The assumption that a prior discharge permanently precludes you from seeking further legal protection is a costly misunderstanding of federal statutes. While many residents in the Chicago metropolitan area believe they've exhausted their options, the law allows for strategic, multi-stage filings when financial circumstances shift. The law isn't a barrier; it's a framework. Understanding exactly how many times can you file bankruptcy depends strictly on the chronological gap between your cases and the specific chapters involved. For instance, according to federal guidelines, a Chapter 7 discharge requires an eight-year interval from the previous Chapter 7 filing date, yet other pathways remain accessible much sooner.

The necessity of preserving assets and halting a 2026 foreclosure sale often requires immediate procedural action. You likely seek a definitive answer regarding your standing within the Illinois court system, especially when previous filings complicate your current strategy. This guide provides a precise analysis of the statutory waiting periods and the critical distinction between filing a case and receiving a discharge. We'll examine how a strategic Chapter 13 petition can effectively terminate creditor actions, regardless of your prior discharge history, and establish a clear timeline for your next phase of debt restructuring.

Key Takeaways

- Distinguish between the technical capacity for unlimited filings and the rigorous statutory intervals required to obtain a subsequent debt discharge.

- Evaluate the specific timelines dictated by federal law to ascertain how many times can you file bankruptcy with the benefit of comprehensive debt erasure.

- Explore the strategic application of the Automatic Stay to secure immediate injunctive relief against creditors, independent of immediate discharge eligibility.

- Mitigate the risks of judicial scrutiny and case dismissal by understanding the procedural complexities inherent in multiple bankruptcy petitions.

- Optimize your financial restructuring through a sophisticated analysis of 2026 Illinois exemptions and strategic chapter selection.

How Many Times Can You File Bankruptcy in Northbrook, IL?

Individuals facing persistent financial challenges often inquire about how many times can you file bankruptcy under current regulations. While the statutory framework doesn't explicitly cap the total number of petitions a debtor may submit over a lifetime, it strictly regulates the frequency of debt relief. The distinction between the act of filing and the achievement of a discharge is fundamental to any strategic insolvency plan. In Northbrook, North Shore residents may find themselves contemplating a second filing due to unforeseen medical emergencies or the complex economic shifts observed throughout 2026.

Determining how many times can you file bankruptcy requires a chronological analysis of your previous cases. The legal bottleneck isn't the filing itself but the waiting period required to receive a second discharge. Without a discharge, the debtor remains legally obligated to pay the underlying debt, rendering the filing largely ineffective for long term recovery. Most petitioners follow one of two primary paths: Chapter 7 liquidation or Chapter 13 reorganization. Each path carries specific time constraints that dictate when you're eligible for renewed relief.

