The "safe" choice of a consolidation loan might actually be the riskiest move you can make for your Illinois home in 2026. You probably feel like you are drowning despite making every minimum payment on time, and the constant fear of losing your car or house makes it impossible to plan for the future. It is frustrating to realize that while you work harder, the average debt in Illinois has climbed to over $55,150 per person.

This guide will help you weigh the debt consolidation vs bankruptcy pros and cons Illinois families face so you can choose the most effective path to financial freedom. You deserve a clear strategy that stops the creditor calls and protects your hard-earned assets. We will explore how the major 2026 increases to Illinois homestead and vehicle exemptions have changed the math, making a legal reset more powerful than a high-interest repayment marathon.

Key Takeaways

- Compare the long-term costs of restructuring your debt through a loan versus the immediate relief provided by a court-ordered discharge.

- See how the 2026 Illinois exemption updates allow you to shield significantly more of your home's equity and your personal vehicle from creditors.

- Evaluate the debt consolidation vs bankruptcy pros and cons Illinois homeowners face, including the difference between a quick four-month process and a multi-year repayment cycle.

- Learn how Chapter 13 can specifically stop a foreclosure and provide a structured, legal path to catch up on missed mortgage payments.

- Understand why a customized legal strategy offers more protection against aggressive creditor lawsuits than a generic debt settlement program.

The Debt Crossroads: Understanding Your Illinois Relief Options

Feeling like you're stuck in a loop of minimum payments is a heavy burden. You watch your hard-earned money disappear every month, yet the balances on your credit cards barely budge. It's a cycle that feels impossible to break, especially when you're working hard but seeing no progress. In 2026, managing high-interest consumer debt has become even more complex as interest rates remain stubborn. With the average Illinois resident carrying a debt balance of $55,150, many people are reaching a breaking point. This is why understanding the debt consolidation vs bankruptcy pros and cons Illinois families face is so important right now. It isn't about failing or making a moral mistake; it's a simple math problem that requires a strategic solution to protect your future and your home.

What Exactly is Debt Consolidation?

