What if the day you received your discharge papers wasn't the end of your financial life, but the most strategic reset button you've ever pressed? It's completely normal to feel a bit of lingering stress about whether you're "blacklisted" from the Chicago housing market or if creditors will find a way to come back. You've likely spent months wondering which debts are officially off the books and if you'll ever see a 700 credit score again. Dealing with the uncertainty of life after bankruptcy discharge in Illinois can be exhausting, but the reality is much more optimistic than the rumors suggest.

This guide is here to provide the clarity you need to move forward with total confidence. We'll show you exactly how to rebuild your credit from the ground up, the specific timelines you need to know for qualifying for a mortgage under 2026 regulations, and the steps to ensure your financial freedom is permanent. You're about to discover a clear roadmap that turns your discharge into a genuine fresh start, allowing you to secure your home and your family's future in the Illinois area without the weight of the past holding you back.

Key Takeaways

- Understand how your discharge acts as a permanent legal shield, ensuring creditors can never legally contact you about those old debts again.

- Get the 24-month roadmap to hitting a 700 credit score as you navigate life after bankruptcy discharge Illinois by using credit strategically.

- Find out when you can realistically qualify for a mortgage or a car loan in the Chicago area without being held back by your filing history.

- Learn how to build a safety net fund that prevents you from ever needing to rely on high-interest debt during a future emergency.

- Discover why staying connected with your legal team in Northbrook helps you handle any post-discharge hurdles with total confidence.

