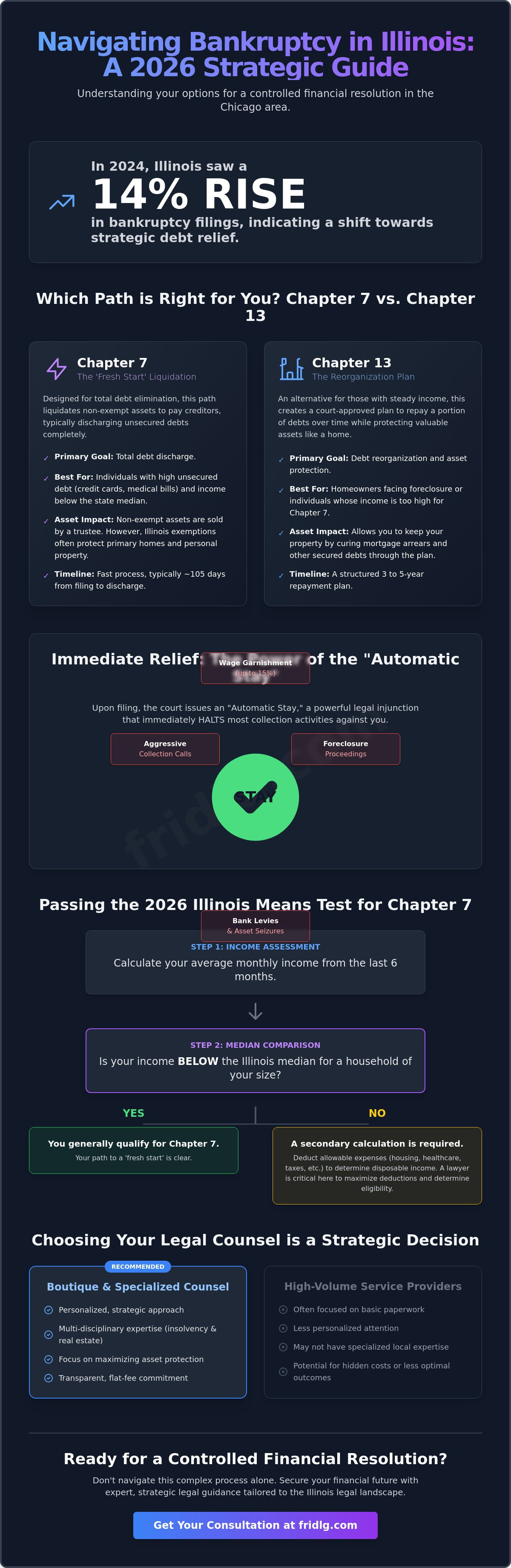

A strategic bankruptcy filing is not a concession of defeat; it's a precise legal maneuver designed to preserve the integrity of your financial future. In 2024, data from the American Bankruptcy Institute indicated a 14 percent rise in Illinois filings, proving that sophisticated debtors increasingly view this path as a necessary tool for asset protection. Whether you're facing the immediate threat of a 15 percent wage garnishment or the prospect of losing a family residence in the Chicago suburbs, engaging a specialized bankruptcy lawyer ensures your interests remain the priority. The stigma often associated with debt relief is a relic of the past that has no place in a modern, calculated business strategy.

You likely recognize that the current economic climate demands more than just basic paperwork; it requires a boutique approach to Chapter 7, 11, and 13 filings. This guide provides the clarity required to move from a state of uncertainty to one of controlled resolution. We'll examine the specific legal frameworks governing Illinois in 2026, detail the mechanisms for stopping aggressive collection actions, and outline a roadmap for total financial recalibration through strategic counsel.

Key Takeaways

- Identify the fundamental differences between Chapter 7, 11, and 13 filings to determine the optimal path for your specific debt reorganization or discharge needs.

- Understand how current Illinois median income thresholds and the 2026 Means Test impact your eligibility for Chapter 7 bankruptcy in the Chicago metro area.

- Learn how a specialized bankruptcy lawyer utilizes the "Automatic Stay" to immediately halt aggressive collection actions, including wage garnishments and bank levies.

- Gain insights into selecting high-caliber legal counsel by distinguishing between personalized boutique representation and high-volume legal service providers.

- Discover the strategic advantages of a multi-disciplinary approach that combines insolvency law with real estate expertise under a transparent flat-fee commitment.