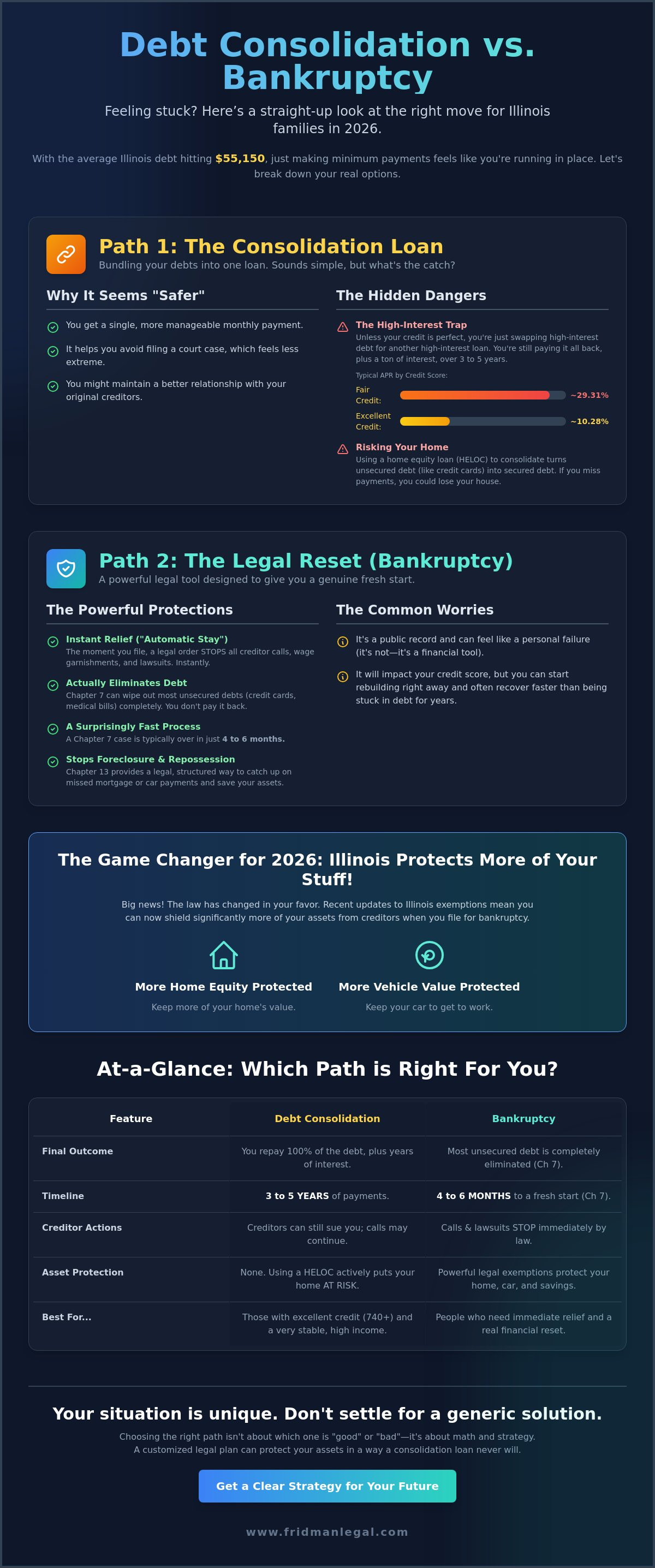

Debt consolidation is essentially a way to group several high-interest debts into a single, more manageable monthly payment. For many, this involves taking out a new loan to pay off old credit cards. You might also consider a debt management plan where a third party negotiates with creditors on your behalf. However, this path relies heavily on your credit score and a very steady income. According to this Debt Consolidation Overview, the goal is often to secure a lower interest rate, but that's not always a reality in the current market. If your credit score is in the "fair" range, which is 580 to 669, you might see APRs as high as 29.31%. If you can't get a rate significantly lower than what you're currently paying, consolidation might just be moving debt from one pocket to another without actually solving the root issue.

The Basics of Bankruptcy in Illinois

Bankruptcy is a federal legal process designed to give people a fresh start when their debt becomes truly unmanageable. It isn't a one-size-fits-all solution. Chapter 7 is often a faster route, taking about four to six months, where most of your unsecured debts like medical bills and credit cards are wiped out entirely. Chapter 13 works differently. It allows you to reorganize your debt into a three to five-year payment plan, which is often used to save a home from foreclosure. One of the biggest advantages of filing is the "Automatic Stay." This is a powerful legal order that forces creditors to stop all collection actions, phone calls, and even lawsuits immediately. It provides the breathing room you need to finally stop the stress. If you're curious about which chapter fits your specific needs, exploring our bankruptcy services can help clarify how these laws protect your assets.

Debt Consolidation in Illinois: The Pros and Cons

Most people lean toward consolidation because they want to protect their credit score. It feels like the safer bet. You keep your accounts open, avoid a court record, and maintain a sense of control. But when we look at the debt consolidation vs bankruptcy pros and cons Illinois borrowers deal with, the math often tells a different story. Consolidation means you're paying back every cent, plus interest. If your credit score has already dipped into the "Fair" range, which covers scores from 580 to 669, you could be looking at an APR of 29.31%. That is a massive amount of interest to pay just to avoid a filing. You might find that you're working just to keep the bank happy while your actual debt barely shrinks over time.

There is also a significant risk if you use your home as collateral through a HELOC. Turning credit card debt into a mortgage-backed loan is dangerous. If life takes a turn and you miss payments, your house is on the line. You should also distinguish consolidation from debt settlement. In settlement, you stop paying creditors to force a deal. While you might pay less, the IRS often views the forgiven amount as taxable income. You could easily trade a credit card bill for a surprise tax bill at the end of the year. For a deeper look at your legal rights in these situations, the Illinois Bankruptcy Guide provides excellent context on how state laws protect you differently than a private loan agreement would.

