What if the most effective way to secure your Northbrook estate isn't by avoiding debt restructuring, but by mastering the strategic timing of a court-protected reorganization? For many residents in the Chicago metropolitan area, the search for "chapter 13 lawyers near me" often begins only when the threat of foreclosure becomes an imminent reality rather than a distant concern. You likely understand that your home represents years of disciplined investment, yet the persistent pressure from creditors can obscure the clear legal pathways available for asset preservation.

It's exhausting to face the complexity of Illinois bankruptcy exemptions while managing the weight of financial uncertainty. This analysis provides a rigorous comparison between Chapter 13 and alternative debt relief strategies, specifically tailored to the 2026 regulatory environment in Cook County. You'll discover how a structured repayment plan functions as a shield for your property and how to consolidate obligations into a single, predictable monthly payment. We'll examine the precise mechanisms that stop foreclosure proceedings and the strategic advantages of maintaining ownership through professional legal advocacy.

Key Takeaways

- Analyze why Chapter 13 functions as a strategic debt restructuring tool to protect high-value residential assets in Northbrook and Chicago.

- Compare the specific eligibility requirements and asset treatment of Chapter 13 versus Chapter 7 to maximize your use of the Illinois homestead exemption.

- Navigate the mandatory procedural steps and credit counseling requirements unique to the Eastern Division of the Northern District of Illinois.

- Identify the critical differences between boutique legal counsel and high-volume firms when searching for chapter 13 lawyers near me to ensure personalized representation.

- Evaluate how a tailored repayment plan, backed by decades of local experience, provides a secure path to long-term financial stability.

Navigating Debt Relief: Why Search for Chapter 13 Lawyers in Northbrook and Chicago?