Understanding Bankruptcy Options in Northbrook and the Chicago Suburbs

Bankruptcy is a federal legal mechanism designed to facilitate the discharge or reorganization of debt for individuals and entities facing insolvency. For residents of Northbrook and the surrounding Cook County area, this process is governed by the United States Bankruptcy Code, yet it remains deeply influenced by Illinois state exemptions. A clear Understanding Bankruptcy Options in Northbrook and the Chicago Suburbs is essential for anyone seeking to preserve their financial integrity. The 2026 economic climate, characterized by a 3.4% stabilization in core inflation and specific shifts in the federal funds rate, necessitates a calculated approach to filing. Strategic timing ensures that the petitioner maximizes the protection of their liquid assets and real estate holdings.

Navigating the federal courts in the Northern District of Illinois requires more than a general knowledge of the law. It demands a local perspective on how trustees in the Chicago area evaluate petitions and apply local rules. A specialized bankruptcy lawyer provides the precision required to align a client’s financial disclosure with the court's rigorous standards. Whether the objective is asset preservation or a complete financial reset, the choice of chapter determines the trajectory of the recovery process. Professional representation ensures that the complexities of the 2026 fiscal environment don't compromise the petitioner's long-term objectives.

Chapter 7: The 'Fresh Start' Liquidation

Chapter 7 involves the liquidation of non-exempt assets by a court-appointed trustee to satisfy creditor claims. In practice, most Northbrook residents utilize Illinois state exemptions to protect their primary residence and personal property from being sold. This process primarily targets unsecured liabilities, such as credit card debt and medical bills, which are often discharged entirely. The typical timeline for a Chapter 7 case in the Chicago area involves a 105-day window from the initial filing to the final discharge order. Chapter 7 is a tool for total debt elimination for qualified individuals.

Chapter 13: Reorganization for Homeowners

Chapter 13 offers a strategic alternative for those who possess a steady income but are burdened by significant debt loads or the threat of foreclosure. This chapter creates a court-sanctioned repayment plan that spans a duration of 3 to 5 years. It’s a powerful instrument for stopping foreclosure proceedings on a Northbrook residence, as it allows the homeowner to cure mortgage arrears over the life of the plan. A bankruptcy lawyer assists in drafting a plan that balances the debtor's monthly disposable income against the requirements of Illinois law. This structure provides a predictable path to solvency while ensuring that high-value assets remain under the owner’s control throughout the process.

The Illinois Means Test and Asset Exemptions in 2026

The Illinois Means Test serves as the primary filter for Chapter 7 eligibility. It functions by comparing your average monthly income from the six months preceding your filing against the median income for a household of your size in Illinois. For residents in the Chicago-Naperville-Elgin metro area, these figures are adjusted periodically to reflect the regional cost of living. Understanding the technical nuances of The Illinois Means Test and Asset Exemptions in 2026 is essential for any debtor seeking to preserve their financial future through the federal court system.

If your income falls below the state median, you generally qualify for Chapter 7 liquidation. However, if your earnings exceed this threshold, a secondary calculation becomes necessary. This involves deducting specific "allowable" expenses, such as housing, utilities, and healthcare, based on IRS national and local standards. A bankruptcy lawyer ensures these deductions are applied accurately to determine if you possess sufficient disposable income to fund a repayment plan.

Passing the Means Test in Cook County

Failing the initial income comparison doesn't mean debt relief is unavailable. Many high-income earners in Cook County successfully qualify for Chapter 7 by documenting high mandatory expenses, such as childcare or significant tax obligations. If the final calculation indicates you have the means to pay back a portion of your debt, the case typically transitions to Chapter 13. This allows for a structured three to five year repayment period. It's a common misconception that earning a high salary disqualifies you from the process; in reality, the complexity of the 2026 standards often requires a strategic legal consultation to identify every available deduction.

Protecting Your Assets from Creditors

Illinois has opted out of federal bankruptcy exemptions, requiring filers to use state-specific statutes to protect their property. The Illinois Homestead Exemption is a cornerstone of this protection, allowing individuals to shield up to $15,000 in equity in their primary residence. Married couples filing jointly can double this amount to $30,000. While this may seem modest compared to other jurisdictions, it remains a powerful tool for preventing the forced sale of a home.

Beyond real estate, the Illinois Compiled Statutes (735 ILCS 5/12-1001) provide several key protections for personal property:

- Motor Vehicles: You can protect up to $2,400 in equity in a single vehicle.