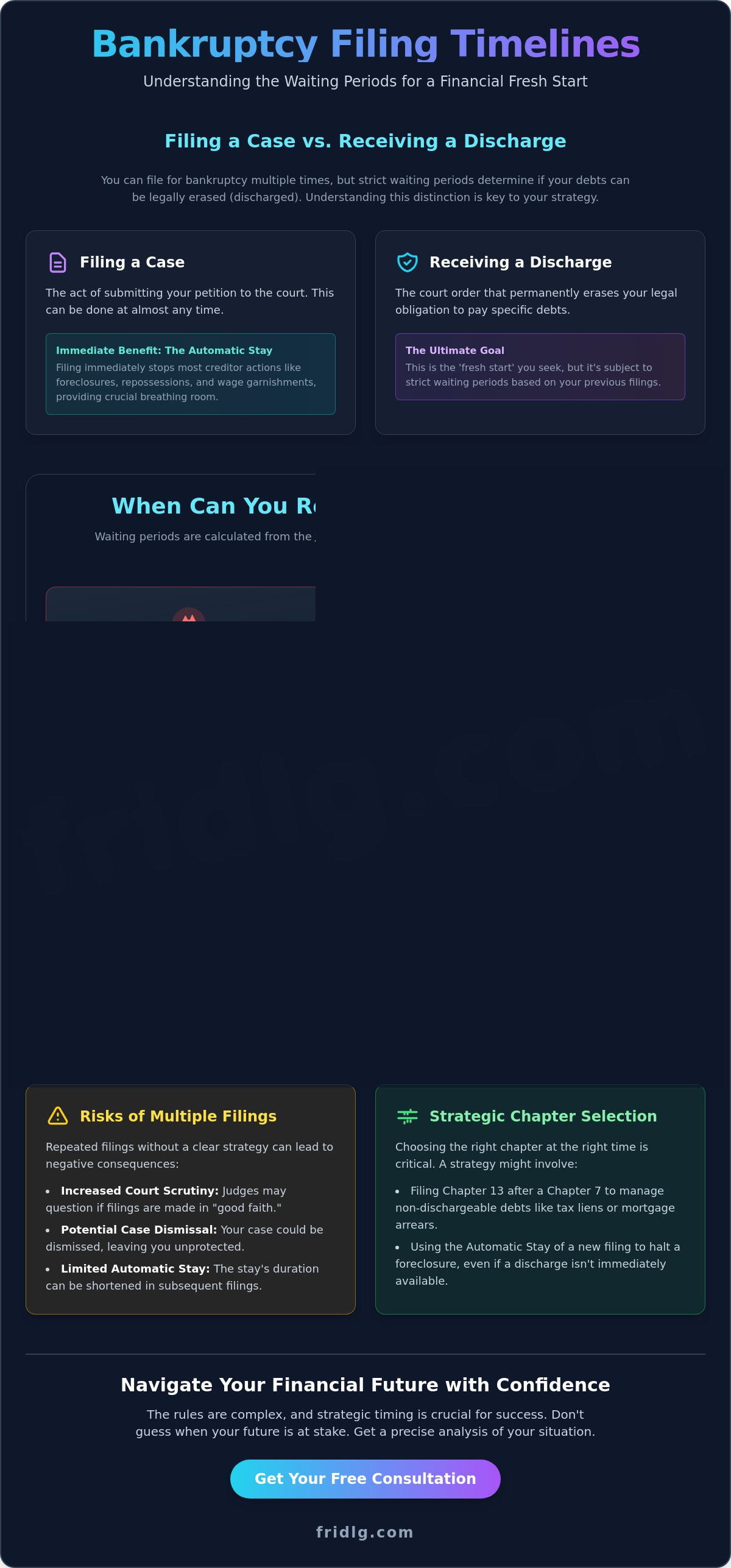

Filing vs. Discharging: Why the Difference Matters

A discharge is the formal legal order that permanently excuses you from the obligation to pay specific debts. It's the primary objective for most Northbrook petitioners. Even if a discharge is currently unavailable due to timing constraints, filing a case triggers the automatic stay. This provision immediately halts collection actions, such as foreclosures or wage garnishments, providing a temporary procedural

Calculating the Waiting Period: When Are You Eligible for Discharge?

The legal framework governing debt relief isn't infinite. It relies on precise chronological benchmarks. For residents in Northbrook and Chicago, the "waiting clock" for a subsequent bankruptcy begins on the exact date the prior case was filed. It doesn't begin on the date the court granted the discharge. This distinction is vital. Filing a new petition even 24 hours before the statutory limit expires results in a denial of discharge. While the case might technically remain open, the debtor remains legally liable for all balances. The court's records in the Northern District of Illinois are meticulous; there's no margin for error when calculating these windows.

Successive Chapter 7 Filings

Under federal law, you must wait eight years between Chapter 7 filings to receive a second discharge. This 8-year mandate is the most restrictive timeline in the bankruptcy code. If you attempt to file at year seven, the court will process the petition, but your debts won't be wiped away. This creates a high-risk scenario where assets are liquidated without providing the intended financial fresh start. This rule ensures that total debt liquidation remains a rare, long-term solution rather than a recurring financial tool. Understanding how many times you can file for bankruptcy requires a strict adherence to these federal windows.

