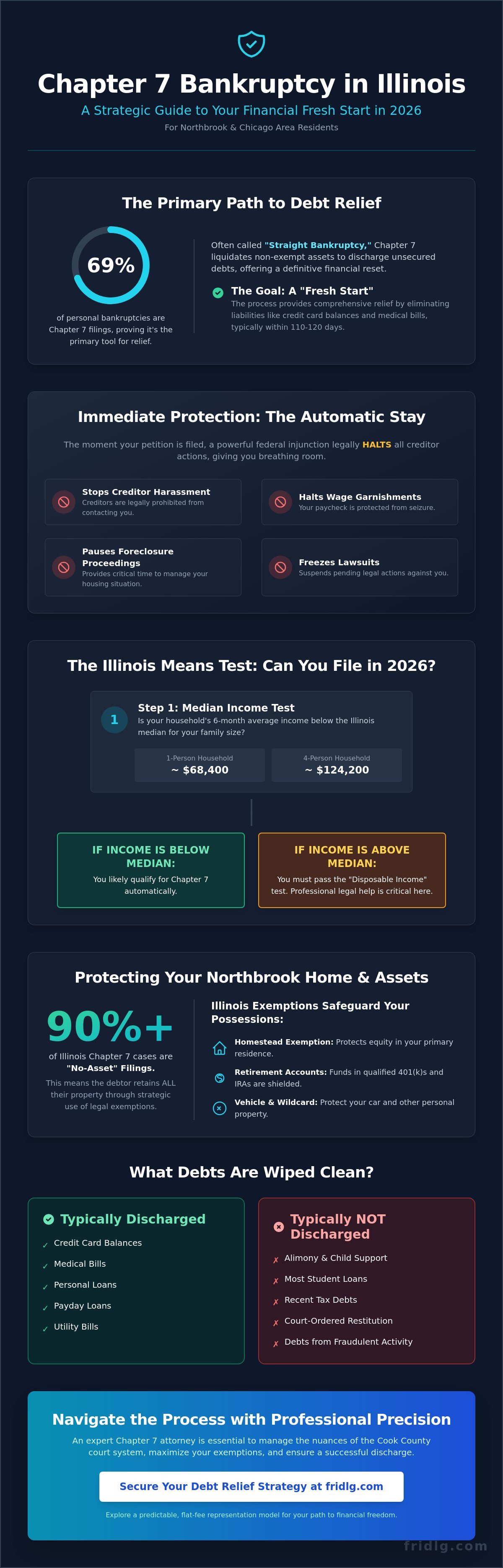

The most effective method to secure a stable financial future in 2026 isn't found in incremental debt management but through the strategic application of federal liquidation laws. You've likely experienced the persistent pressure of creditor harassment and the legitimate concern that your Northbrook residence or Chicago assets might be at risk. It's a heavy burden to carry alone. Federal data indicates that Chapter 7 filings accounted for approximately 69% of all personal bankruptcy cases in recent cycles, proving its status as the primary instrument for genuine relief. By securing a qualified attorney bankruptcy chapter 7 specialist, you'll navigate the rigorous Illinois Means Test with professional precision to protect your exempt property and achieve a definitive fresh start. This guide details the exact legal mechanisms required to invoke the automatic stay immediately and secure a total discharge of qualifying liabilities under current statutes. We'll examine the specific exemptions that keep your car and home safe while providing the roadmap to professional debt resolution.

Key Takeaways

- Gain clarity on the liquidation process and the immediate legal protections provided by the automatic stay against Northbrook creditors.

- Identify the specific 2026 income thresholds and procedural requirements of the Illinois Means Test necessary for a successful filing.

- Discover strategic methods to protect your home and personal assets using the Illinois homestead and wildcard exemptions during the liquidation phase.

- Secure professional precision by engaging an expert attorney bankruptcy chapter 7 to manage the nuances of the Cook County court system and the 341 Meeting of Creditors.

- Explore the advantages of a flat-fee representation model designed to provide financial predictability and a definitive path toward debt relief.