When Consolidation Makes Sense

Consolidation works best if you have a credit score above 740 and can snag a low interest rate, like the 10.28% average for those with excellent credit. It requires a rock-solid three to five year plan and a stable job, particularly in competitive areas like Chicago or Northbrook. If you have the discipline to cut up the cards and a high enough income to cover the new monthly payment without stress, it can be a great tool. If you aren't sure where you stand, looking into debt negotiation and settlement options might provide a clearer picture of your alternatives before you sign a new loan agreement.

The Hidden Traps of Consolidation Loans

The biggest danger is the "re-loading" trap. You pay off your cards with a loan, feel a sense of relief, and then start using those same cards again for daily expenses or emergencies. Within a year, you have a consolidation loan payment and new credit card balances to juggle. Many Illinois residents find themselves in this exact spot, eventually needing to file for bankruptcy anyway after wasting years on interest payments. Watch out for teaser rates as well. That low monthly payment might jump significantly after the first 12 months, leaving you in a worse position than when you started.

Filing Bankruptcy in Illinois: Clearing the Air

A common misconception is that bankruptcy is a sign of personal failure. In reality, it's a powerful legal tool designed for the exact same reason businesses use it: to restructure and survive. When you're looking at the debt consolidation vs bankruptcy pros and cons Illinois residents face, the most immediate benefit of bankruptcy is the legal protection it provides. The moment your case is filed, the court issues an "Automatic Stay." This isn't just a polite request; it's a federal order that forces creditors to stop all collection activities. If you're facing wage garnishments or a pending lawsuit, those actions freeze instantly. It gives you the breathing room to actually think about your future instead of just reacting to the next bill.

While some financial advisors highlight the Pros and Cons of Debt Consolidation, they often overlook the "Strategic Bankruptcy" approach. Consolidation keeps you in the debt cycle for years, often at high interest rates. Bankruptcy can offer a much faster path to a clean slate. You might also worry about your credit, but the truth is that a discharge can actually be the first step in rebuilding. It's much easier to improve a credit score when you no longer have a debt-to-income ratio that's off the charts. If you want to explore how this applies to your specific assets, our bankruptcy services page breaks down the protections available to you.

Chapter 7: The True Fresh Start

Chapter 7 is what most people think of when they hear "bankruptcy." It's a liquidation process that wipes out most unsecured debts, including credit cards, personal loans, and medical bills. To qualify in Illinois, you'll need to pass a "Means Test," which compares your income to the state median. If your income is below the threshold, you can typically move through the process in about four to six months. For residents in the North Shore area, this Chapter 7 Bankruptcy in Northbrook guide provides a detailed look at how local courts handle these filings and what you can expect during your 2026 filing.

Chapter 13: The Repayment Shield

If you have a steady income but have fallen behind on your mortgage or car payments, Chapter 13 is often the better choice. It doesn't wipe debt away instantly; instead, it reorganizes it into a three to five-year plan. This is especially vital for homeowners in Northbrook or Chicago who want to save their property from foreclosure. The court supervises your payments, and in many cases, you only pay back a small fraction of what you owe to unsecured creditors. It's a structured, legal way to catch up on arrears while keeping the assets you've worked so hard to build.

The Side-by-Side Comparison: Illinois Pros and Cons

When you look at the clock and your bank balance, the differences between these two paths become very clear. The most striking contrast is the timeline. A typical Chapter 7 bankruptcy in Illinois moves from filing to discharge in about four to six months. In that short window, your legal obligation to pay unsecured debt is gone. On the other hand, a consolidation loan is a commitment to a three to five year marathon. You're betting that your income will stay perfectly stable for half a decade while you pay back 100% of the principal plus interest. When evaluating the debt consolidation vs bankruptcy pros and cons Illinois residents must consider, you have to ask if you'd rather spend one season or five years resolving the issue.