Chapter 13 Timelines and Cross-Chapter Rules

Reorganization plans offer more flexibility than liquidations. The rules change based on the sequence of the chapters filed, reflecting the different nature of repayment versus total discharge.

- Chapter 13 to Chapter 13: There's a 2-year waiting period between filing dates. Because most plans last 36 to 60 months, eligibility for a new discharge often exists the moment the previous case concludes.

- Chapter 7 to Chapter 13: A 4-year waiting period applies. Practitioners often call this a "Chapter 20" strategy. It's used to handle non-dischargeable debts like tax liens or mortgage defaults after a Chapter 7 has cleared other liabilities. It's a sophisticated tool for managing complex financial structures.

- Chapter 13 to Chapter 7: A 6-year gap is mandatory. An exception exists if the previous Chapter 13 plan paid 100% of unsecured claims, or at least 70% through a "good faith" effort. If the debtor didn't meet these thresholds, they must wait the full six years.

Strategic timing is the difference between legal protection and continued creditor harassment. If you're uncertain about your specific eligibility date, consulting a strategic legal advisor ensures your filing aligns with federal requirements. Knowing how many times can you file bankruptcy depends entirely on the specific chapter sequence you choose and the success of your previous filings.

Strategic Use of the Automatic Stay in Chicago and Suburbs

The filing of a bankruptcy petition triggers an immediate legal injunction known as the automatic stay. This provision serves as a robust shield, halting all collection activities, including phone calls, lawsuits, and asset seizures, the moment the court issues a case number. For many residents in Northbrook and the greater Chicago area, the stay’s primary value lies in its power to freeze creditor actions, providing the necessary time to reorganize finances. Even when considering how many times can you file bankruptcy, it's essential to recognize that the stay's protection can be invoked even if the debtor isn't currently eligible for a debt discharge due to the timing of recent prior filings.

In Cook County, Chapter 13 bankruptcy is frequently utilized to address mortgage arrears. A Northbrook homeowner facing a scheduled judicial sale can utilize the stay to stop the foreclosure process instantly. This allows for a court-approved repayment plan to cure the default over a three to five-year period. According to the U.S. Courts Bankruptcy Basics, this stay is a fundamental pillar of the bankruptcy process, ensuring that the status quo is maintained while the legal proceedings unfold. This strategic delay is often the only mechanism capable of preventing the permanent loss of a primary residence or a vehicle essential for commuting to work in the Chicago Loop.

Stopping Wage Garnishments in Illinois

Illinois law allows creditors to garnish up to 15% of a worker's gross weekly wages. The automatic stay terminates these deductions the instant a case is filed in the Northern District of Illinois. Beyond immediate relief, this pause creates a strategic window for negotiations. If a discharge isn't the immediate goal, the stay provides leverage to pursue a structured resolution through a debt settlement lawyer. This approach is particularly effective for high-income professionals in Northbrook who require a discreet method to manage liabilities without the long-term implications of a full bankruptcy discharge.

Halting Foreclosure and Repossession

A second or third filing provides a critical "breathing spell" for families facing the loss of significant assets. However, the law imposes strict limitations on the stay's duration for repeat filers. If a debtor had one case dismissed within the previous year, the stay expires after 30 days unless extended by the court. If two or more cases were dismissed in that timeframe, the stay doesn't go into effect automatically. In such complex scenarios, the expertise of a bankruptcy lawyer chicago is mandatory to petition the court for a stay extension or imposition. Understanding how many times can you file bankruptcy involves more than just counting years; it requires a precise calculation of these stay limitations to ensure assets remain protected during the filing process.

Risks of Multiple Filings: Dismissals and Court Scrutiny

The U.S. Bankruptcy Court for the Northern District of Illinois maintains rigorous oversight regarding repeat petitions. While the law doesn't strictly limit how many times can you file bankruptcy over a lifetime, it imposes severe procedural hurdles for those seeking relief shortly after a prior dismissal. Filing "pro se" in these instances often results in immediate dismissal. Without professional counsel, debtors frequently fail to address the heightened evidentiary standards required to prove they aren't merely stalling creditors. The court's primary objective is to ensure the system remains a tool for debt relief rather than a mechanism for persistent litigation delay.