Understanding Chapter 7 Bankruptcy in Illinois: The Fresh Start Provision

Chapter 7 serves as the primary mechanism for individual debt liquidation under federal law. It's often referred to as a "straight bankruptcy" because it facilitates a definitive financial reset by discharging unsecured obligations. As defined by Chapter 7 of the U.S. Bankruptcy Code, the process involves the systematic collection and distribution of non-exempt assets. In the 2026 legal environment, Illinois filers must navigate specific median income thresholds and means testing requirements that have been adjusted to reflect the economic shifts of the past fiscal year. Engaging a qualified attorney bankruptcy chapter 7 ensures that these technical eligibility requirements are met with procedural integrity.

The Purpose of Chapter 7 Liquidation

The liquidation process operates under the supervision of a court-appointed trustee who evaluates the debtor's estate. While the term "liquidation" implies the sale of assets, over 90% of Illinois cases remain "no-asset" filings where the debtor retains all property through statutory exemptions. The timeline typically spans 110 to 120 days from the initial petition filing to the final discharge order. This structured progression aims to provide comprehensive debt relief by eliminating liabilities such as credit card balances and medical bills. A strategic attorney bankruptcy chapter 7 focuses on maximizing these exemptions to protect the client's home, vehicle, and retirement accounts.

Immediate Benefits of the Automatic Stay

The Automatic Stay is a federal injunction that takes effect the moment a petition is filed. This provision creates an immediate legal barrier against creditor actions, effectively halting wage garnishments, foreclosure proceedings, and pending lawsuits in the Cook County Circuit Court. Once the stay is active, creditors are legally prohibited from contacting the debtor or pursuing collection efforts. For residents in Northbrook, this injunction provides the requisite legal insulation to finalize a financial strategy without the pressure of persistent harassment or asset seizure.

Success in a Chapter 7 filing depends on distinguishing between dischargeable and non-dischargeable obligations. Most unsecured debts are eligible for elimination, but certain liabilities remain legally binding post-discharge. These exceptions include:

- Domestic support obligations such as alimony and child support payments.

- Most student loans, unless a specific "undue hardship" is proven in an adversary proceeding.

- Recent tax debts and court-ordered criminal restitution.

- Debts incurred through fraudulent activity or willful and malicious injury.

The 2026 legal landscape requires a meticulous audit of all financial records to ensure that the petition accurately reflects the debtor's status. Precision in these early stages prevents the dismissal of the case and ensures that the "fresh start" provision is fully realized under the law.

Eligibility and the Illinois Means Test: Can You File in 2026?

Securing a debt discharge requires more than a simple petition. The federal government uses a rigorous two-part screening process to ensure only those with genuine financial need access Chapter 7. For Northbrook residents, this starts with the Median Income Test. If your household's average monthly income over the preceding six months is below the Illinois state median, you typically qualify without further financial scrutiny. This initial benchmark serves as a gatekeeper, separating straightforward filings from those requiring complex financial analysis.

The Median Income Comparison

The Illinois median income levels are updated periodically by the Census Bureau. For 2026 filings, these thresholds reflect the economic shifts of the previous 24 months. A single-person household in the Chicago suburbs currently faces a median threshold near $68,400, while a four-person household may exceed $124,200. Household size is the primary variable here; even a high-earning individual might qualify if they support multiple dependents. Detailed eligibility rules and state-specific exceptions are explored in our Chapter 7 Bankruptcy in Northbrook, IL strategic guide.

Calculating Disposable Income

If your income exceeds the state median, you don't face an automatic disqualification. Instead, you must pass the Means Test. This calculation determines if you have enough disposable income to pay back a portion of your debts through a Chapter 13 plan. The test uses a combination of actual expenses and IRS National and Local Standards. Precision is vital because the Illinois Means Test data dictates exactly how much you can claim for housing, transportation, and utilities in Cook County.

Allowable deductions that an attorney bankruptcy chapter 7 specialist will identify include:

- Mandatory retirement contributions and union dues required for employment.

- Court-ordered payments such as child support or alimony.

- Specialized healthcare costs and life insurance premiums.

- Actual monthly payments for secured debts, specifically your home or vehicle.