The Immediate Aftermath: What Your Discharge Order Actually Changes

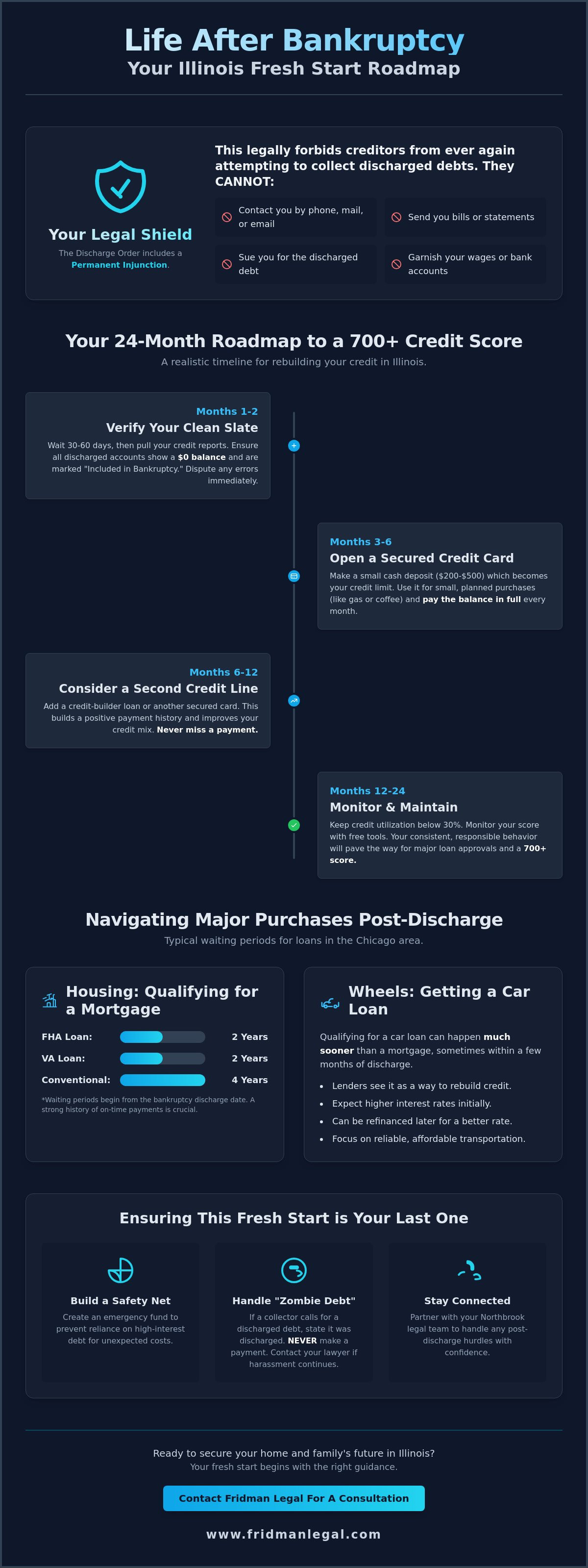

The day your discharge order arrives, the ground shifts beneath your feet. It's not just a formal conclusion to a court case; it's a permanent legal shield that completely alters your financial reality. This order includes a "Permanent Injunction," which is a court mandate that forbids creditors from contacting you, sending bills, or attempting any form of collection for the rest of your life regarding those specific debts. To understand the full scope of this protection, it helps to look at What a Bankruptcy Discharge Means in a broader legal context. Essentially, the court has stripped those creditors of their power to sue you, garnish your wages, or even send you a polite reminder letter.

You should treat your physical discharge papers like a birth certificate or a deed. Keep them in a safe, accessible spot, perhaps a fireproof box or a secure digital cloud. You'll likely need these documents when you apply for a mortgage or a car loan later on, as lenders will want to see proof that your previous obligations were officially wiped out. Having them ready saves you from a frantic search when you're in the middle of a major purchase.

However, it's vital to identify the "survivors." Bankruptcy is a powerful tool, but it's not a magic wand for every single liability. Most student loans, recent tax debts, and domestic support obligations like child support will remain on your plate. Distinguishing between what's gone and what stays is a huge part of managing life after bankruptcy discharge in Illinois effectively. You don't want to be blindsided by a debt you thought was erased.

Verifying Your Clean Slate on Credit Reports

Patience is your best friend here. You might feel an urge to check your score the minute the judge signs the paper, but you should actually wait 30 to 60 days. This window allows the credit bureaus time to process the court's data. When you do pull your report, look for two things on every discharged account: a balance of exactly zero and a status that says "included in bankruptcy." If a creditor in Illinois is being stubborn and refuses to update their reporting, you have the right to dispute it formally. Accuracy at this stage is the foundation of your future 700+ score.

Handling the 'Zombie Debt' Collectors

Occasionally, a collection agency might try their luck by calling you about a discharged medical bill. This is what's known as "zombie debt." If this happens, don't panic and, whatever you do, never make a "good faith" payment. Even a five dollar payment can complicate your legal protections and potentially restart statutes of limitations. Instead, tell them the debt was discharged and provide your case number. If the harassment continues, your bankruptcy lawyer can step in to enforce the court's injunction. Most collectors back off quickly once they realize you're represented by counsel who knows the rules of life after bankruptcy discharge in Illinois.

Your 24-Month Roadmap to Rebuilding an Illinois Credit Score

It might seem strange to think about borrowing money immediately after you've cleared your slate, but the credit bureaus need current data to judge your reliability. Staying away from credit entirely is actually a mistake. To see real progress in your life after bankruptcy discharge in Illinois, you have to show that you can manage modern financial tools responsibly. Your goal is to reach a 700 score within two years of your filing. This is a very realistic target if you follow a disciplined plan and stay consistent with your monthly habits.

Monitoring your progress is easier than ever in 2026. Use free tools that provide "soft" inquiries, so your score doesn't take a hit every time you check it. While your score matters, lenders also look closely at your debt-to-income ratio. This ratio becomes your new North Star. By keeping your fixed costs low and your available credit high, you signal to banks that you aren't at risk of overextending yourself again. This transition is a core part of the process outlined in the U.S. Bankruptcy Code, which aims to give you a genuine opportunity for a fresh start.

