What if the constant ringing of your phone stopped tonight and you could finally see a path toward keeping your family home in Chicago or Northbrook? It's completely normal to feel a sense of dread when looking at your bank account, especially when you're worried about the Illinois Means Test or losing the equity you've worked so hard to build. You probably feel like you're stuck between a rock and a hard place, but filing for bankruptcy isn't a sign of failure; it's a calculated move to reclaim your future. Deciding between chapter 7 vs chapter 13 bankruptcy Illinois often feels like a high-stakes guessing game, but the updated 2026 regulations have actually made it easier for many residents to protect their property while finding relief.

We've put together this guide to help you navigate these choices with confidence and clarity. You'll learn how the significant increase in homestead exemptions to 50,000 dollars for individuals can work in your favor and which path leads to a faster recovery. Our goal is to give you the exact information you need to stop the collector calls, secure your house, and start a clear plan to rebuild your credit by 2027. We'll break down the eligibility requirements and the practical differences so you can decide which strategy fits your specific financial goals.

Key Takeaways

- Discover how the legal "Automatic Stay" acts as an immediate shield, putting a stop to those stressful collector calls and letters as soon as your paperwork is filed.

- We'll help you weigh the pros and cons of chapter 7 vs chapter 13 bankruptcy Illinois so you can choose between a fast fresh start or a structured plan to save your home.

- Learn how a Chapter 13 filing gives you a three to five year grace period to catch up on debt while keeping your assets safe from foreclosure.

- Get the facts on the updated 2026 Illinois Means Test and property exemptions to see exactly how much of your income and equity you can legally protect.

- Understand why having a clear, professional strategy in Northbrook or Chicago is the best way to ensure your credit is back on track by 2027.

Struggling with Debt in Illinois? Understanding the Chapter 7 vs. Chapter 13 Choice

Living with debt in Illinois isn't just about the numbers on a screen; it's about the weight of every unknown phone call and the pit in your stomach when you check the mail. If you're in Chicago or Northbrook, you've likely seen how aggressive debt collection can get. It feels like you're constantly looking over your shoulder. But there's a reason the legal system provides specific options for relief. Deciding between chapter 7 vs chapter 13 bankruptcy Illinois is the first step toward breathing again. This isn't a sign of failure. It's a strategic pivot to get your life back on track and protect your family's future.

The legal process is designed to help people who have hit a financial wall. You aren't alone in this. In fact, many residents find that once they understand the mechanics of the law, the fear starts to fade. There are two primary paths available, and choosing the right one depends entirely on your income, your assets, and whether you're trying to save a specific piece of property like your home.