Failing this test results in a "presumption of abuse." This usually forces a conversion to Chapter 13, where you'll spend three to five years in a court-supervised repayment plan. Strategic planning with an attorney bankruptcy chapter 7 expert allows for the legitimate maximization of these deductions. We focus on the technical nuances of the law to ensure your filing remains in Chapter 7, protecting your future earnings from creditor claims and ensuring a faster path to financial recovery.

Protecting Your Northbrook Home and Assets During Liquidation

A common fear among Northbrook residents considering debt relief is the total loss of personal property. This concern is largely unfounded. While the process involves a structured liquidation, the legal framework provides significant protections for essential assets. The strategic objective of a skilled attorney bankruptcy chapter 7 is to utilize state and federal exemptions to shield as much of your wealth as possible. Most filers in the Chicago area find that they retain the vast majority of their possessions, including their homes, vehicles, and retirement savings.

The distinction between exempt and non-exempt assets is the pivot point of any filing. Exempt assets are those protected by law from being sold by the bankruptcy trustee to pay creditors. Non-exempt assets are those with significant equity above the legal limits, which may be subject to turnover. In practice, many Chapter 7 cases are "no-asset" cases, meaning the debtor's property falls entirely within the exemption limits. Understanding the Chapter 7 Bankruptcy Basics is essential for setting realistic expectations regarding asset retention.

The Illinois Homestead Exemption

For many in Northbrook, the primary residence is their most significant asset. In 2026, the Illinois homestead exemption allows an individual filer to protect up to $15,000 in home equity. If you're filing a joint petition with a spouse, this amount doubles to $30,000. This exemption applies only to your primary residence and doesn't cover investment properties or vacation homes. A precise real estate equity analysis is required before you file. If your property's market value, minus your mortgage balance and the exemption, leaves a surplus, the trustee might attempt to sell the home. For those managing complex property transitions or looking for broader context on Northbrook property law, our Real Estate Lawyer for Closing guide provides additional insights into local market dynamics.

Vehicle and Personal Property Exemptions

Maintaining a vehicle is often a necessity for commuting to Chicago or managing daily life in the suburbs. Illinois law permits an exemption of $2,400 for a single motor vehicle. To protect a car with higher equity, we often utilize the "wildcard" exemption. This flexible provision allows you to protect up to $4,000 of any personal property, including cash, bank accounts, or additional vehicle equity. Other critical protections include:

- Retirement Accounts: ERISA-qualified plans, 401(k)s, and most IRAs are generally 100% exempt, ensuring your long-term security remains intact.

- Household Goods: Standard furniture, clothing, and appliances are rarely targeted for liquidation due to their low resale value and specific statutory protections.

- Tools of the Trade: Professionals can often protect up to $1,500 in equipment necessary for their livelihood.

Precise valuation is the cornerstone of asset protection. Overlooking the true value of an asset or failing to disclose it can lead to the loss of that property or even a denial of your discharge. An experienced attorney bankruptcy chapter 7 ensures that every item is valued correctly and matched with the appropriate exemption to maximize your "fresh start."

Navigating the Cook County Bankruptcy Court: The Attorney’s Role

The Northern District of Illinois Eastern Division operates under a distinct set of procedural mandates that have undergone significant refinements leading into 2026. Successfully managing a Chapter 7 filing requires more than clerical accuracy; it demands a strategic alignment with the specific expectations of the Cook County trustees. A seasoned attorney bankruptcy chapter 7 specialist ensures that every asset disclosure aligns with the court’s rigorous transparency standards. This professional oversight is essential because the court treats even minor administrative oversights as potential grounds for a case dismissal.

Local presence in the Northbrook and Chicago corridor provides a distinct advantage in managing the court’s strict calendar. Deadlines in the Eastern Division are unforgiving. Missing a single filing window for the Statement of Financial Affairs can jeopardize the entire discharge. A local attorney monitors these milestones through the federal CM/ECF system, providing a level of oversight that national "document preparation" services cannot replicate. This proximity allows for a more responsive approach to the specific requirements of the judges presiding at the Dirksen Federal Building.