Understanding Section 362(c)(3)

Under 11 U.S.C. § 362(c)(3), the automatic stay protections change significantly if you had a previous case dismissed within the last 365 days. In these scenarios, the stay protecting your assets expires exactly 30 days after the new filing. To maintain protection, your attorney must file a formal motion to extend the stay before this deadline. The court in Northbrook evaluates "good faith" by examining whether the new case is likely to result in a discharge, unlike the failed predecessor. You must provide clear and convincing evidence that your financial situation has stabilized since the previous dismissal. Failure to secure this extension allows mortgage lenders or car creditors to resume collection actions immediately.

The "Serial Filer" Label and How to Avoid It

Cook County trustees scrutinize repeat filings to identify patterns of bad faith. To avoid being labeled a "serial filer," you must demonstrate a material change in circumstances. This might include a 15% increase in household income or the resolution of a medical crisis that caused the previous case to fail. Transparency regarding your history is mandatory. Concealing a prior case is a violation of Rule 9011 and can lead to a dismissal "with prejudice." In the Northern District, such a ruling often includes a 180-day bar on refiling, leaving assets vulnerable to foreclosure. Determining how many times can you file bankruptcy requires a strategic evaluation of these statutory limitations to ensure your assets remain protected.

- Court Scrutiny: Judges look for filers who use the stay to stop auctions without intending to complete a plan.

- Legal Expertise: Repeat cases require specific motions that self-represented filers rarely navigate successfully.

- Good Faith: You must prove the current filing isn't a continuation of past procedural failures.

- Dismissal Consequences: A dismissal "with prejudice" can permanently bar the discharge of specific debts.

Navigating Your Second Filing with a Northbrook Bankruptcy Attorney

A second bankruptcy filing requires a higher level of strategic precision than the initial petition. Our firm provides a meticulous analysis of your previous filing history and current debt structure to ensure full compliance with federal timelines. Understanding how many times can you file bankruptcy is merely the baseline; the primary objective is optimizing your petition under the 2026 Illinois exemptions. We evaluate your assets against current state protections to determine whether Chapter 7 or Chapter 13 offers the most robust shield for your property in the current economic climate. Our office maintains a policy of transparent, flat-fee pricing for residents in Northbrook and Chicago. This approach ensures you understand the financial commitment before the legal process begins.

The choice between chapters often hinges on your specific goals for asset retention. If you're seeking a total discharge of unsecured debt, we analyze your eligibility for Chapter 7 under the 2026 means test. For those facing foreclosure or vehicle repossession in the Chicago area, a Chapter 13 reorganization might be the superior strategic choice. We focus on the mathematical reality of your debt load. Our team doesn't rely on guesswork. We use hard data to project the outcome of your filing.

The Fridman Legal Approach to Debt Relief

Our firm brings nearly twenty years of experience to the local Chicago bankruptcy landscape. We don't simply process paperwork; we provide strategic advisory services. We emphasize results-driven solutions that prioritize your long-term stability over temporary fixes. A second filing demands a partner who understands the nuances of the local court systems and the tendencies of regional trustees. We view bankruptcy as a tool for credit rebuilding and financial recovery. Our role is to act as a discreet, highly capable guide through the complex legal framework of the Northern District of Illinois.

Preparing for Your Consultation

Efficiency is a hallmark of our practice. To facilitate a productive initial meeting, you'll need to prepare several key documents. Please bring your previous discharge papers, current income verification, and a comprehensive list of all active creditors. Determining your exact "eligible to file" date is a critical technical step. You can find this by reviewing your previous discharge or dismissal orders. These documents establish the statutory waiting period required by the court. We'll verify these dates during our session to confirm your eligibility under current federal law. Contact Fridman Legal today to discuss your bankruptcy eligibility.