The Secured Credit Card Strategy

Think of a secured card as training wheels for your new financial life. You provide a cash deposit, which serves as your credit limit. It's essential to choose a card that reports to all three major bureaus: Equifax, Experian, and TransUnion. Follow the "10% Rule" strictly. If your limit is $500, never let your statement balance exceed $50. Pay it off in full every single month. This shows a perfect payment history without the risk of falling back into high-interest traps. It's about demonstrating restraint, not just the ability to pay.

Credit Builder Loans and Small Installments

Credit scores thrive on a "credit mix." Having only credit cards isn't enough; you also need installment history to prove you can handle fixed monthly obligations. Credit builder loans are perfect for this. You make small monthly payments into a locked savings account, and the lender reports those on-time payments to the bureaus. Once the loan is "paid off," you get the money back. This builds your score and an emergency fund simultaneously. Watch out for subprime lenders who target recent filers with high-fee cards. You don't need to pay hundreds in annual fees to rebuild your reputation. If you ever feel unsure about a specific financial offer, consulting with a legal professional can help you avoid predatory terms that might derail your progress.

Housing and Wheels: Navigating Major Purchases in the Chicago Area

One of the most persistent myths about life after bankruptcy discharge in Illinois is that you'll be locked out of major purchases for a decade. The reality is far more practical. Car dealerships in suburbs like Northbrook and across the Chicago area are often quite eager to work with post-discharge buyers. From their perspective, you're actually a lower risk because your old debts have been legally erased and you're barred from filing for bankruptcy again for several years. You've essentially been "de-leveraged," which makes you a candidate for new credit, provided you're willing to navigate the initial cost of entry.

You should expect higher interest rates at first. As of May 2026, subprime auto loans for those with a recent discharge typically carry APRs between 19% and 24%. While this is significantly higher than the rates offered to prime borrowers, it isn't a permanent sentence. The strategy here is to view this first post-bankruptcy loan as a tool. If you take the loan, manage it perfectly for 12 to 18 months, and continue rebuilding your score as we discussed in the roadmap section, you can often refinance into a much more reasonable rate later on.

Renting in Illinois requires a similarly proactive approach. Most landlords will run a background check and see the filing. Instead of hoping they don't notice, it's better to be upfront. Bring your discharge papers and proof of your current income to the showing. Showing a landlord that you have no remaining debt and a stable job often carries more weight than a credit score that's still in recovery. Many property managers in the Chicago area are willing to overlook a bankruptcy if you can demonstrate that your current financial house is in order.

Mortgage Waiting Periods: FHA vs. Conventional

Buying a home is a matter of timing and meeting specific regulatory milestones. Under current 2026 guidelines, you can generally qualify for an FHA or VA loan just two years after a Chapter 7 discharge, provided you've maintained perfect credit since the filing. Conventional loans are more rigorous, typically requiring a four-year wait and a higher credit score. As of May 2026, the average 30-year fixed mortgage rate in Illinois is approximately 6.5%. While your rate might be slightly higher, having real estate lawyers to manage your closing ensures that your interests are protected as you reclaim this piece of the American dream.

Financing a Reliable Vehicle

If your current vehicle is reliable, try to wait at least six months post-discharge before seeking a new loan. This brief window allows your credit rebuilding efforts to start showing up on your reports, which can help you stay on the lower end of that 19% to 24% interest range. A down payment is essential; it reduces your total interest cost and signals to the lender that you're invested in the deal. Stay away from "Buy Here Pay Here" lots. They often charge predatory fees and rarely report your on-time payments to the bureaus, meaning you're paying a premium without getting the credit-boosting benefits you need.

