee possesses the legal authority to liquidate the asset to satisfy your creditors.

Can I keep my house if I have $50,000 in equity and file Chapter 7?

You generally cannot retain a home with $50,000 in equity during a Chapter 7 liquidation because it exceeds the $15,000 individual exemption. The trustee will likely sell the property to recover the non-exempt portion for your creditors. In this scenario, Chapter 13 bankruptcy is the preferred strategic path, as it allows you to keep the home by paying the non-exempt equity amount through a 3 to 5 year court-approved repayment plan.

What happens if I stop paying my mortgage during the bankruptcy process?

Ceasing mortgage payments during bankruptcy triggers a motion for relief from the automatic stay by your lender. While the initial filing provides an injunction against collection, 11 U.S.C. § 362 requires you to maintain all post-petition payments on secured debts. If you fail to meet these obligations, the court will likely permit the bank to resume foreclosure proceedings despite your active bankruptcy status.

Will filing for bankruptcy in Chicago stop a scheduled foreclosure sale?

Filing for bankruptcy creates an immediate automatic stay that halts any scheduled foreclosure sale in the Circuit Court of Cook County. This federal protection remains active throughout the duration of your case unless a creditor successfully petitions the court to lift it. It's a vital tool for homeowners who want to determine if they can you file bankruptcy and keep your house by restructuring their arrears through a legal framework.

Can I file for bankruptcy and keep a second vacation home or rental property?

Retaining a second home is complex because the Illinois homestead exemption applies strictly to your primary residence. Any equity in a vacation property or rental unit is considered a non-exempt asset that a Chapter 7 trustee will target for liquidation. To keep such properties, you must file under Chapter 13 and commit to a 60 month plan that pays creditors the equivalent value of the equity held in those secondary assets.

How long do I have to live in Illinois to use the $15,000 homestead exemption?

You must maintain a primary residence in Illinois for at least 730 days prior to your filing date to utilize the state's $15,000 homestead exemption. If you moved to Northbrook within the last 24 months, the court may require you to use the exemptions from your previous state. This residency requirement prevents individuals from moving specifically to take advantage of more favorable state exemption laws before seeking debt relief.

Do I still have to pay my property taxes if I file for bankruptcy in Cook County?

You remain legally obligated to pay all property taxes to the Cook County Treasurer during and after your bankruptcy case. Real estate tax liens are typically non-dischargeable and maintain priority over almost all other financial claims. If taxes remain unpaid, the county will proceed with a tax sale, which can eventually result in the loss of your home ownership regardless of your federal bankruptcy protections.

Can I keep my house if my spouse doesn’t file for bankruptcy with me?

You can keep your home when filing individually if the property is titled in "tenancy by the entirety" under 735 ILCS 5/12-112. This legal designation protects a primary residence from being sold to pay debts that are only in the name of one spouse. It's a primary reason many residents find they can you file bankruptcy and keep your house even when their spouse isn't part of the legal proceeding.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.