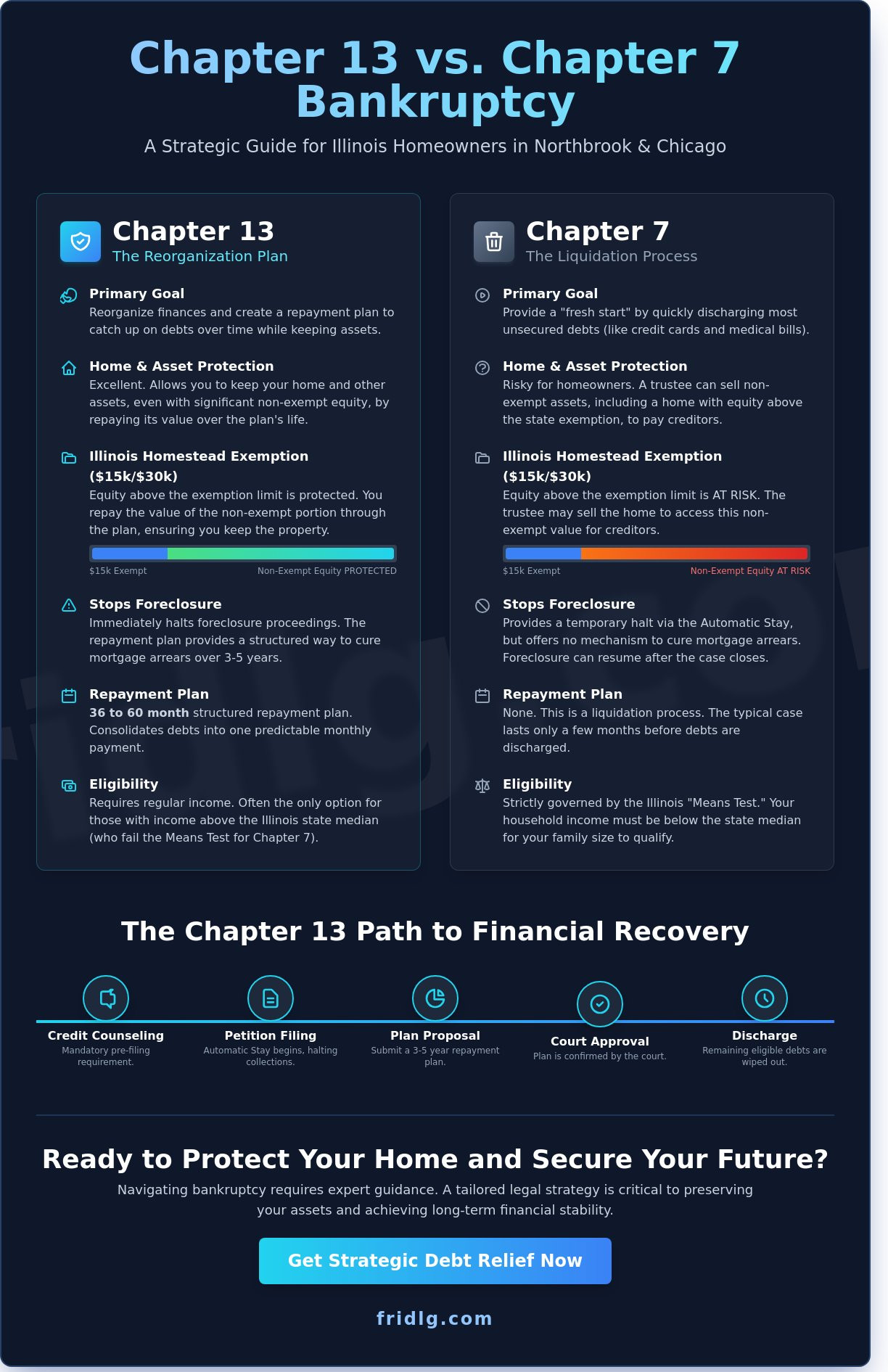

Securing financial stability requires a precise understanding of the available legal frameworks. Chapter 13 of the United States Bankruptcy Code, frequently categorized as a wage earner's plan, enables individuals with regular income to develop a structured proposal to repay all or part of their debts. Unlike the liquidation process of Chapter 7, this mechanism focuses on reorganization and the preservation of assets. For those searching for chapter 13 lawyers near me in the Chicago metropolitan area, the distinction between these two paths often dictates the long-term viability of their personal or business holdings.

The economic projections for 2026 suggest a continued tightening of credit markets in the Chicago suburbs, making proactive debt management essential. The immediate activation of the Automatic Stay provides a critical shield during Cook County foreclosure proceedings. This legal injunction halts collection actions, including phone calls and pending lawsuits, the moment the petition is filed. It's a strategic tool that grants debtors the necessary time to reorganize their finances without the immediate threat of asset seizure.

The Strategic Advantage of Chapter 13 for Illinois Residents

Northbrook property owners often face a unique challenge regarding home equity. The Illinois homestead exemption is currently limited to $15,000 per individual; a figure that many Northbrook residences easily surpass. Chapter 13 allows homeowners to protect this excess equity while curing mortgage arrears through a court-approved repayment plan lasting between 36 and 60 months. This structure is also effective for managing non-dischargeable obligations, such as child support arrears or specific tax debts, by integrating them into a single, manageable monthly payment. The process ensures that priority debts are addressed systematically while preserving the debtor's primary residence.

Common Triggers for Filing in the Chicago Suburbs

The decision to file often stems from urgent external pressures. Sheriff sales and foreclosure auctions in Lake or Cook County represent the most common catalysts for seeking professional counsel. When a home is scheduled for auction, the filing of a Chapter 13 petition can stop the sale, provided the debtor acts before the gavel falls. Additionally, high-income earners in the Chicago suburbs may find themselves ineligible for Chapter 7 due to the Illinois Means Test. The Means Test serves as the primary gateway to bankruptcy eligibility, comparing a household's income against the state median to determine which chapter provides the appropriate path for relief. Experienced chapter 13 lawyers near me ensure that these calculations are precise, preventing the dismissal of a case due to technical errors.

Chapter 13 vs. Chapter 7: Comparing Your Options for Illinois Debt Restructuring

The choice between Chapter 7 and Chapter 13 bankruptcy requires a precise analysis of your current balance sheet and long-term financial objectives. While Chapter 7 focuses on a swift liquidation of unsecured debt; Chapter 13 provides a structured reorganization over a three to five-year period. In Illinois, eligibility for Chapter 7 is strictly governed by the Means Test, which compares your household income against the state median. If your income exceeds this threshold, seeking chapter 13 lawyers near me becomes a strategic necessity to navigate the mandatory repayment requirements.