New Habits: Ensuring This Fresh Start is Your Last One

The true success of life after bankruptcy discharge in Illinois isn't found in the court documents; it's built in the quiet moments when you decide how to handle your next paycheck. For years, you've likely felt like you were "paying for the past," watching money disappear into interest payments for things you bought a lifetime ago. Now, the psychological shift moves toward "saving for the future." Your first priority is building an "In Case of Emergency" fund. This isn't just a savings account; it's your primary defense against ever needing high-interest credit again. If your car breaks down or a medical bill arrives, you pay cash. The cycle of debt stops because you've built a wall around your financial peace.

Automating your finances is another foundational habit. Set up automatic transfers for your savings and auto-pay for every utility and new credit account. This ensures your bills are never late, which protects your newly recovering credit score without requiring you to remember dozens of due dates. Once you've stabilized your daily cash flow, it's the perfect time to revisit your estate planning. Now that your debts are cleared, you can focus on securing what you're building for the next generation without the shadow of creditors hanging over your assets.

Creating a Realistic 2026 Budget

In 2026, you don't need a complex spreadsheet to stay on track. Modern budgeting apps can link directly to your accounts, tracking every dollar without it feeling like a chore. The key to a sustainable plan, especially with the higher cost of living in Chicago suburbs like Glenview or Wilmette, is balance. Allocate a specific amount for "fun money" each month. If you try to live on a "financial diet" that's too restrictive, you're more likely to experience burnout, which often leads to impulsive spending. A budget should feel like a plan for what you can do, not just a list of what you can't.

The Power of Saying 'No' to New Debt

Prepare yourself for a flood of mail. Within weeks of your discharge, predatory lenders will start sending you "pre-approved" offers for high-interest credit cards. They know you have no other debt and can't file for bankruptcy again soon. You have to learn to distinguish between a "tool" and a "trap." A secured card used for small purchases is a tool; a 29% APR store card for a new television is a trap. Staying disciplined when these offers look tempting is what separates a temporary fix from a permanent lifestyle change. If you're ready to take the next step in protecting your new financial life, reach out to us today to discuss how we can support your long-term goals.

Why Partnering with a Northbrook Bankruptcy Attorney Matters

Your relationship with Fridman Legal doesn't have to end just because the judge signed your papers. Many people think of their attorney as someone who only handles the immediate crisis, but we see ourselves as your long-term strategic partners. Navigating life after bankruptcy discharge in Illinois involves more than just ignoring old phone calls. It's about having a professional advocate who understands the specific quirks of the Northern District of Illinois court system. Whether you're dealing with a stubborn creditor who refuses to acknowledge your discharge or you're planning your next big financial move, having someone who knows your history and the law is invaluable.

We focus on helping you transition from the survival mode of debt relief to the strategic phase of asset protection and growth. The peace of mind that comes from knowing a professional is just a phone call away cannot be overstated. You've worked hard to reach this fresh start. Now, you need to ensure that every decision you make strengthens your new financial foundation. We're here to provide that stability, ensuring that the legal shield we've built together remains impenetrable as you move forward.

A Personalized Approach to Debt Relief

O. Allan Fridman focuses on results-driven solutions specifically tailored for Northbrook families. We understand that every situation is unique, which is why we don't offer cookie-cutter advice. One of the ways we reduce your stress is through a transparent flat-fee structure. You won't have to worry about hidden costs or escalating bills while you're trying to rebuild. By integrating our Chapter 7 expertise with your long-term goals, we ensure that your discharge is the launchpad for a much larger success story. It's about more than just clearing debt; it's about setting the stage for your future prosperity.

Taking the Next Step Toward Freedom

We encourage you to reach out with any post-discharge questions or concerns that might pop up. Whether you're looking into residential real estate closings or starting a new commercial venture, we're here to help you navigate the legal complexities. 2026 is the perfect year to reclaim your financial narrative and move forward with total confidence. You've cleared the hurdles; now it's time to build the life you've planned. If you're ready to discuss your next chapter in real estate or business, contact us to schedule a follow-up. We look forward to seeing where your fresh start takes you and helping you protect the assets you're about to build.