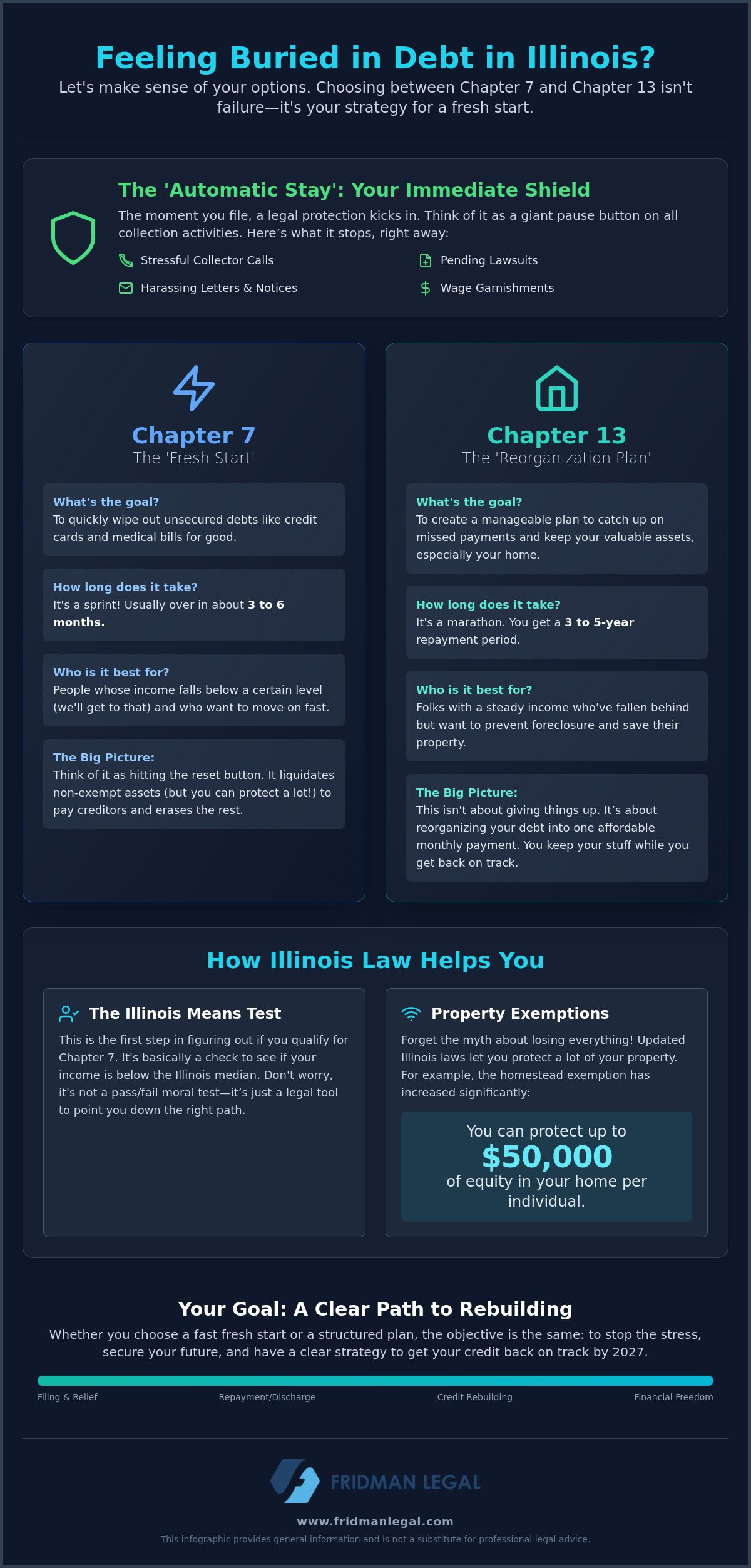

What Exactly is the Automatic Stay?

Think of the Automatic Stay as a legal pause button. The second you file your petition with the court, an invisible wall goes up. Creditors are legally forbidden from crossing it. This means the lawsuits stop. The letters stop. Those disruptive phone calls during dinner finally end. For families in Northbrook or the surrounding suburbs, this provides immediate mental space to think clearly again.

It also has a very practical benefit: it halts Illinois wage garnishments. If your paycheck has been shrinking because of a court order, the Automatic Stay puts that money back in your pocket. It gives you the chance to address your bankruptcy case without the constant drain on your current earnings. It's an immediate shield that buys you the time you need to reorganize.

The Big Picture: Liquidation vs. Reorganization

Most people are looking for one of two things: a clean slate or a way to save their property. Chapter 7 is often described as a "fresh start." In this Chapter 7 Bankruptcy Overview, you can see how the process works to wipe out unsecured debt like credit cards or medical bills. It's relatively fast and highly effective for those who qualify under the income limits. It's about leaving the past behind and starting over with a zero balance on most of your obligations.

On the other hand, Chapter 13 is a "catch-up plan." It’s built for people who have a steady income but have fallen behind on mortgage or car payments. Instead of losing your assets, you reorganize your debt into a manageable three to five year payment plan. You pay back what you can afford, and at the end of the period, the remaining eligible debt is discharged. Both options are perfectly ethical ways to reset your financial compass and move toward a stable 2027.

Ultimately, the choice comes down to your specific goals. If you want to keep your house and you have the income to support a plan, Chapter 13 is a powerful tool. If you just need to erase the debt and start over, Chapter 7 might be the better fit. We'll dive deeper into how the Illinois Means Test decides which path you can take in the following sections.

