What if the very process you're dreading is actually the most reliable way to save your family home and your car? It's completely natural to feel a heavy sense of anxiety when debt piles up, especially when you're worried that filing for bankruptcy means losing every single thing you've worked for. Many people assume the court just clears out your house and takes your keys, but that's rarely the case. If you're searching for how to protect my assets during bankruptcy, you're actually looking for a strategic path toward a fresh start that keeps your lifestyle intact.

I know that legal jargon can feel incredibly overwhelming when you're just trying to keep your family's foundation solid. This guide will walk you through how to use the major 2026 updates to Illinois laws, including the new $50,000 homestead exemption and the increased $3,600 vehicle protection. You'll learn how the Automatic Stay works to stop creditors in their tracks and how choosing the right filing strategy can provide debt relief without the risk of losing your home. Here's a clear look at how you can navigate this process with confidence and keep your property safe.

Key Takeaways

- You'll see how the Automatic Stay acts as an instant legal shield, stopping bill collectors and foreclosures the second your paperwork is filed.

- We'll show you how to protect my assets during bankruptcy by using the new 2026 Illinois laws that help you keep more of your equity.

- Learn why choosing between Chapter 7 and Chapter 13 isn't just about debt, but about finding the best way to save your home.

- Discover which common mistakes, like selling a car to a friend for cheap, can actually lead to the court seizing your property.

- Find out how a professional strategy can turn a stressful situation into a clear, manageable path toward financial freedom.