Start Building Your New Financial Legacy

Your discharge is much more than a set of court papers; it's the foundation of a life where you finally control your financial destiny. By using your discharge order as a legal shield and following a clear roadmap to a 700 credit score, you're setting yourself up for long-term success. Remember that major purchases like a home or a car are still within reach if you stay patient and consistent with your new habits. Life after bankruptcy discharge in Illinois is about moving from a place of survival to a place of strategic growth.

Fridman Legal brings nearly 20 years of Illinois legal experience and deep roots in the Northbrook and Chicago community to your corner. We offer personalized, flat-fee bankruptcy services designed to help you reclaim your narrative without hidden costs or extra stress. You've already done the hard work of seeking a reset. Now, let's work together to ensure your fresh start is permanent. Ready for a fresh start? Contact Fridman Legal today for a consultation. You deserve a future defined by freedom rather than debt.

Common Questions About Life After Bankruptcy

How long does a bankruptcy discharge stay on my credit report in Illinois?

A Chapter 7 bankruptcy remains on your credit report for 10 years from the date you filed your petition. If you filed for Chapter 13, the record typically drops off after seven years. While these dates are fixed, their impact on your score lessens significantly as time passes and you build a fresh history of on-time payments. Most lenders care more about your recent habits than a filing from several years ago.

Can I get a credit card immediately after my Chapter 7 discharge?

Yes, you can apply for a credit card the moment your discharge is official. In fact, you'll likely see "pre-approved" offers arriving in your mailbox within weeks of your case closing. Starting with a secured credit card is often the smartest move for life after bankruptcy discharge in Illinois because it allows you to rebuild your score without the risk of high-interest unsecured debt.

Will my employer find out that I filed for bankruptcy?

Your employer is not typically notified by the court when you receive a discharge. Unless you are in a Chapter 13 plan that requires a wage deduction order, your workplace won't be involved in the process. While bankruptcy is a matter of public record, most employers in the Chicago area don't actively monitor court filings unless you're applying for a high-level financial or security-clearance position.

Can I keep my tax refund after I receive my bankruptcy discharge?

You can usually keep your tax refund if it's protected by your available Illinois exemptions. The state's $4,000 wildcard exemption is often used to shield cash assets like refunds. If the refund is for money you earned after your filing date, it's generally considered your property and isn't part of the bankruptcy estate. Your attorney can help you calculate exactly how much you can protect before you file.

When is the earliest I can qualify for an FHA home loan in Chicago?

You can qualify for an FHA mortgage exactly two years after your Chapter 7 discharge date. This two-year waiting period is a standard requirement, provided you've maintained perfect credit and haven't missed any payments since your case was filed. For those in a Chapter 13, you might even qualify while still in your payment plan, as long as you've made 12 months of on-time payments and have court approval.

What happens if a creditor tries to sue me for a debt that was discharged?

If a creditor attempts to sue you for a debt that was wiped out, they are in direct violation of a federal court order. The "permanent injunction" created by your discharge legally forbids them from taking any collection action. You should contact your legal team immediately if this happens. The court can sanction the creditor and force them to pay for any damages or legal fees caused by their illegal collection efforts.

Can I buy a car while I am still waiting for my final discharge papers?

You can technically buy a car before your discharge, but your options will be much better if you wait. Most reputable lenders in the Chicago suburbs prefer to see the final discharge order before they'll approve a loan. If you're in an active Chapter 13 case, you'll need to get formal permission from the bankruptcy trustee to take on any new debt over a certain threshold, which adds another layer of paperwork.

Is it possible to remove a bankruptcy from my credit report early?

No, there is no legal way to remove a legitimate bankruptcy filing from your credit report before the seven or 10-year limit expires. Any company claiming they can "erase" a bankruptcy for a fee is likely a scam. The most effective strategy for managing life after bankruptcy discharge in Illinois is to focus on adding positive, new accounts to your report, which naturally dilutes the negative impact of the filing over time.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.