The Illinois homestead exemption protects up to $15,000 of equity in a primary residence for an individual; this amount doubles to $30,000 for married couples filing jointly. If your home equity surpasses these limits, a Chapter 7 trustee may sell the property to satisfy creditors. Chapter 13 acts as a safeguard in these scenarios. It allows you to retain the property by paying the non-exempt equity portion through your court-approved plan. This mechanism makes Chapter 13 the superior option for homeowners with substantial equity or those facing foreclosure. According to the Chapter 13 Bankruptcy Basics provided by the United States Courts, the process requires a debtor to submit a repayment plan for court approval within 14 days of filing the petition.

Disposable income serves as the foundation for your monthly repayment plan. The court calculates this by subtracting IRS-standardized living expenses from your gross monthly income. The remaining balance is distributed to creditors. This disciplined approach ensures that you only pay what you can realistically afford while maintaining a path toward full debt discharge.

When to Choose Chapter 13 Over Chapter 7

Chapter 13 is particularly effective for protecting assets that do not fall under standard exemptions, such as a luxury vehicle or a secondary investment property. It offers immediate relief from collection actions and can stop repossession of a primary vehicle, allowing you to cure arrears over the plan's duration. In specific cases involving underwater homes, Chapter 13 allows for "lien stripping." This process can remove a second mortgage or HELOC if the home's market value is lower than the balance of the first mortgage, reclassifying the junior debt as unsecured.

The Long-Term Financial Impact

The structural differences between chapters extend to your credit profile. A Chapter 13 filing remains on your credit report for seven years from the filing date, while a Chapter 7 filing persists for ten. This shorter duration reflects the debtor's commitment to partial repayment. There's also a significant psychological benefit to this path; many individuals prefer the integrity of paying back a portion of their obligations rather than total liquidation. For repeat filers, timing is critical. You must verify how often can you file bankruptcy to ensure your current filing will result in a discharge of debt. If you require a sophisticated evaluation of your financial standing, consulting with chapter 13 lawyers near me can provide the clarity needed to proceed with confidence.

The Chapter 13 Process in the Northern District of Illinois: A Step-by-Step Guide

The Eastern Division of the Northern District of Illinois serves as the primary venue for residents of Chicago and surrounding suburbs. Filing here requires strict adherence to local protocols and federal statutes. Before initiating a case, individuals must complete credit counseling from an approved agency within 180 days prior to filing. This prerequisite ensures that all parties have explored alternatives to insolvency before seeking judicial relief. For detailed procedural requirements, the Northern District of Illinois Chapter 13 Information portal provides the necessary regulatory framework for debtors and practitioners.

Approximately 30 to 45 days after filing, you'll attend the Meeting of Creditors, commonly known as the 341 meeting, at the Dirksen Federal Building in downtown Chicago. During this session, the Standing Chapter 13 Trustee examines your financial statements under oath. The Trustee's role isn't to act as a judge; instead, they verify the accuracy of your schedules and ensure the proposed plan meets the legal requirements for confirmation. If you're searching for chapter 13 lawyers near me to facilitate this process, local expertise is vital for navigating these specific administrative hurdles.

From Filing to Confirmation

Your attorney will draft a repayment plan spanning 36 to 60 months, depending on whether your income falls above or below the Illinois median. The confirmation hearing is the final hurdle where a judge determines if your plan is feasible and compliant with the Bankruptcy Code. Success requires a disciplined approach to lifestyle changes. You'll need to adhere to a strict budget, as any discretionary spending is redirected toward debt satisfaction. This period functions as a financial reorganization that demands consistent performance over several years.

Local Court Nuances in Cook and Lake Counties

Judges in the Northern District scrutinize "good faith" by examining the totality of circumstances surrounding your filing. In Cook and Lake Counties, managing local property tax liens is a critical component of the strategy. These liens often take priority and must be addressed within the plan to prevent forfeiture. Local court rules in the Northern District can vary significantly from other jurisdictions. Engaging chapter 13 lawyers near me who understand these regional variations ensures that your filing accounts for local judicial preferences and specific county-level tax protocols.

