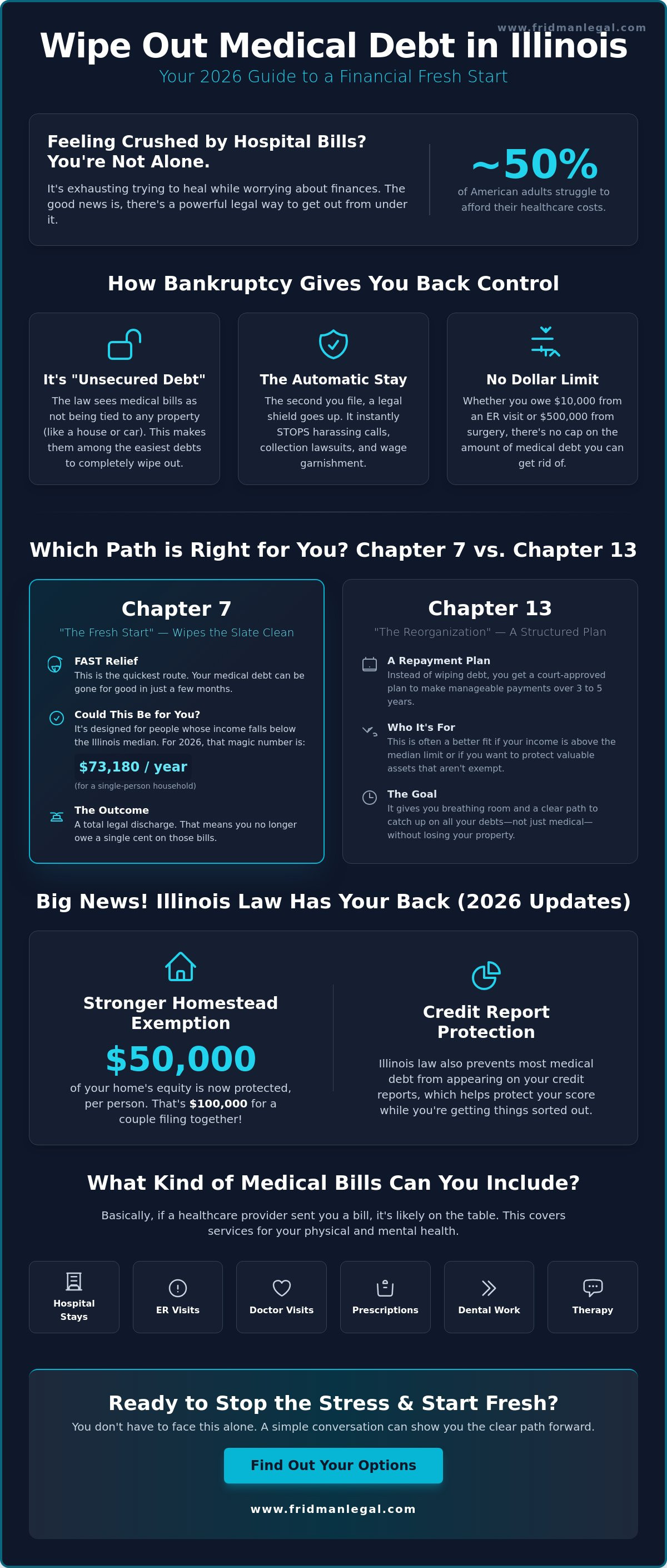

Did you know that nearly half of all American adults currently struggle to afford their healthcare costs? If you're feeling the weight of mounting hospital invoices, you aren't alone. It's exhausting to deal with harassing calls from collectors or the constant fear of wage garnishment in Cook County while you're trying to focus on your recovery. You've worked hard for what you have, and the thought of losing it all to a medical emergency is overwhelming.

The good news is that filing bankruptcy on medical bills Illinois has become a more powerful tool for protection than ever before. With the 2026 updates to state law, including a significant jump in the homestead exemption to $50,000, you can likely wipe out your debt without losing your most valuable assets. This guide provides a clear roadmap to help you achieve a total discharge of medical debt and stop collection lawsuits in their tracks. We'll explore the newest 2026 income limits for Chapter 7, explain how the latest consumer protections keep your bank account safe, and show you exactly how to start rebuilding your financial life by 2027.

Key Takeaways

- You'll see why medical bills are categorized as general unsecured debt, which makes them fully eligible to be wiped out legally.

- We'll show you how filing bankruptcy on medical bills Illinois puts an immediate stop to collector harassment and wage garnishment through the power of the Automatic Stay.

- You'll find out if you qualify for the quick Chapter 7 discharge or if a Chapter 13 plan better fits your specific income and financial goals.