The cost difference is equally significant. With consolidation, you are often paying back significantly more than you originally borrowed due to interest rates that can reach 29.31% for fair credit. Bankruptcy often results in paying back between 0% and 10% of unsecured debt. Most importantly, bankruptcy provides the shield of Federal Court protection. If a creditor tries to sue you during a consolidation plan, you have no automatic legal defense. In bankruptcy, the court stops those lawsuits cold. If you are tired of the uncertainty, you might want to contact our office to discuss a more secure legal strategy.

Asset Protection: The Illinois Advantage

One of the biggest gaps in national financial advice is the failure to mention state-specific protections. As of January 1, 2026, Illinois has significantly increased its homestead exemption. You can now protect up to $50,000 of equity in your home, or $100,000 if you own it jointly with a spouse. This means most homeowners can file for bankruptcy without any fear of losing their house. You also have a $3,600 exemption for your car and a $4,000 "wildcard" exemption for any other personal property. Debt consolidation offers none of these legal guarantees; it is simply a contract that provides zero protection for your assets if you fall behind again.

Credit Score Recovery: The Surprising Truth

You might worry that bankruptcy will destroy your credit forever, but the reality is often the opposite. Many people see their credit scores begin to rise within a year of their discharge because their debt-to-income ratio has been reset. While bankruptcy marks your report, it also clears the path to rebuild; unlike a mountain of debt that keeps you stagnant for years. In a consolidation plan, a single missed payment can tank your score all over again, leaving you right back where you started but with even more interest accumulated.

Choosing Your Path: Why a Local Northbrook Attorney is Vital

Deciding between these two paths is a major life decision, but you don't have to make it in a vacuum. Many people try the DIY route by signing up for an online consolidation loan or a national debt settlement program, only to realize these companies have no legal power in an Illinois courtroom. When a creditor decides to sue or garnish your wages, a cookie-cutter loan won't stop them. This is where the debt consolidation vs bankruptcy pros and cons Illinois comparison becomes very practical. You need a strategy that actually works under Illinois law, not a generic plan designed for a different state.

The reality is that many debt relief companies are essentially sales organizations. They want to sell you a product, whether it's a high-interest loan or a settlement plan that might leave you with a massive tax bill or a lawsuit. At Fridman Legal, we take a different approach. We look at the legal framework of your specific situation to see how we can protect your home, your car, and your future. You shouldn't have to guess which option is best when your financial stability is on the line. We handle the heavy lifting, including the aggressive creditor calls that have been keeping you up at night.

Strategic Debt Relief in the Chicago Suburbs

Living in the Chicago suburbs means you need a representative who understands the local economic climate and the specific procedural nuances of the Cook County and Lake County courts. Working with a Strategic Bankruptcy Lawyer in Chicago means having someone who knows how local trustees and judges view certain assets. We don't just look at your balances; we look at your whole life. For some, a Debt Settlement approach might be the right middle ground if a full bankruptcy filing isn't the best fit for your current goals. We act as your shield, taking over all communication with your creditors so you can focus on moving forward.

Your First Step Toward Peace of Mind

When you come in for a consultation at Fridman Legal, we sit down and look at the numbers together. We'll walk through your assets, your income, and your long-term goals to see which path leads to genuine peace of mind. To make things as transparent as possible, we use a flat-fee structure for our bankruptcy filings. This removes the anxiety of hidden costs and lets you focus on the fresh start ahead. You've been carrying this weight alone for a long time. It's time to take a breath and put a real, legal plan in place. Reach out to our Northbrook office for a confidential chat and let's figure out your next move together.