Chapter 7 Bankruptcy in Illinois: The 'Fresh Start' for Unsecured Debt

Chapter 7 is the most common path for people who just want to wipe the slate clean. It's often called straight bankruptcy because it doesn't involve a long-term payment plan. When you're weighing chapter 7 vs chapter 13 bankruptcy Illinois, the most obvious difference is the speed. While a reorganization plan takes years, a Chapter 7 case is usually wrapped up in about three to six months. It’s a sprint toward financial freedom that allows you to leave the burden of old bills behind without looking back.

One of the biggest myths is that you'll lose everything you own. That simply isn't true in 2026. Thanks to the updated Illinois property exemptions, you can protect a significant amount of assets. For instance, there's a new exemption for household goods up to 5,000 dollars and a wildcard exemption of 4,000 dollars. Most people who file for Chapter 7 in Cook County or Lake County find that their everyday belongings, like furniture, clothing, and basic electronics, are completely safe from being sold to pay off creditors.

Which Debts Can You Actually Erase?

Medical debt is a massive factor for Illinois families. If an unexpected hospital stay or a chronic illness has left you with tens of thousands in bills, Chapter 7 can erase that entirely. The same goes for credit card balances, personal loans, and even old utility bills. It's important to remember that some things don't go away. Child support, most taxes, and student loans typically stay with you. If your primary goal is to save a home from foreclosure rather than just erasing credit cards, you might want to look at how the U.S. Courts on Chapter 13 describe the repayment process, as that path offers different protections for homeowners.

The Role of the Bankruptcy Trustee

You'll eventually meet your Bankruptcy Trustee. Don't worry; they aren't a judge, and you won't be in a courtroom. Their job is simply to review your paperwork and make sure everything is accurate. This happens at the Meeting of Creditors, also known as the 341 meeting. It’s usually a short, straightforward conversation where you answer a few questions under oath about your assets and income. Most of our clients find the process much less intimidating than they expected. If you're feeling overwhelmed by the paperwork, reaching out to a professional for bankruptcy filing assistance can help ensure your petition is handled correctly and your exemptions are maximized.

Chapter 13 Bankruptcy: Protecting Your Illinois Home and Assets

If Chapter 7 is a clean break, think of Chapter 13 as a structured reorganization of your financial life. It's often the preferred route for homeowners in the Chicago suburbs who have fallen behind on payments but aren't ready to give up their front door keys. When you're weighing chapter 7 vs chapter 13 bankruptcy Illinois, the most significant advantage of the latter is that it allows you to keep assets that might otherwise be sold to satisfy creditors. You enter into a court-approved repayment plan that lasts between three and five years. During this time, you pay a single monthly amount to a trustee, who then distributes those funds to your creditors based on a specific priority. It’s a predictable, manageable way to handle your debt without the constant threat of repossession or lawsuits.

Saving Your Home from Foreclosure

For many families, the most powerful feature of Chapter 13 is the ability to "cure" a mortgage default. If you've missed several months of payments, your bank might have already started the foreclosure process. Filing for Chapter 13 triggers the Automatic Stay, which stops a foreclosure sale in its tracks, even if it's scheduled for tomorrow. You then take your "arrearages", which is the total amount of missed payments, late fees, and interest, and spread them out over the life of your 3 to 5 year plan. As long as you make your new monthly plan payments and keep up with your current mortgage, the bank cannot take your home. If you're currently facing this situation, looking into professional foreclosure defense strategies within a Chapter 13 framework is often the most effective way to stay in your house.

Who is Chapter 13 Really For?

This path isn't just for people trying to save a house. It's also the standard choice for high-income earners who have a steady paycheck but simply have too much debt to manage. If your household income is above the Illinois median, you might fail the Means Test for Chapter 7. In that scenario, the law requires a reorganization instead of a total discharge. It's also ideal for people who own assets that aren't covered by the 2026 exemptions, such as a second vehicle or a small business. According to the Illinois Bankruptcy Guide, this chapter also provides a unique "co-debtor stay." This means if you have a family member who co-signed a personal loan or a car note, the bankruptcy filing protects them from collection actions while you're in the plan. It’s a strategic tool for those who want to protect their loved ones while they rebuild their own stability.