Securing Your Financial Future Through Strategic Legal Counsel

Navigating the statutory requirements of the U.S. Bankruptcy Code requires more than a simple understanding of the forms. It demands a precise calculation of discharge eligibility dates. While the law allows for repeat filings, the 8 year mandatory waiting period between Chapter 7 discharges under 11 U.S.C. § 727 remains a firm barrier. The automatic stay's duration often diminishes to just 30 days for those filing a second case within a single calendar year. Understanding how many times can you file bankruptcy is only the first step in a complex recovery process.

Our firm leverages nearly 20 years of Illinois bankruptcy experience to provide the structure your case requires. We offer flat-fee Chapter 7 and 13 services. This ensures cost transparency while we deliver local Northbrook and Chicago representation. Success in the federal court system depends on meticulous adherence to procedural rules and proactive management of court scrutiny. It's a path toward stability that you don't have to walk alone. Strategic planning today prevents procedural dismissals tomorrow.

Schedule a Strategic Debt Relief Consultation in Northbrook

Frequently Asked Questions

How many times can you file Chapter 7 bankruptcy in Illinois?

You're eligible to receive a Chapter 7 discharge once every 8 years. This statutory timeframe is calculated from the date you filed your previous case to the date you initiate the new petition. The U.S. Bankruptcy Code, specifically Section 727(a)(8), establishes this 96-month interval as a mandatory requirement for debt elimination. If you submit a petition before this period elapses, the court will refuse to discharge your qualifying debts.

What is the waiting period between Chapter 7 and Chapter 13?

A 4-year waiting period applies if you previously received a Chapter 7 discharge and now seek a Chapter 13 discharge. This duration begins on the filing date of the initial Chapter 7 case. While you're permitted to file a Chapter 13 case earlier to manage a repayment plan, the court won't grant a final discharge of remaining balances until the full 48-month period has passed.

Can I file bankruptcy again if my first case was dismissed?

You can typically refile immediately unless the court issued a specific 180-day refiling bar. This restriction often occurs under Section 109(g) if you failed to follow court orders or voluntarily dismissed the case after a creditor requested relief from the automatic stay. If your previous case was dismissed without prejudice, there's no mandatory waiting period, though the automatic stay's duration may be limited in subsequent filings.

Will filing bankruptcy a second time hurt my credit score more than the first?

A second filing impacts your credit score, but the initial damage is frequently less dramatic since the first bankruptcy already established a lower baseline. FICO data indicates that a Chapter 7 filing remains on your report for 10 years, while Chapter 13 stays for 7 years. A subsequent filing adds a new public record, which complicates the 24-month recovery period typically seen after a single successful discharge.

Can I stop a foreclosure in Northbrook if I already filed bankruptcy once?

You can halt a foreclosure through the automatic stay, but its protection is limited if you've filed previously within the last 12 months. If one case was dismissed in the past year, the stay only lasts 30 days unless your attorney proves a good faith change in circumstances. For those with two or more dismissals within a single year, the automatic stay doesn't take effect at all upon filing.

What happens if I file for bankruptcy before the waiting period is over?

Filing before the statutory period concludes results in the court denying your debt discharge. You might still benefit from the automatic stay's temporary protection against creditors, but your underlying debts will remain legally enforceable once the case ends. Understanding how many times can you file bankruptcy is critical because a premature filing exhausts your resources without providing the permanent financial relief most Illinois petitioners require.

Is there a limit on how many times I can file Chapter 13 in Chicago?

The law doesn't set a maximum number of Chapter 13 filings, but you must wait 2 years between discharges. This 24-month window is measured from the filing date of the prior successful case. Repeated filings without a documented change in financial stability may lead the court to dismiss the petition for lack of good faith, especially if the cases appear intended only to delay creditors.

How do I find out the exact date of my last bankruptcy filing?

You can retrieve your official filing records through the Public Access to Court Electronic Records (PACER) system. This federal database provides the specific month, day, and year of every petition filed in the Northern District of Illinois. Knowing these precise dates is essential to determine how many times can you file bankruptcy within the legal intervals mandated by the 2005 Bankruptcy Abuse Prevention and Consumer Protection Act.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.