- We explain the strategic "One-and-Done" rule so you can time your filing perfectly and avoid being left with new, uncovered medical costs.

- You'll get a simple breakdown of the pre-filing steps and learn how local legal knowledge helps you navigate the Chicago court system with confidence.

Can You Actually File Bankruptcy on Medical Bills in Illinois?

You might be wondering if your medical debt is "special" or if the law treats it differently than a standard credit card balance. The short answer is yes, you can absolutely get rid of these costs. In the eyes of the court, medical bills are considered general unsecured debt. This is favorable for you because it means there's no collateral, like a car or a house, tied to the money you owe. When you explore the option of filing bankruptcy on medical bills Illinois, you'll find that these expenses are usually among the first things to be completely wiped away.

One of the most powerful tools you gain the second you file is the Automatic Stay. Think of it as a legal shield that goes up instantly. It forces debt collectors to stop calling your phone, sending letters, or pursuing lawsuits immediately. If a hospital was planning to garnish your wages in Cook County, that process must stop. It gives you the breathing room you need to focus on your health instead of your mailbox.

Unlike some other legal processes, there's no maximum dollar limit on the amount of medical debt you can discharge. Whether your bills total $10,000 from a quick ER visit or $500,000 from a major surgery, the law allows you to include it all. It's also helpful to distinguish these from priority debts. While things like recent taxes or child support generally stay with you, medical bills are non-priority. This categorization puts them at the top of the list for total elimination in a Chapter 7 Bankruptcy case.

What Counts as Medical Debt Under the Law?

You can include almost any cost related to your physical or mental health. This covers standard doctor visits, long hospital stays, and those expensive emergency room charges that seem to multiply. It also extends to prescription medications, medical devices like oxygen tanks or wheelchairs, and even dental work. If you've had specialized therapies or mental health counseling that insurance didn't cover, those are also eligible for discharge. Essentially, if a healthcare provider sent you a bill for a service, it's likely dischargeable.

The Illinois Fair Patient Billing Act vs. Bankruptcy

Illinois has some of the strongest consumer protections in the country. The Fair Patient Billing Act requires hospitals to screen you for financial assistance before they get aggressive with collections. While this is a helpful first step, hospital charity care often has strict income caps that leave many families behind. Bankruptcy serves as the ultimate fallback when these assistance programs don't cover the full balance. Additionally, Illinois law now prevents most medical debt from appearing on your credit reports, which helps protect your score while you're resolving the underlying debt through the legal system.

Chapter 7 vs. Chapter 13: Which Wipes the Slate Clean?

Picking the right path is the most important decision you'll make in this process. Most people who are overwhelmed by hospital costs hope to qualify for a Chapter 7 filing because it offers the fastest resolution. It's designed to liquidate unsecured debts, meaning your medical balances can simply disappear in a matter of months. If you're looking into filing bankruptcy on medical bills Illinois, you'll find that Chapter 7 is generally the most direct route to a zero balance. As of April 2026, the median income limit for a one person household in Illinois is $73,180, which helps determine if you're eligible for this specific relief.

You don't have to worry about losing everything you own just to get out from under these bills. Thanks to the significant changes in Illinois law that took effect on January 1, 2026, your assets have much better protection. For example, the homestead exemption now protects $50,000 of equity in your primary residence per person. If you and a spouse file together, that's $100,000 in equity that creditors can't touch. Understanding these Bankruptcy Basics is the first step toward reclaiming your financial stability and protecting your home.

Going the Chapter 7 Route in Northbrook

To qualify, you'll need to pass the "Means Test," which compares your household income to other Illinois residents. If your income is below the threshold, Chapter 7 allows for a total discharge of your medical debt. Once the judge signs that discharge order, you're no longer legally obligated to pay those providers a single cent. For a deeper dive into how this works locally, you can read our guide on Chapter 7 Bankruptcy in Northbrook, IL.

When Chapter 13 Makes More Sense

Sometimes your income might be too high for Chapter 7, or you might have a home with equity that exceeds the $50,000 exemption. In these cases, Chapter 13 is a strategic choice. It doesn't wipe the debt instantly; instead, it rolls your medical bills and other costs into one manageable monthly payment. For Cook County residents, this plan usually lasts between three and five years. It's a structured way to pay what you can afford while keeping your property safe from foreclosure. If you're feeling stuck, reviewing your Chapter 13 Bankruptcy Filing options can help you find a sustainable path forward.

The Strategy of Timing: When Should You Actually File?