- Wildcard Exemption: A $4,000 exemption applies to any personal property, including cash or bank accounts.

- Professional Tools: Up to $1,500 in tools of the trade are exempt from creditor claims.

- Retirement Accounts: Most ERISA-qualified plans and IRAs are 100% exempt under state law.

Retaining a bankruptcy lawyer ensures that your assets are properly valued and scheduled to fit within these statutory limits. For those exploring Chapter 7 Bankruptcy in Northbrook, IL, the objective is to maximize the retention of personal wealth while legally discharging unsecured liabilities.

Strategic Debt Relief: Stopping Garnishment and Foreclosure

The moment a bankruptcy lawyer submits your petition to the federal court, a powerful legal mechanism known as the automatic stay is activated. This isn't merely a procedural pause; it's a court-ordered injunction that immediately halts all collection efforts. In Illinois, where creditors can legally garnish up to 15% of your gross wages, the automatic stay provides essential financial breathing room. It effectively freezes bank levies and prevents creditors from seizing funds directly from your accounts, preserving the liquidity you need for essential living expenses. For residents in Northbrook and the surrounding Chicago suburbs, this protection is the most immediate benefit of the filing process.

The strategic utility of the stay extends to real estate preservation. If your home is scheduled for a judicial sale, the bankruptcy filing stops the clock on foreclosure proceedings. This intervention allows for a structured evaluation of your assets and liabilities without the imminent threat of dispossession. While the United States Courts provide resources regarding filing for bankruptcy without an attorney, the complexity of Illinois exemptions and local court rules makes professional guidance a prerequisite for a successful stay. A single filing error can lead to a dismissal, which may limit the stay's effectiveness in subsequent filings.

Ending Creditor Harassment Immediately

Creditors and collection agencies are legally bound to cease all communication once they receive notice of your bankruptcy filing. The automatic stay functions as a legal injunction against all collection actions, including phone calls, demand letters, and active lawsuits. If a creditor persists in these activities, they face severe legal consequences, including sanctions and potential liability for your legal fees. Your bankruptcy lawyer becomes the sole point of contact for all financial adversaries; this shift transfers the burden of communication from the individual to a professional representative. This structured environment replaces the chaos of constant harassment with a disciplined, court-supervised process.

Foreclosure Defense and Debt Settlement

Bankruptcy offers tools that traditional debt negotiation cannot match. While a Debt Settlement Lawyer in Northbrook, IL can often reduce principal balances, bankruptcy provides the unique ability to strip junior liens or second mortgages under specific Chapter 13 conditions. If the value of your home has dropped below the balance of your first mortgage, the court may reclassify a second mortgage as unsecured debt. This strategic maneuver can eliminate thousands of dollars in debt that a standard settlement would leave untouched. It's a precise legal operation that requires a thorough analysis of current market valuations and debt structures to ensure the most favorable outcome for the debtor's long-term stability.

How to Choose a Bankruptcy Lawyer in the Chicago Area

Selecting the right legal counsel is a decision that dictates the trajectory of your financial recovery. In the 2026 economic climate, characterized by shifting interest rates and evolving credit markets, a generic approach is insufficient. You need a bankruptcy lawyer who treats your case as a unique strategic challenge rather than a clerical task. The selection process requires a rigorous evaluation of technical proficiency and local reputation.

First, verify the attorney's standing within the Northern District of Illinois. Local rules in the Eastern Division are precise; a practitioner must be active in these specific courtrooms to stay ahead of procedural shifts. Second, distinguish between high-volume "mills" and boutique practices. Mills prioritize turnover, which often leads to missed exemptions or poorly structured repayment plans. A boutique firm offers a direct line to the principal attorney, ensuring that sophisticated assets receive the scrutiny they require. Third, confirm expertise in both personal and business sectors. Many 2026 filings involve "prosumers" or small business owners where personal and professional liabilities overlap. Fourth, insist on fee transparency. Whether utilizing a flat-fee model for Chapter 7 or an hourly structure for Chapter 11, the engagement letter must be unambiguous. Finally, use the initial consultation to evaluate the attorney's analytical depth. If they don't ask about your long-term business goals, they aren't the right fit.