The 341 Meeting of Creditors

The 341 meeting represents the primary procedural hurdle in a Chapter 7 case. It typically occurs within 21 to 40 days after the initial petition is filed. During this session, the bankruptcy trustee examines the debtor under oath. The inquiry focuses on the accuracy of the schedules and the valuation of assets, such as Northbrook real estate or private business interests. An attorney prepares the client for these specific lines of questioning, ensuring that answers are precise and legally sound. The presence of counsel serves as a stabilizing force, preventing the trustee from expanding the scope of the meeting beyond the necessary statutory inquiries.

Avoiding Procedural Dismissals

Filing without professional representation carries a documented risk of failure. In the previous judicial cycle, data indicated that pro se filings were dismissed at a rate nearly ten times higher than those handled by experienced counsel. Common errors include the failure to submit the Certificate of Credit Counseling within the mandatory 15-day window or the miscalculation of the Means Test based on current Cook County median income data.

A strategic Chicago lawyer applies the latest 2026 local rules to protect the debtor's interests. This involves a meticulous review of all schedules to ensure no "hidden" assets are inadvertently omitted, which could otherwise lead to allegations of bad faith. By contrast, generic national services often overlook the nuances of Illinois exemptions, potentially leaving valuable personal property unprotected. Professional representation ensures that the path to a discharge remains clear of these avoidable technical traps.

Protect your assets and ensure a successful filing by scheduling a strategic bankruptcy consultation with our experienced legal team.

Strategic Debt Relief with Fridman Legal: Professional Representation

Fridman Legal approaches debt relief through the lens of strategic asset protection and long-term solvency. Selecting an attorney bankruptcy chapter 7 specialist requires a partnership built on transparency and proven expertise. O. Allan Fridman brings over 20 years of experience within the Illinois legal system to every case, ensuring that Northbrook residents receive counsel that's both technically precise and strategically sound. The firm's boutique structure allows for a level of attention that larger, volume-based practices often lack. This personalized focus ensures that every petition is handled with the meticulous care required to navigate the complexities of federal bankruptcy courts.

Transparent Flat-Fee Bankruptcy Services

Predictability remains a cornerstone of professional legal representation. Fridman Legal utilizes a fixed-rate fee structure for Chapter 7 petitions, which removes the financial volatility associated with traditional hourly billing. This model ensures that clients understand their total legal obligations before the process begins. By eliminating hidden costs, the firm provides a clear financial roadmap for individuals seeking a fresh start without the anxiety of mounting legal invoices. The standard Chapter 7 filing package includes:

- A comprehensive means test analysis to confirm eligibility under current Illinois standards.

- Detailed preparation and electronic filing of the bankruptcy petition and schedules.

- Professional representation at the mandatory Section 341 Meeting of Creditors.

- Management of all standard correspondence with the court-appointed trustee and creditors.

The peace of mind that comes from knowing the total legal cost upfront allows clients to focus on their financial recovery rather than worrying about billable minutes. This commitment to transparency reflects the firm's broader dedication to professional integrity.

A Comprehensive Approach to Financial Stability

Bankruptcy isn't an isolated event; it's a recalibration of one's financial trajectory. The firm integrates these proceedings with broader strategies, such as Estate Planning, to secure a family's legacy post-discharge. This holistic method is particularly beneficial for professionals in the Chicago suburbs who require sophisticated solutions for complex asset structures. Working with a local Northbrook boutique firm ensures that your attorney bankruptcy chapter 7 understands the specific nuances of the local court system and the unique economic environment of the North Shore.

Securing a stable financial future requires immediate, decisive action. Northbrook residents can schedule a confidential consultation to evaluate their eligibility and discuss the most effective path forward. Contact Fridman Legal to initiate a professional assessment of your financial standing and begin the transition toward long-term security. Professional integrity and a commitment to meticulous documentation define every interaction, providing the foundation for a true fresh start.