The Automatic Stay: Your Immediate Shield Against Creditors

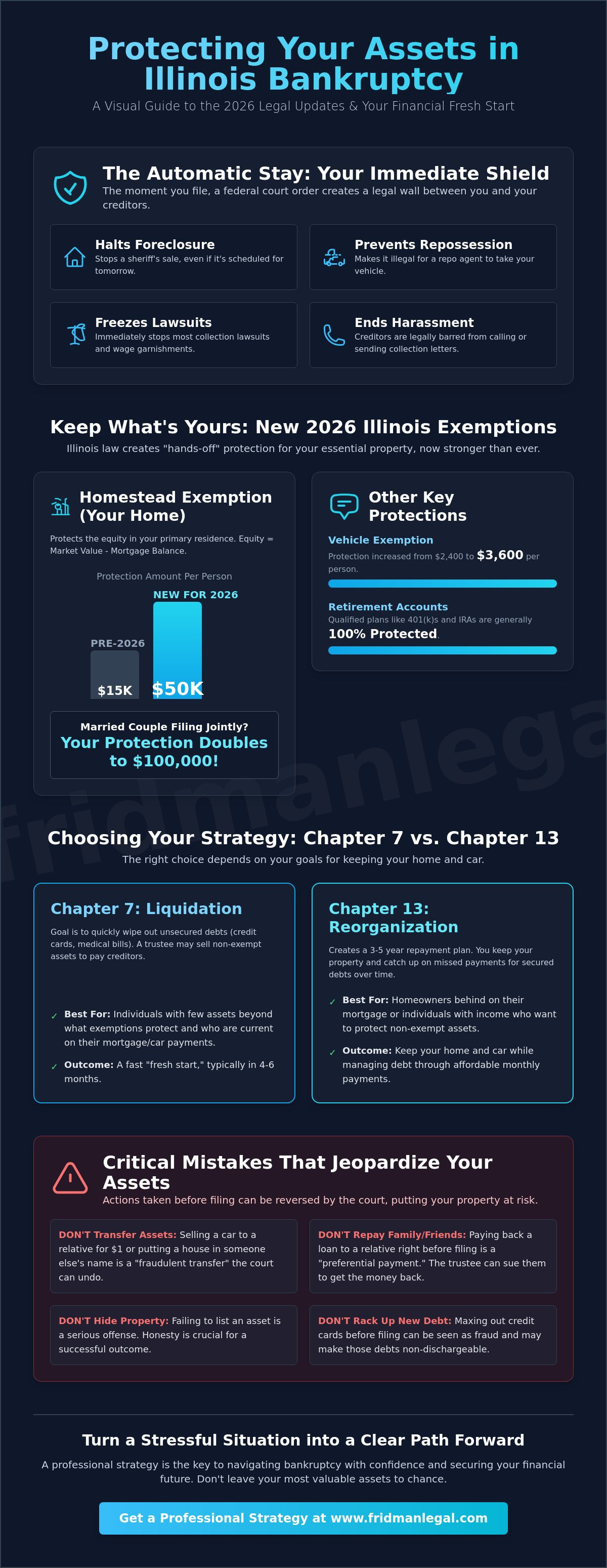

The moment your bankruptcy petition is filed, a decisive shift occurs. A legal wall goes up between you and everyone you owe money to. This isn't just a polite request for space; it's a federal court order known as the automatic stay. Understanding how this mechanism works is the first lesson in how to protect my assets during bankruptcy because it provides the immediate breathing room you need to think clearly. It's a core component of Bankruptcy in the United States, designed to ensure the court can manage your assets fairly without creditors racing to grab what they can first.

Think of the stay as a "pause button" for your financial life. It doesn't matter if a creditor has already started a lawsuit or if they're in the middle of a collection action. Once that case number is generated, the law requires them to stop. This is the most powerful tool available to you because it's instant and it carries the weight of the federal government. If a creditor knowingly violates the stay, they can face serious penalties from the judge, including fines and paying your attorney fees.

Stopping Foreclosures and Repossessions Cold

If you're facing a sheriff’s sale or watching for a tow truck in your driveway, the stay is your best friend. It halts foreclosure proceedings immediately. Even if your home is scheduled for auction tomorrow morning, a filing today stops that sale in its tracks. The same applies to your vehicle. If a repo agent is on the way, the stay makes their actions illegal. While the stay is a temporary pause and not a permanent fix for the underlying debt, it gives you the time to propose a plan, like a Chapter 13 filing, to catch up on payments and keep your property.

Ending the Harassment: No More Calls or Letters

The silence that follows a filing is often the biggest relief for my clients. Once the stay is active, creditors are legally barred from calling you, sending letters, or filing lawsuits against you. If a collector ignores this and keeps pestering you, they're actually violating a federal court order. This shift in power is significant. You go from being pursued by collectors to being protected by the court system. This allows you to focus on your long term recovery instead of screening your phone calls every time the ringer goes off.

It's vital to remember that the stay has limits. It won't stop criminal proceedings, child support collection, or certain tax audits. Also, a creditor can ask the judge to "lift" the stay if you don't stay current on your house or car payments after you file. This is why the stay is a bridge, not a destination. It buys you the time needed to implement a real strategy for how to protect my assets during bankruptcy for the long haul.

Leveraging Illinois Exemptions to Keep What is Yours

When you start looking into how to protect my assets during bankruptcy, you'll quickly realize that the rules vary wildly depending on where you live. Illinois is what's known as an "opt-out" state. This means we don't use the federal bankruptcy exemptions you might read about on national websites; instead, we follow specific laws set right here in Illinois. In simple terms, an exemption is like a legal "hands-off" sign you place on your property that tells the bankruptcy trustee they can't touch it. Because of significant updates that took effect on January 1, 2026, these protections are now stronger than they've been in decades.

Most people are surprised to learn that they can often keep their retirement accounts and pensions entirely. Under Illinois bankruptcy exemptions, qualified retirement plans like 401(k)s and IRAs are generally 100% protected. This ensures that while you're resolving your current debt, your future remains secure. The goal of the system isn't to leave you with nothing; it's to give you a foundation to rebuild.