The Boutique Advantage: Personalized Legal Strategy

High-volume firms frequently utilize automated software that misses the subtle details of complex financial portfolios. This leads to avoidable audits. A Northbrook-based boutique firm provides a distinct advantage by offering the same level of sophistication as downtown giants but with a higher degree of accountability. Direct communication with your lead counsel ensures that your strategy remains agile. Selecting a bankruptcy lawyer who understands the nuances of the North Shore business community provides a layer of discretion that larger, impersonal firms cannot replicate.

This emphasis on personalized, boutique service is a hallmark of high-caliber firms across the country; for example, the Law Offices of Matthew T. Desrochers, P.C. offers similar dedicated advocacy for clients in Massachusetts dealing with bankruptcy and debt reorganization.

Navigating the Cook County Court System

Success in the Northern District depends on more than just filing paperwork. It requires a deep understanding of local trustee expectations and the specific tendencies of the bench. Your lawyer's reputation for accuracy and integrity directly impacts the speed of your discharge. For those requiring specialized guidance, working with a Strategic Bankruptcy Lawyer in Chicago ensures that every local procedural hurdle is anticipated and managed with precision. This localized expertise prevents the administrative bottlenecks that often plague less experienced representatives.

Fridman Legal: A Multi-Disciplinary Approach to Financial Recovery

Financial distress rarely exists in a vacuum. Effective resolution requires a bankruptcy lawyer who understands how debt relief intersects with property rights and corporate obligations. O. Allan Fridman brings over 20 years of experience to the Chicago legal market, providing a sophisticated perspective that prioritizes long-term stability over short-term fixes. Our firm operates on a transparent, flat-fee commitment for Chapter 7 and Chapter 13 filings. This ensures clients face no hidden costs or unexpected billable hours during the most critical phases of their recovery. We believe that professional integrity is built on predictability and clear communication.

Success isn't measured solely by the discharge of debt. It's defined by the strategic preservation of assets and the ability to operate in the 2026 economy without historical burdens. We provide the legal infrastructure necessary for individuals and business owners to transition from insolvency to growth. Our methodology integrates civil litigation expertise with federal bankruptcy procedures, ensuring that every filing serves a broader financial objective. We focus on the precision of the filing to minimize the risk of challenges from creditors or trustees.

Beyond Debt: Real Estate and Business Continuity

A bankruptcy discharge often marks the beginning of a new investment cycle. We assist clients with property transactions post-bankruptcy, ensuring that previous filings don't impede future acquisitions or sales. For Northbrook businesses and contractors, a strategic Chapter 11 filing can provide the breathing room needed to restructure operations while maintaining day-to-day services. This process allows for the renegotiation of unfavorable contracts and the stabilization of cash flow. If you're currently managing a property transfer or moving past a restructuring, consulting a Real Estate Lawyer for Closing in Northbrook ensures your title is clear and your interests are protected.

Securing Your Future with Estate Planning

The conclusion of a bankruptcy case is the optimal time to establish a robust framework for asset protection. Coordinating your fresh start with an updated estate plan prevents future vulnerabilities. We align your financial recovery with long-term family security by drafting instruments that reflect your current economic reality. We help you designate beneficiaries and establish trusts that shield your newly acquired stability. Professional Estate Planning in Northbrook, IL serves as the final step in a comprehensive strategy to insulate your legacy from future liabilities and market volatility. This structured approach ensures that the relief you achieve today remains a permanent foundation for your family's future.

Securing Your Financial Future Through Strategic Legal Counsel

Navigating the complex 2026 regulatory environment requires a disciplined approach to debt restructuring. Protecting your assets under the Illinois Means Test and halting aggressive collection actions like wage garnishments are critical steps toward recovery. These processes demand precision and a deep understanding of local court procedures in Northbrook and the broader Chicago area. Success isn't just about filing paperwork; it's about executing a multi-disciplinary strategy that considers your real estate holdings and long-term civil interests.

Fridman Legal brings nearly 20 years of local Illinois legal experience to every case. We provide flat-fee pricing for standard filings, ensuring transparency while delivering the sophisticated representation typically reserved for complex litigation. Choosing the right bankruptcy lawyer means selecting a partner who prioritizes your stability and professional reputation above all else. Our firm bridges the gap between technical legal requirements and practical business outcomes, providing the steady guidance you need to move past insolvency.

Schedule a strategic consultation with Fridman Legal today to begin your transition toward financial clarity. It's time to regain control of your assets with a firm that values integrity and results.