Your Path to Lasting Financial Stability

You've seen how the 2026 changes to Illinois law have made protecting your home and car easier than ever. Choosing the right path involves more than just picking a lower interest rate; it's about finding a permanent solution that finally stops the cycle of minimum payments. Whether you decide on a structured reorganization or a total discharge, the debt consolidation vs bankruptcy pros and cons Illinois families weigh depend on their specific assets and long-term goals. A court-ordered fresh start often provides a level of security that a private loan simply cannot match.

Attorney O. Allan Fridman brings nearly 20 years of Illinois legal experience to every case, providing the personalized attention you won't find at a national loan company. We offer flat-fee bankruptcy services to ensure you have full pricing clarity from the very start. You don't have to navigate these complex regulations on your own. Schedule your free, confidential debt relief consultation today to explore your options with a local expert. You deserve to wake up without the weight of debt hanging over your head, and we're here to help you make that a reality.

Frequently Asked Questions

Is it better to consolidate debt or file for bankruptcy in Illinois?

The best choice depends entirely on your credit score and the total amount of debt you're carrying. If you have excellent credit and a manageable balance, consolidation can lower your interest rates without a court record. However, when evaluating the debt consolidation vs bankruptcy pros and cons Illinois residents face, bankruptcy is often the only way to completely wipe out overwhelming debt that a loan simply can't fix.

Will I lose my house in Illinois if I file for bankruptcy instead of consolidating?

No, you're very unlikely to lose your home in 2026 because of the generous Illinois Homestead Exemption. As of January 1, 2026, you can protect up to $50,000 in equity individually or $100,000 if you own the property jointly with a spouse. Consolidation offers no such legal protection. If you fall behind on a consolidation loan, your house could still be at risk if creditors decide to sue you.

How long does bankruptcy stay on my credit report compared to a consolidation loan?

A Chapter 7 bankruptcy stays on your report for 10 years, while Chapter 13 stays for seven. A consolidation loan stays on your report as long as the account remains open. While the 10 year mark sounds intimidating, many people see their credit scores begin to rebound within 12 to 24 months of a discharge. Consolidation keeps that debt on your back for years, which can keep your score stagnant.

Can I keep my car if I file for Chapter 7 in Illinois?

Yes, most Illinois residents can keep their primary vehicle through the 2026 motor vehicle exemption. This law protects up to $3,600 of equity in one car. If your vehicle is worth more, you can often use the $4,000 wildcard exemption to cover the remaining equity. This ensures you can continue driving to work and managing your daily life in the Chicago area while your unsecured debts are eliminated.

Does debt consolidation stop wage garnishment in the Chicago area?

No, a consolidation loan doesn't have the legal power to stop an active wage garnishment. Only a bankruptcy filing triggers the "Automatic Stay," which is a federal court order that halts all collection actions immediately. If a creditor in the Chicago area is already taking money from your paycheck, consolidation won't stop them unless they voluntarily agree to it. Bankruptcy forces them to stop the moment you file.

What is the "Means Test" and do I have to pass it to file for bankruptcy?

The Means Test is a calculation used to determine if your income is low enough to qualify for Chapter 7 bankruptcy. It compares your average monthly income to the median income for a household of your size in Illinois. If your income is above the median, it doesn't mean you're out of luck; it just means you'll likely file for Chapter 13 instead. This ensures the system is used fairly.

Can I file for bankruptcy on just some of my debts and keep others?

No, you're required by law to list every single person or company you owe money to when you file. You can't pick and choose which creditors to include. However, you can choose to "reaffirm" certain secured debts, like your car loan or mortgage. This allows you to keep the asset and continue making payments as if you hadn't filed, while still wiping out your credit cards and medical bills.

How much does it cost to hire a bankruptcy lawyer in Northbrook?

Legal fees in Northbrook vary based on the complexity of your specific case and which chapter you choose to file. While we don't provide industry average prices, many local firms prefer a flat-fee structure so you know exactly what you'll pay from the start. You should always ask what's included in that fee, such as court filing costs, to ensure you can plan your fresh start without any surprises.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.