The Illinois Homestead Exemption Explained

Your home is likely your most valuable asset, and the law reflects that. As of 2026, the homestead exemption has increased to $50,000 per person. If you're a married couple filing jointly, that protection doubles to $100,000. To see if you're safe, you just need to calculate your equity. Take the current market value of your home and subtract your mortgage balance. If that number is less than your exemption limit, the trustee can't sell your house to pay creditors. This is the primary way of keeping your house during bankruptcy while still getting the relief you need.

Personal Property and the Wildcard "Catch-All"

Beyond your home, the law provides specific buckets of protection for your daily life. Your car is protected up to $3,600 in equity per person. If you use certain equipment for your job, the "tools of the trade" exemption covers up to $2,250. But the most flexible tool is the "wildcard" exemption. This is a $4,000 credit that you can apply to any personal property you choose, whether it's money in a bank account, a family heirloom, or high-end electronics. If you're unsure how these limits apply to your specific situation, a quick conversation with a professional bankruptcy attorney can help you maximize these protections. There's even a new 2026 provision that protects household goods and pets, provided no single item is worth more than $5,000 in resale value. By stacking these exemptions strategically, most residents find they don't actually lose any of their personal belongings.

Chapter 7 vs. Chapter 13: Choosing the Right Protection Strategy

When deciding how to protect my assets during bankruptcy, the choice between Chapter 7 and Chapter 13 is the most critical fork in the road. It isn't just about which one you qualify for based on your income; it's about which structure offers the best defense for your specific property. While Chapter 7 is designed to wipe the slate clean quickly, Chapter 13 acts as a long term shield for assets that might otherwise be vulnerable. The decision often comes down to the amount of equity you have and whether you're behind on your monthly payments.

In a Chapter 7 case, the bankruptcy trustee's primary role is to see if you own anything valuable that isn't protected by the Illinois exemptions we covered. If your equity is within those legal limits, you keep everything. However, if you have a house with significant equity or a luxury vehicle with no loan, a Chapter 7 filing could potentially put those items at risk. This is where a strategic comparison of Chapter 7 vs. Chapter 13 becomes vital. In Chapter 13, you don't lose your property to a trustee. Instead, you pay the value of your non-exempt assets over a three to five year period, allowing you to retain ownership while still resolving your debt in a structured way.

When Chapter 7 is the Safest Bet

For many Illinois residents, Chapter 7 is actually the most efficient path. If your home equity is under the $50,000 mark (or $100,000 for couples) and your personal items fit within the wildcard and vehicle limits, you're looking at what the courts call a "no-asset" case. This means the trustee finds nothing to sell, and you receive your discharge in just a few months. It's the fastest way to reach a fresh start without losing a single possession. You can find more details on this specific process in our guide to Chapter 7 bankruptcy in Illinois.

Using Chapter 13 to Catch Up on Missed Payments

Chapter 13 is often the superior choice for homeowners who have fallen behind on their mortgage or car notes. While the automatic stay stops a foreclosure, only a Chapter 13 plan allows you to "cure" those missed payments over several years. It's a reorganization that protects your home and other high-value assets by rolling your arrears into one manageable monthly payment. If you're wondering how to protect my assets during bankruptcy when you're facing a looming sheriff's sale, Chapter 13 provides the legal framework to stop the clock and keep your keys. It's a marathon rather than a sprint, but it offers a level of security for your primary residence that a Chapter 7 simply cannot match.

Avoiding Common Pitfalls That Put Your Assets in Jeopardy

When you're under the weight of mounting debt, it’s natural to want to "clean up" your finances before the court sees them. However, many well intentioned people end up causing the very problems they were trying to avoid. If you are researching how to protect my assets during bankruptcy, the most important rule is to stop moving things around. Actions that feel like common sense, such as paying back a personal loan to a family member or selling a vehicle to a friend for a few hundred dollars, are often seen as red flags by the bankruptcy trustee. These are known as preferential or fraudulent transfers, and they can lead to the court undoing your transactions and seizing the property anyway.