Evaluating Bankruptcy Attorneys: Beyond the "Near Me" Search in Chicago Suburbs

Most individuals begin their search for debt relief by typing chapter 13 lawyers near me into a search engine. While proximity is convenient, the distinction between a high-volume bankruptcy mill and a boutique Northbrook practice is often the deciding factor in a case's success. Bankruptcy mills prioritize turnover; they process hundreds of filings with minimal attorney-client contact. In a Chapter 13 context, this lack of attention is frequently fatal to the reorganization plan.

Chapter 13 isn't a singular event like Chapter 7. It's a structured, 36 to 60-month financial commitment. This duration requires an advocate who remains accessible long after the initial filing. You'll need a professional who understands the specific nuances of the Northern District of Illinois. Local expertise regarding the preferences of Chicago Trustees and Judges ensures your repayment plan survives the confirmation process without avoidable friction. Securing the right chapter 13 lawyers near me involves looking past the map pins and analyzing their specific track record in the Chicago courts.

Fee structures also vary based on the complexity of the estate. Many firms utilize the "no-look" flat fee established by local rules for standard consumer cases. However, high-net-worth individuals or business owners often require hourly billing for complex litigation, such as lien stripping or valuation disputes. A sophisticated firm provides transparency regarding these costs during the initial strategy session, ensuring no surprises arise during the multi-year plan.

Questions to Ask Your Chapter 13 Lawyer

- How many Chapter 13 plans have you successfully confirmed in the Northern District of Illinois this year?

- Do you handle adversary proceedings internally if a creditor challenges my filing?

- Will the principal attorney handle my 341 meeting of creditors, or is it delegated to a junior associate?

The Role of Technology and Discretion

Modern legal practice demands high-level security and efficiency. Leading firms utilize encrypted secure portals for document collection, ensuring that sensitive financial records remain protected. This discretion is vital for high-net-worth clients in Northbrook who require absolute privacy throughout the restructuring process. If your financial situation doesn't necessitate a court filing, a debt settlement lawyer can offer a private, out-of-court alternative to traditional bankruptcy. This strategic approach allows for debt reduction without the public record associated with a federal filing.

Strategic Debt Relief with Fridman Legal: Protecting Your Northbrook Home and Future

O. Allan Fridman has navigated the complexities of the Illinois bankruptcy courts for over 20 years. This extensive tenure within the Northern District of Illinois provides a distinct advantage for clients seeking structured debt relief. He doesn't rely on automated templates or high-volume processing. Instead, the firm focuses on a disciplined, personalized approach where repayment plans are tailored to your specific 60-month financial trajectory. When searching for qualified chapter 13 lawyers near me, residents of the North Shore require a representative who understands how local judicial preferences impact plan confirmation.

The firm’s unique integration of real estate law ensures a holistic view of your assets. This is particularly vital in Northbrook, where property values require sophisticated protection strategies. By analyzing your home equity through the lens of both bankruptcy exemptions and real estate trends, Fridman Legal creates a shield around your most significant investments. This strategic oversight prevents the common pitfalls that lead to dismissed cases or lost equity.

A Results-Driven Advocacy for Chicago Families

The primary objective at Fridman Legal is the successful confirmation of your reorganization plan. We prioritize home preservation and the systematic elimination of unsecured debt. Our firm maintains a commitment to transparent, flat-fee pricing for bankruptcy petitions, which eliminates the uncertainty of hourly billing during a financial crisis. This clarity allows you to focus on your recovery rather than mounting legal costs. If your financial assessment reveals that your income falls below the state median, a Chapter 7 bankruptcy Illinois filing may be a more efficient alternative to achieve a fresh start.

Next Steps Toward Financial Stability

Securing advocacy from experienced chapter 13 lawyers near me ensures that your petition meets the rigorous standards of the federal court system. Preparation is the foundation of a successful filing. Before your initial meeting, you should organize the following items:

- Tax returns from the last four years to verify filing compliance.

- Pay stubs and income records from the previous six months.

- A comprehensive list of all creditors, including mortgage servicers and medical providers.

- Recent valuations or appraisals of any real estate holdings in Illinois.

A court-protected financial plan provides immediate relief from creditor actions, including wage garnishments and foreclosure proceedings. It's a legally binding framework that replaces chaos with order. To begin the process of reclaiming your financial autonomy, Schedule your consultation with Fridman Legal today at our Northbrook office. We offer the professional discretion and technical expertise necessary to resolve complex debt obligations with precision.