Architecting Your Financial Recovery in 2026

Navigating the rigorous 2026 Illinois Means Test requires a precise understanding of current regulatory standards. Protecting your Northbrook home and personal assets during a liquidation process isn't a matter of chance; it's the result of a disciplined legal strategy. Our firm leverages nearly 20 years of Illinois bankruptcy expertise to ensure every petition adheres to the strict procedural requirements of the Cook County Bankruptcy Court. When you engage a dedicated attorney bankruptcy chapter 7 specialist, you're securing a structured path toward a complete debt discharge. O. Allan Fridman provides personalized representation for every client, ensuring that complex filings receive the attention they deserve. We maintain professional integrity through transparent flat-fee billing for all Chapter 7 petitions, which provides clarity in an otherwise uncertain period. This methodical approach transforms a daunting legal hurdle into a manageable transition toward long-term stability. You don't have to face these complexities alone.

Secure your financial future with a professional Chapter 7 consultation at Fridman Legal

Frequently Asked Questions

Is it possible to file Chapter 7 bankruptcy and keep my house in Illinois?

You can typically retain your primary residence in Illinois if the equity doesn't exceed the statutory exemption limits. Under 735 ILCS 5/12-901, individuals may exempt up to $15,000 in home equity, while married couples filing jointly can protect $30,000. If your equity falls within these parameters and you remain current on mortgage payments, the property remains secure during the liquidation process.

Can an attorney stop wage garnishment immediately in Northbrook?

An experienced attorney bankruptcy chapter 7 specialist can halt wage garnishment immediately through the invocation of the automatic stay. This legal injunction, codified in 11 U.S. Code § 362, becomes effective the moment your petition is filed with the court. It prohibits creditors from continuing collection actions, including the 15% maximum wage deduction allowed under Illinois law; providing immediate financial stabilization.

How much debt do I need to have to make Chapter 7 bankruptcy worthwhile?

While the U.S. Bankruptcy Code doesn't mandate a minimum debt threshold, legal professionals generally consider Chapter 7 once unsecured liabilities exceed $10,000. This figure balances the cost of filing against the total relief obtained. You must evaluate your debt-to-income ratio; if your non-exempt assets are minimal and your debt exceeds 50% of your annual income, the procedure offers a strategic recovery path.

What is the Illinois Means Test and how does it affect my eligibility?

The Illinois Means Test determines your eligibility by comparing your average monthly income from the previous six months to the Illinois median income for a household of your size. If your earnings fall below the state median, you qualify automatically for Chapter 7. For those above the median, a secondary calculation subtracts IRS-approved living expenses to determine if sufficient disposable income exists to fund a Chapter 13 plan.

How long does the Chapter 7 bankruptcy process take in Cook County?

The Chapter 7 process in the Northern District of Illinois typically concludes within 120 to 180 days from the initial filing date. Following the submission of your petition, the court schedules a Meeting of Creditors, also known as a 341 hearing, approximately 30 to 45 days later. If no objections arise from the trustee or creditors, the court usually issues the discharge order 60 days after that meeting.

What happens to my credit score after a Chapter 7 discharge in 2026?

Your credit score will likely experience an immediate reduction of 100 to 200 points following the discharge in 2026. However, many filers see their scores begin to stabilize and improve within 12 to 24 months as they demonstrate responsible credit utilization. While the Chapter 7 filing remains on your credit report for 10 years, the elimination of high debt-to-income ratios often makes you a more attractive candidate for future financing.

Can I include medical bills and credit card debt in my Chapter 7 filing?

You can include 100% of your qualifying medical bills and credit card debt in a Chapter 7 filing. These are classified as general unsecured debts, which the court typically discharges entirely at the conclusion of the case. By working with a qualified attorney bankruptcy chapter 7 expert, you ensure that all creditors are properly notified, preventing any residual liability or post-discharge collection attempts on these specific balances.

How much are typical attorney fees for a Chapter 7 bankruptcy in Chicago?

According to industry data for the Chicago metropolitan area, attorney fees for a standard Chapter 7 case generally range between $1,200 and $2,500. This professional fee is separate from the $338 filing fee mandated by the U.S. Bankruptcy Court for the Northern District of Illinois. Costs fluctuate based on the complexity of your financial portfolio and the volume of creditors involved in the litigation.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.