Timing is a strategic decision that can make or break your fresh start. One detail people often overlook is the "One-and-Done" nature of a Chapter 7 discharge. Under federal law, you can only receive a Chapter 7 discharge once every eight years. If you rush into filing bankruptcy on medical bills Illinois while you're still in the middle of a major treatment plan, you might find yourself with a pile of new, non-dischargeable debt just months after your case closes. You want to ensure that the "line in the sand" drawn by your filing date captures the bulk of your expenses.

If an emergency surgery or an unexpected complication occurs right before you plan to file, it often changes the math. Any debt you incur after the clock starts on your bankruptcy case stays with you. This creates a difficult choice for many families in Cook County. You have to balance the immediate need for relief from collectors with the reality of ongoing medical needs. We focus on finding the specific window where your largest expenses are behind you, but before a creditor can take drastic action like a lawsuit.

Waiting for the Final Bill

If your health allows it, the best strategy is often to wait until you've reached what doctors call "maximum medical improvement." This doesn't mean you're perfectly healthy, but it means your treatment has stabilized and the bills have mostly stopped arriving. When you have a major procedure, you aren't just billed by the hospital. You'll likely receive separate invoices from the surgeon, the anesthesiologist, the imaging lab, and the physical therapist. It's very easy to miss one of these smaller, third party bills. Make sure to gather every single medical bill before your first consultation to ensure nothing is left out of your petition.

Stopping Garnishments and Lawsuits in Illinois

There are times when you simply can't wait for the final bill. If a debt collector has already secured a court judgment and is moving to garnish your wages or freeze your bank account, filing immediately becomes a necessity. The Automatic Stay mentioned earlier stops these aggressive actions in their tracks, regardless of where you are in your medical treatment. If you're still weighing your options and aren't sure if a full filing is necessary yet, you might consider consulting a Debt Settlement Lawyer in Northbrook, IL to see if negotiating your current balances is a viable alternative to the court system.

The Step-by-Step Process of Filing in Illinois

The path to a fresh start isn't a mystery; it follows a very specific sequence of events designed to move you from debt to stability. Most people find that once the process starts, the mental weight begins to lift almost immediately. Here is the typical roadmap for those filing bankruptcy on medical bills Illinois in the Northern District court system.

- Step 1: The Consultation. We conduct a thorough review of your financial landscape, looking at your medical invoices alongside any credit card balances to see which chapter fits your goals.

- Step 2: Credit Counseling. You'll need to complete a pre-filing course. It's a standard requirement, usually done online or by phone, that ensures you've looked at all your options.

- Step 3: Filing the Petition. We submit your formal paperwork to the U.S. Bankruptcy Court for the Northern District of Illinois. This triggers the Automatic Stay.

- Step 4: The Meeting of Creditors. About a month after filing, you'll attend a brief meeting to verify your information. Don't worry; hospitals rarely show up to these.

- Step 5: The Discharge. If everything is in order, you'll receive your discharge notice. This is the legal proof that your qualifying medical debts are gone for good.

Gathering Your Illinois-Specific Paperwork

You'll need a few key documents to get started. This includes your recent paystubs, tax returns from the last two years, and that mountain of medical invoices you've been collecting. When filing bankruptcy on medical bills Illinois, listing every single creditor is the most critical part of your petition. If you leave a surgeon, an anesthesiologist, or a lab off the list, that specific debt might not be wiped out. Having a professional eye on your paperwork ensures no bill is left behind, giving you the total relief you're looking for.

What Happens at the 341 Meeting?

Many people lose sleep over the 341 Meeting, but it's much simpler than it sounds. It isn't a trial, and you won't be in a courtroom in front of a judge. Instead, it's a brief conversation with a court-appointed Trustee. They'll ask basic questions to verify your identity and confirm the accuracy of your petition. While providers have the right to attend, they almost never do for medical debt cases. Your lawyer sits right next to you to handle any technical legal hurdles, so you're never facing the Trustee alone. If you're ready to get this process moving, you can start your filing process with a professional review.

Why Working with a Northbrook Bankruptcy Attorney Matters

Trying to handle the court system on your own is a lot like trying to perform your own surgery. It's technically possible, but the risks of a mistake are far too high. When you're already managing health issues, you don't need the added burden of a complex legal filing. A Northbrook attorney provides a level of predictability that online forms or generic services can't offer. We use a flat-fee structure so you won't have to worry about hourly bills or hidden costs. This transparency is vital when you're already trying to regain your footing after filing bankruptcy on medical bills Illinois.

Our team understands the specific rhythms of the Chicago and Northbrook court systems. We've seen how local Trustees operate and we know how to present your case to protect your assets under the 2026 exemptions. You'll also avoid the "AI-lawyer" trap. While automated tools are becoming common, they can't provide human advice for a human problem. A computer doesn't care about your recovery or your family's future. We do. We're here to offer professional integrity and a steady hand as you move toward a life where medical debt is a thing of the past.