The Illinois Means Test and Property Exemptions: How the Law Decides

While your personal goals are the most important factor, the legal system has its own set of criteria for determining your path. This is where the technical side of chapter 7 vs chapter 13 bankruptcy Illinois comes into play. You don't simply pick the one you like best; you have to qualify. The court uses two main tools to make this decision: the Means Test and the schedule of property exemptions. These aren't meant to be hurdles, but rather guardrails that ensure the bankruptcy system is used fairly based on your actual financial capacity in 2026.

It's a common misconception that earning a good living prevents you from seeking relief. The law looks at your "disposable income," not just your gross salary. Even if you "fail" the initial test for a Chapter 7 filing, it doesn't mean you're out of options. It simply means the court believes you have enough left over each month to pay back a portion of what you owe through a reorganization plan. This keeps the process grounded in reality and ensures that everyone gets the specific type of help they need.

The 2026 Illinois Means Test Explained

The Means Test acts as the primary gatekeeper for those seeking a Chapter 7 discharge. It compares your household income to the median income for a similar family in Illinois. For cases filed between April 1, 2026, and November 1, 2026, the thresholds have been updated to reflect current economic conditions. A one person household has a limit of 73,180 dollars, while a four person household can earn up to 137,902 dollars and still potentially qualify. If your income is above these marks, we look at your allowable expenses, such as your mortgage, health insurance, and taxes, to see if you still qualify. Ultimately, the Means Test is the gatekeeper that determines if you are eligible for the Chapter 7 fresh start.

Keeping Your Stuff: Illinois Exemptions

Many residents worry they'll be left with nothing, but the 2026 Illinois exemption rules are remarkably protective. The Homestead exemption is a perfect example. If you're a homeowner in Northbrook or Chicago, you can now protect up to 50,000 dollars in equity as an individual, or 100,000 dollars if you own the home jointly. This is a massive increase from previous years. There is also a 4,000 dollar "Wildcard" exemption that you can apply to any property you choose, like jewelry or a savings account. Most importantly, your 401k, IRA, and other qualified retirement accounts are generally 100 percent exempt, meaning creditors cannot touch your future security. If you're ready to see how these numbers apply to your specific situation, you can request a professional case evaluation to get a clear picture of your protected assets.

Choosing the Right Path: Why Professional Guidance in Northbrook Matters

Filing for bankruptcy in Cook County or the surrounding suburbs isn't a task you should handle like a standard weekend project. While it might be tempting to try a DIY approach to save on initial costs, the legal reality is much more complex. A single error on your petition or a misunderstanding of the chapter 7 vs chapter 13 bankruptcy Illinois rules can result in the court dismissing your case. This doesn't just waste your time; it can leave you vulnerable to the very creditors you were trying to stop. Having an experienced advocate like O. Allan Fridman means you have someone who understands the local court expectations in Northbrook and Chicago, ensuring your filing is both accurate and strategic.

The goal is to provide a sense of security during a turbulent time. We don't just see you as another case file. We see a person who wants to protect their family and their future. Navigating the bankruptcy process requires a partner who can translate complex regulations into a clear, actionable plan. By working with a professional, you ensure that every exemption is utilized and every legal protection is fully engaged. This isn't just about debt relief; it’s about reclaiming your peace of mind and setting a foundation for your 2027 financial goals, which can be further supported by wealth management experts like Timothy Roberts & Associates, LLC.

The Value of a Strategic Filing

A successful bankruptcy isn't just about getting a discharge. It's about maximizing the benefits of the law. The timing of your filing can save you thousands of dollars, depending on your recent income or upcoming expenses. It’s also about absolute transparency. Failing to disclose an asset, even by accident, can be seen as fraud by the court. We work with you to ensure every detail is documented so you can move forward without fear. For more local insights, you can explore our Chapter 7 Bankruptcy in Northbrook guide, which covers specific strategies for our community.

Taking the Next Step Toward Financial Peace

We believe that everyone deserves a clear, honest conversation about their financial future. That's why Fridman Legal operates with a transparent flat-fee structure. You won't have to guess what your legal costs will be or worry about billable hours adding to your stress. This isn't a high-pressure sales environment. It’s a professional partnership focused on your long-term success. By choosing the right path in the chapter 7 vs chapter 13 bankruptcy Illinois debate today, you're setting yourself up to have a rebuilt credit score and a stable life by 2027. If you're ready to stop the calls and secure your home, schedule a consultation with Fridman Legal today and let’s discuss your next move.