Protecting Your Illinois Property and Financial Sovereignty

Navigating the complexities of the Northern District of Illinois bankruptcy courts requires a methodology that prioritizes long-term stability over temporary relief. While many residents begin their search for chapter 13 lawyers near me looking for simple convenience, the actual value lies in strategic debt restructuring that preserves home equity and halts foreclosure proceedings. It's vital to distinguish between a standard liquidation and the sophisticated repayment plans mandated by the 2026 legal landscape. Success depends on a precise understanding of local court variations and trustee expectations.

Fridman Legal offers a boutique approach where the principal attorney manages every case personally, ensuring your filing reflects nearly 20 years of Illinois bankruptcy experience. Our Northbrook office provides a discreet environment to develop a comprehensive plan that safeguards your family's primary residence. You don't have to navigate these federal mandates without expert support. Professional intervention ensures every exemption is maximized and every creditor's claim is scrutinized for accuracy. Secure your family’s financial future; consult with a Northbrook Chapter 13 expert at Fridman Legal. Taking this first step brings the clarity needed to reclaim control of your financial narrative.

Frequently Asked Questions

Can I keep my home in Northbrook if I file for Chapter 13?

You can retain your Northbrook residence by utilizing the Chapter 13 reorganization process to cure mortgage arrears over time. The Illinois homestead exemption provides $15,000 of protection for individual owners under 735 ILCS 5/12-901. This legal mechanism allows you to maintain possession while restructuring debt into a manageable 60 month schedule. It's a strategic tool for homeowners facing immediate foreclosure threats.

How much does a Chapter 13 lawyer cost in the Chicago area?

Legal fees for Chapter 13 cases in the Northern District of Illinois are typically structured as no-look fees set by the court. The standard flat fee is $4,000 for a consumer case, which covers the duration of the three to five year plan. Engaging chapter 13 lawyers near me ensures that these statutory costs are handled through the repayment plan rather than requiring a large upfront payment.

What is the maximum income to file Chapter 13 in Illinois?

There is no maximum income cap for filing Chapter 13, as this chapter is specifically designed for high earning individuals who don't qualify for Chapter 7. If your household income exceeds the Illinois median, which is $69,380 for a single person as of May 2024, you'll likely file a five year plan. This process provides a disciplined framework for debt satisfaction based on your disposable income.

Will Chapter 13 stop a sheriff sale in Cook County?

Filing a Chapter 13 petition triggers an automatic stay under 11 U.S.C. § 362 that halts a Cook County sheriff sale instantly. This federal injunction stops all foreclosure proceedings, providing a window to restructure your financial obligations. You must ensure the filing is completed before the actual sale occurs. Local chapter 13 lawyers near me can facilitate emergency filings to protect your property interests.

How long does a Chapter 13 repayment plan typically last?

A Chapter 13 repayment plan lasts either 36 or 60 months depending on your income's relation to the state median. Debtors earning above the Illinois median must commit to a five year plan to maximize creditor recovery. This fixed duration ensures a predictable path toward a final discharge. It's a structured timeline that demands strict adherence to the court mandated payment schedule.

Can I discharge tax debt through Chapter 13 in Illinois?

Certain income tax debts are dischargeable if they satisfy the 3-2-240 rule established by the bankruptcy code. The taxes must be from a return due at least three years ago and filed at least two years before your petition. Additionally, the IRS must've assessed the tax at least 240 days prior. This precision is vital for effective tax liability management and strategic financial recovery.

What happens if I miss a payment in my Chapter 13 plan?

Missing a payment results in the Trustee filing a Motion to Dismiss for material default. You typically have 21 days to respond or cure the delinquency before the court terminates your case. If the case is dismissed, you lose the protection of the automatic stay. This allows creditors to resume collection actions, including wage garnishments or foreclosure proceedings, immediately.

Do I have to go to court in downtown Chicago for my bankruptcy?

Most 341 Meetings of Creditors for the Northern District of Illinois are currently conducted via Zoom or teleconference rather than in person. While the Dirksen Federal Building at 219 South Dearborn Street remains the official courthouse, remote proceedings provide a more efficient experience. Your physical presence in downtown Chicago is rarely required for routine matters under current administrative orders.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.