The Fridman Legal Approach to Debt Relief

We don't believe in one size fits all solutions. When you work with us, you get personalized attention from O. Allan Fridman. We take the time to understand your specific medical history and financial hurdles. Our primary goal is often helping you qualify for Fridman Legal Bankruptcy Services under Chapter 7, as this offers the most efficient path to total debt elimination. We focus on getting your paperwork right the first time so you can stop looking backward and start focusing on your 2027 credit rebuilding goals.

Take the First Step Toward Relief

Worrying about collectors for another month won't change your balance, but taking action will. A quick conversation can often provide more clarity than weeks of late-night internet research. We're here to help you move through the 2026 legal process with a modern, professional approach that respects your time and your privacy. If you're tired of the calls and the stress, it's time to see how the law can work in your favor. You can schedule your consultation today to begin your journey toward a genuine fresh start.

Take Control of Your Financial Future Today

The 2026 updates to Illinois law, particularly the significant increase in homestead exemptions, have created a more protective environment for families seeking relief. You now have the legal tools to stop the cycle of collection calls and garnishments while keeping your home and assets safe. By understanding the timing of your filing and choosing the right bankruptcy chapter, you can ensure that your medical debt becomes a hurdle of the past rather than a permanent weight on your future.

Deciding to move forward with filing bankruptcy on medical bills Illinois is a major step toward reclaiming your life. Fridman Legal provides nearly 20 years of local experience and the personalized guidance of a Northbrook native who knows the Chicago court system inside and out. Our flat-fee structure means you'll have predictable costs as we work together to wipe the slate clean. Let's talk about wiping out your medical debt; reach out to Fridman Legal today. You've focused on your health long enough; it's time to let the law focus on protecting your finances.

Frequently Asked Questions

Can medical debt be wiped out in Chapter 7 bankruptcy in Illinois?

Yes, medical debt is fully dischargeable in a Chapter 7 filing. Because these bills are considered general unsecured debt, they don't have priority status like taxes or child support. Once your case is finalized, you're no longer legally required to pay the balances. This is why filing bankruptcy on medical bills Illinois is such a common path for those facing sudden healthcare crises.

Will I lose my house if I file bankruptcy for medical bills in Chicago?

You likely won't lose your home thanks to the 2026 Illinois homestead exemption. As of January 1, 2026, you can protect up to $50,000 in home equity per person. If you and your spouse file a joint petition, that protection doubles to $100,000. Most Chicago homeowners find their primary residence is completely safe throughout the legal process.

How much does a bankruptcy lawyer cost for medical debt in Northbrook?

Professional fees for bankruptcy representation vary depending on the complexity of your financial situation. Most local practitioners in Northbrook offer flat-fee structures so you know exactly what the cost will be before you begin. It's best to check with a legal professional directly to get a quote that reflects your specific debt load and filing needs.

How long does it take to get rid of medical debt through bankruptcy?

A standard Chapter 7 case usually takes between four and six months from the date you file until you receive your discharge notice. If you're filing a Chapter 13 repayment plan, the process is longer, typically lasting between three and five years. Most people dealing with overwhelming medical costs aim for the quicker Chapter 7 route to clear their slate fast.

Can I file for bankruptcy on medical bills if I have a job?

Yes, having a job doesn't disqualify you from seeking debt relief. Eligibility for Chapter 7 depends on the Illinois Means Test. As of April 1, 2026, the median income limit for a single person household is $73,180. If you earn more than the limit for your household size, you can still file for Chapter 13 to manage your payments through a structured plan.

What happens to my credit score after filing for medical bankruptcy?

Your credit score will see an initial decline, but it's often the first step toward a higher score in the long run. By wiping out high debt to income ratios and stopping late payment reports, you create a foundation for recovery. Many residents find they can start rebuilding their credit and qualify for new financing by 2027.

Can I keep my car after filing for Chapter 7 in Illinois?

You can keep your vehicle if the equity falls within the state's exemption limits. Effective January 1, 2026, the Illinois motor vehicle exemption increased to $3,600. If your car is worth more, you might also use the $4,000 wildcard exemption to protect the remaining value. Most people who file are able to keep their primary transportation.

What if I have more medical procedures coming up after I file?

Any medical debt you incur after your filing date isn't covered by the bankruptcy discharge. This is why timing is so critical. If you have upcoming surgeries, it's often better to wait until those procedures are finished. Filing bankruptcy on medical bills Illinois works best when you've reached a point where new, massive bills are unlikely to appear.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.