Take Control of Your Financial Future Today

You've seen how the 2026 legal landscape offers real protection for your home and assets. Whether you're looking for the immediate clean slate of a liquidation or the structured security of a repayment plan, the decision between chapter 7 vs chapter 13 bankruptcy Illinois doesn't have to be overwhelming. You now know that the updated homestead exemptions and the Means Test are tools designed to help you, not hold you back. The most important step is simply deciding that you've had enough of the collector calls and the uncertainty.

At Fridman Legal, we bring nearly 20 years of Illinois bankruptcy experience to every case we handle. You'll work directly with O. Allan Fridman, receiving the personalized attention your situation deserves without worrying about hidden costs. Our flat-fee services ensure that your path to financial recovery is predictable and transparent from day one. It's time to stop worrying about the past and start planning for a stable 2027. You can get a free, confidential debt evaluation from Fridman Legal right now to explore your options. You've worked hard for what you have; let's make sure you keep it.

Frequently Asked Questions

Is Chapter 7 better than Chapter 13 in Illinois?

Neither option is objectively better than the other; the right choice depends entirely on your financial goals and the assets you want to protect. Chapter 7 is often preferred for its speed, as it can wipe out unsecured debts like credit cards in just a few months. However, Chapter 13 is a superior tool for homeowners who are behind on their mortgage and want to prevent a foreclosure sale. Your income level and the specific nature of your debt will ultimately dictate which path serves you best.

Can I keep my car if I file for bankruptcy in Chicago?

Yes, most residents are able to keep their primary vehicle through the use of property exemptions. As of 2026, the Illinois motor vehicle exemption allows you to protect up to 3,600 dollars in equity for a single car. If you have more equity than that, or if you are behind on your auto loan payments, a Chapter 13 plan can often be used to protect the vehicle from repossession while you catch up on what you owe, ensuring you maintain reliable transportation for work and essential healthcare visits to specialists like the Frankel Foot & Ankle Center.

How long does a Chapter 13 repayment plan last?

A court-approved repayment plan typically lasts between three and five years. The exact duration is determined by your household income relative to the state median and the amount of time needed to pay back priority debts. Once you successfully complete the final payment of your plan, any remaining eligible unsecured debt is discharged, giving you a clean slate to move forward.

Will my employer find out if I file for bankruptcy?

It's unlikely that your employer will ever know about your filing. While bankruptcy is a matter of public record, the court doesn't send notices to your boss. The only common exceptions are if you're using bankruptcy to stop an active wage garnishment or if you choose to have your Chapter 13 payments deducted directly from your paycheck for convenience. Most people find that their professional life remains completely unaffected by the process.

What is the 2026 median income for the Illinois Means Test?

The income limits are based on the size of your household and are updated periodically. For cases filed between April 1, 2026, and November 1, 2026, the limit for a one person household is 73,180 dollars. A household of four has a threshold of 137,902 dollars. Understanding these figures is a vital part of the chapter 7 vs chapter 13 bankruptcy Illinois evaluation, as they determine whether you're eligible for an immediate discharge or a reorganization plan.

Can I file for bankruptcy alone if I am married?

You absolutely have the right to file for bankruptcy individually even if you're married. This is often the best strategy if the majority of the debt is in only one spouse's name. You should be aware that the court still requires you to disclose your spouse's income on the Means Test to get an accurate picture of the household's total financial health, but their personal credit score won't be directly impacted by your filing.

How much does it cost to file for bankruptcy in Illinois?

The total cost involves both the mandatory court filing fees and the fees for your legal representation. While court fees are standardized across the federal system, attorney fees can vary depending on whether you're filing a relatively simple Chapter 7 or a more involved Chapter 13. Many people find that choosing a flat-fee structure is the best way to ensure their costs stay predictable throughout the entire legal process.

How soon can I get a credit card after a Chapter 7 discharge?

You'll likely start seeing credit card offers in your mailbox within weeks of your discharge being finalized. Banks often view post-bankruptcy consumers as a lower risk because they no longer have other competing debts and can't file for Chapter 7 again for several years. By starting with a secured card and making consistent payments, most residents can significantly rebuild their credit scores by 2027.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.