Frequently Asked Questions

Is it better to file Chapter 7 or Chapter 13 in Illinois?

The optimal choice depends on your income relative to the Illinois median and your specific asset protection goals. Chapter 7 provides a swift liquidation process, typically concluding within 120 days, whereas Chapter 13 requires a 3 to 5 year repayment plan. A strategic bankruptcy lawyer evaluates your disposable income under the Chapter 7 Means Test to determine eligibility. If your household income exceeds the 2025 Illinois median of $72,454 for a single person, Chapter 13 remains the viable structural solution for debt reorganization.

Can I keep my home in Northbrook if I file for bankruptcy?

You can retain your Northbrook residence if the equity falls within the Illinois homestead exemption limits or if you maintain payments through a Chapter 13 plan. Illinois law provides a $15,000 homestead exemption per individual, which doubles to $30,000 for married couples filing jointly. If your home's equity exceeds these statutory limits, Chapter 13 allows you to cure defaults over a 60 month period while retaining possession. We focus on precise valuation to navigate these exemptions effectively within the local jurisdictional framework.

How much does a bankruptcy lawyer cost in Chicago for 2026?

Legal fees for bankruptcy services in the Chicago metropolitan area are influenced by case complexity and the specific chapter filed. Filing fees are standardized by the U.S. Bankruptcy Court for the Northern District of Illinois, currently set at $338 for Chapter 7 and $313 for Chapter 13. Professional fees vary based on the structural complexity of your financial profile and the duration of the engagement. Engaging a bankruptcy lawyer involves an initial retainer that covers the petition preparation and mandatory credit counseling oversight. Detailed fee structures are provided during the initial strategic consultation to ensure full transparency and budgetary predictability.

How long does the bankruptcy process take from start to finish?

A standard Chapter 7 case typically reaches discharge within 4 to 6 months, while Chapter 13 proceedings last between 36 and 60 months. The timeline begins the moment the petition's filed, triggering an automatic stay. For Chapter 7, the 341 Meeting of Creditors usually occurs within 40 days, with the final discharge order following approximately 60 days later. Chapter 13 requires a longer commitment, as the court-approved repayment plan spans a minimum of 3 years. This structured approach ensures a systematic resolution of all creditor claims within the federal legal framework.

What happens to my credit score after filing for bankruptcy?

Filing for bankruptcy results in an immediate reduction of your credit score, though it also provides a foundation for systematic financial recovery. A Chapter 7 filing remains on your credit report for 10 years, while a Chapter 13 filing is visible for 7 years. Many filers see their scores begin to stabilize within 12 to 18 months post-discharge as debt-to-income ratios improve. By eliminating delinquent accounts, you create the necessary space to rebuild your credit profile through disciplined financial management. This transition from insolvency to stability is a critical component of the strategic debt relief process.

Can bankruptcy stop a wage garnishment that has already started?

Yes, the "automatic stay" provision of the Bankruptcy Code immediately halts most active wage garnishments upon filing. Section 362 of the Bankruptcy Code mandates an immediate cessation of collection actions, including wage deductions. Once the petition's electronically filed, we notify your employer and the garnishing creditor to terminate the withholding process. This federal injunction provides instant liquidity relief for your household budget. It's a powerful tool that prevents further erosion of your earnings while the court adjudicates your case.

Do I have to go to court for a bankruptcy case in Cook County?

Most debtors in Cook County attend a 341 Meeting of Creditors, which is currently conducted via telephonic or video conference platforms. While formal courtroom appearances before a judge are rare for standard petitions, the 341 Meeting of Creditors is a mandatory statutory requirement. These sessions are supervised by a trustee and typically last 10 to 15 minutes. We represent your interests during this meeting to ensure all testimony aligns with the filed documentation. Since 2020, the Northern District of Illinois has largely transitioned these meetings to remote formats, increasing efficiency for all parties involved.

What debts cannot be discharged in an Illinois bankruptcy?

Certain obligations, including most student loans, recent tax debts, and domestic support obligations, cannot be eliminated through bankruptcy in Illinois. Federal law prohibits the discharge of child support, alimony, and most government-funded student loans. Additionally, income taxes owed to the IRS that are less than 3 years old generally remain your responsibility. Criminal fines and restitution are also excluded from the discharge order. We conduct a rigorous audit of your liabilities to identify which debts will persist post-bankruptcy, allowing for a more accurate long-term financial strategy.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.