A preferential transfer happens when you favor one creditor over others, like paying back your sister for a loan while ignoring your credit card bills. In Illinois, the trustee can look back up to one year for payments made to "insiders" like family members. If they find these payments, they have the power to sue your relative to get that money back so it can be distributed among your other creditors. Similarly, selling an asset for significantly less than it’s worth is considered a fraudulent transfer. The trustee doesn't have to prove you were trying to lie; they only have to show that you didn't receive "reasonably equivalent value" for the item. This is why transparency is your best defense in court.

The "Don’t Touch That" Phase Before Filing

The moment you decide to file, you should treat your bank accounts and asset titles as if they are frozen. Moving large sums of money between accounts or changing the name on a deed creates a paper trail that is difficult to explain later. Illinois trustees are very thorough during the look back period, which often extends back two years for general asset transfers. If you've already made a transfer you're worried about, don't panic. It's much better to consult with a bankruptcy professional to disclose and address the issue properly before your paperwork is submitted to the court.

Full Disclosure: Why Honesty is the Best Asset Protection

Some people believe they can protect an asset simply by not mentioning it on their schedules. This is a dangerous gamble that rarely pays off. Trustees have access to sophisticated databases that track property records, bank accounts, and even previous tax returns. If you "forget" to list a boat, a secondary bank account, or a potential personal injury claim, you risk more than just losing that asset. The court can deny your entire discharge, meaning you'll still owe all your debt but will have lost the legal protections of bankruptcy. In extreme cases, hiding assets can even lead to criminal charges. Being completely honest with your attorney and the court ensures that we can use the exemptions we discussed earlier to protect your property the right way, without the risk of legal blowback.

How a Northbrook Bankruptcy Attorney Secures Your Future

While understanding the updated 2026 laws is a great first step, applying those rules in the Northern District of Illinois requires a more nuanced approach. Every bankruptcy trustee in the Chicago area has their own specific way of evaluating property values and lifestyle expenses. This is why local expertise is so vital. A Northbrook bankruptcy attorney doesn't just fill out your paperwork; they act as a strategic advisor who understands how local courts interpret the latest exemption updates. If you're still trying to figure out how to protect my assets during bankruptcy, a personalized plan is what bridges the gap between reading about the law and actually keeping your property safe.

One of the most valuable roles an attorney plays is acting as your advocate during the Meeting of Creditors, also known as the 341 meeting. This is the part of the process where the trustee asks you questions under oath about your assets and your filing. Having a professional by your side ensures that your exemptions are presented correctly and that any complex property issues are handled with precision. This advocacy turns a potentially high-stress court requirement into a routine step toward your financial recovery. Our goal is to move you from a state of financial crisis to a stable, asset-protected future where you can finally breathe again.

Strategic Planning Before You File

The real work happens long before we walk into a courtroom. We start by performing a comprehensive analysis of your debt-to-asset ratio to determine which Chapter provides the most robust protection for your specific situation. This includes pre-filing audits to ensure all exemptions are maximized and that no red flags, like the preferential transfers we discussed earlier, are left unaddressed. Fridman Legal has extensive experience handling complex asset cases, ensuring that even high-value property is shielded within the full extent of the law. We look at the big picture to make sure your filing is a strategic success, not just a temporary fix.

Your Next Steps Toward Financial Stability

Taking the first step toward debt relief can feel heavy, but it's where your peace of mind begins. During your first consultation, we'll sit down and look at your specific goals. Whether you are trying to save a family home in the suburbs or protect a professional practice, we'll build a strategy tailored to you. You'll walk away with a clear roadmap and the confidence that comes with a professional legal strategy. If you're ready to put the stress of debt behind you and secure your belongings, please contact us for a consultation. We are here to help you navigate how to protect my assets during bankruptcy and get you back on solid ground.

Secure Your Assets and Reclaim Your Financial Freedom

Navigating the bankruptcy process doesn't have to mean starting from zero. We've seen how the 2026 Illinois exemption updates provide a significant safety net for your home and personal property. By choosing the right filing chapter and avoiding common pre-filing mistakes, you can move toward a debt-free life without losing the things that matter most. If you're still feeling uncertain about how to protect my assets during bankruptcy, the best thing you can do is get a professional perspective tailored to your specific situation.

O. Allan Fridman brings nearly 20 years of local bankruptcy experience to every case; providing the personalized representation you need in the Chicago area courts. We offer clear, flat-fee options for Chapter 7 filings, so you'll know exactly what to expect from the start. You don't have to face this transition alone or wonder if your property is truly safe. Protect your assets and start fresh; schedule a consultation with Fridman Legal today. Taking this step is the first move toward a stable and predictable financial future.

Frequently Asked Questions

Can I keep my wedding ring if I file for bankruptcy in Illinois?

Yes, you can almost always keep your wedding ring. Illinois law provides a specific exemption for necessary wearing apparel, and most wedding bands fall well within these protections. If you own an exceptionally high value ring, we can use the $4,000 wildcard exemption to cover any remaining equity. It is very rare for a trustee to pursue a wedding ring unless its resale value is truly extraordinary.

What happens to my 401(k) or IRA during bankruptcy?

Your retirement accounts are generally 100% protected from creditors. ERISA qualified plans like 401(k)s and most IRAs are fully exempt under both state and federal guidelines. This ensures you don't have to worry about your future security while resolving your current debts. Just make sure you don't withdraw the money before filing; once that cash is in a standard bank account, it loses its protected status.

Will I lose my car if I am still making payments on it?

You won't lose your car as long as you stay current on your loan payments and your equity is within legal limits. The 2026 Illinois motor vehicle exemption protects up to $3,600 of equity per person. If you are still making payments and have little to no equity, the trustee has no incentive to take the vehicle. You will simply continue your payments through a reaffirmation agreement or a Chapter 13 plan.

Can the court take my tax refund if I file for bankruptcy?

The court can potentially take your tax refund if it isn't protected by an exemption. Since a refund is considered a financial asset, we often use the $4,000 wildcard exemption to shield it. Timing your filing is crucial here. If you've already received and spent the refund on necessary living expenses like rent or groceries before filing, there is nothing for the trustee to collect.

Is there a limit on how much cash I can have in my bank account?

Illinois law now provides an automatic $1,000 exemption for funds in a bank account as of January 1, 2026. If you have more than that, you can apply your wildcard exemption to protect the remaining balance. This is a vital part of how to protect my assets during bankruptcy because it ensures you have liquid cash available for immediate needs like utilities and food after your case begins.

What is the "Wildcard Exemption" and how do I use it?

The wildcard exemption is a $4,000 catch-all credit that you can apply to any property you own. You can use it to save extra equity in a vehicle, protect cash in the bank, or keep family heirlooms that don't fit into other categories. It is incredibly flexible. For married couples filing jointly, this protection doubles to $8,000, providing a significant buffer for your personal belongings.

Does filing for bankruptcy stop a wage garnishment immediately?

Filing for bankruptcy stops wage garnishments the moment your case is filed. The automatic stay legally requires your employer to stop withholding funds for creditors immediately. If a garnishment continues after your filing date, the creditor may be required to return those funds to you. This provides instant relief to your take-home pay, allowing you to manage your daily expenses more effectively while your case proceeds.

Can I keep my home if it has a lot of equity?

If your home has equity significantly higher than the $50,000 homestead exemption, a Chapter 13 filing is usually the best strategy. In a Chapter 7 case, a trustee might sell a high equity home to pay creditors. However, in Chapter 13, you keep the house and pay the value of the unprotected equity over a three to five year plan. This is the most reliable method for how to protect my assets during bankruptcy when your home value has increased substantially.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.