What if the legal process you're currently avoiding is actually the most reliable way to protect your suburban family home? Many homeowners in the Chicago area feel a deep sense of unease when debt collectors begin their outreach, fearing that the bankruptcy means test illinois will somehow disqualify them from the relief they need. It's a stressful experience to face these financial pressures while trying to maintain the stability of your household and your long term assets.

I'm going to show you how to navigate these legal hurdles with a local perspective that prioritizes your property and your peace of mind. This guide provides a clear look at the 2026 standards for debt discharge, including the significant updates to state exemptions that help secure your equity. We'll preview the specific income thresholds you need to meet and the strategic steps required to stop creditor harassment immediately, giving you a professional roadmap to financial recovery.

Key Takeaways

- See how the bankruptcy means test illinois acts as a gatekeeper for Chapter 7 and what it looks for in your financial history.

- Check how the 2026 median income limits change based on your household size and what that means for your filing options.

- Compare Chapter 7 and Chapter 13 to see which path offers the best protection for your equity and your family home.

- Explore the second chance provided by the means test, where deducting your necessary living expenses can lead to a successful filing even if your income is high.

- Learn the value of having a legal expert who handles your case personally to ensure your suburban assets remain safe throughout the process.

What Exactly is the Illinois Bankruptcy Means Test and Why Does it Matter?

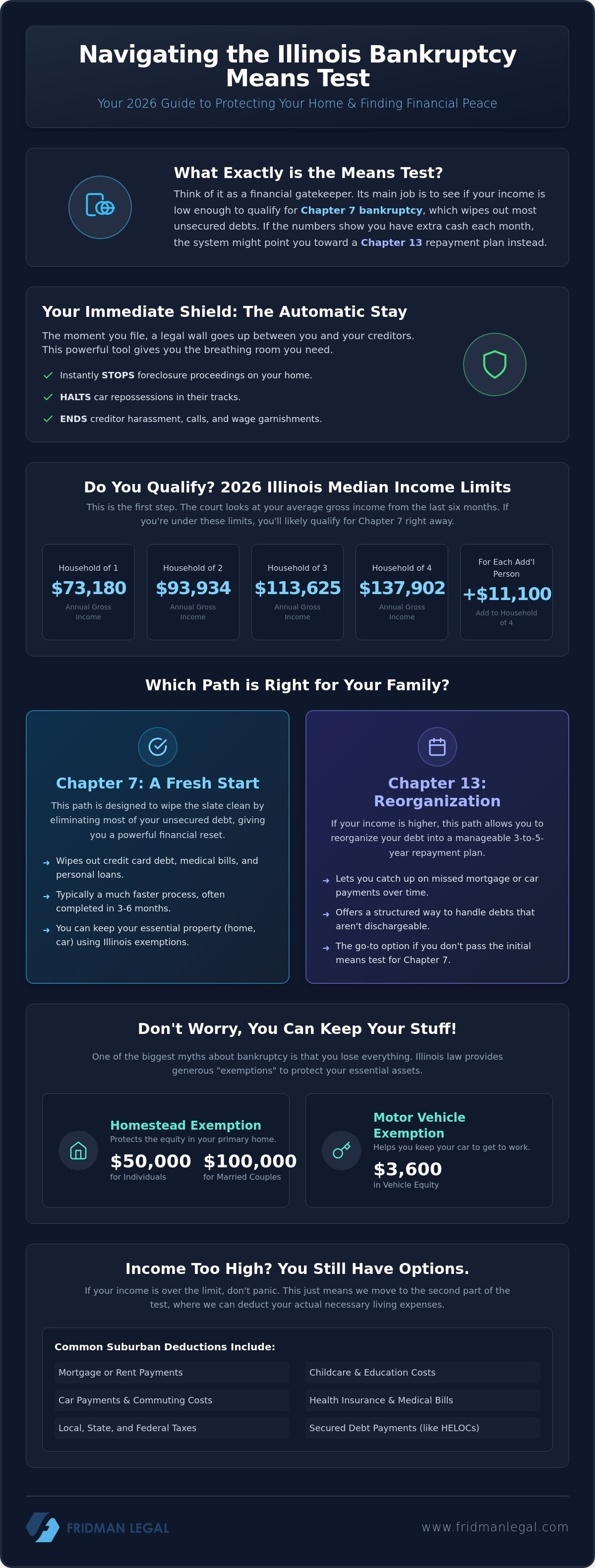

When you're facing a mountain of debt, the bankruptcy means test illinois is the first significant checkpoint on your path to relief. Think of this bankruptcy means test as a formulaic gatekeeper. Its primary purpose is to determine if your household income is low enough to qualify for a Chapter 7 discharge, which wipes out most unsecured debts. The court uses this calculation to decide if you truly lack the disposable income to pay back your creditors through a structured plan. If the numbers show you have extra cash at the end of the month, the system might steer you toward a Chapter 13 reorganization instead.

It's natural to feel some anxiety about these calculations, but you should know that most people who genuinely need to file actually pass the test. The formula isn't just about what you earn; it's also about what it costs to live. This is where a suburban perspective becomes vital. Expenses in the Chicago suburbs, from property taxes to commuting costs, are often higher than the national averages used in generic forms. A local attorney knows how to document these real world costs to ensure your Chapter 7 filing reflects your actual financial reality rather than a rigid, one size fits all spreadsheet.

The Automatic Stay: Your Immediate Shield in 2026

The moment your petition is filed, an invisible but legally binding wall goes up between you and your creditors. This is known as the automatic stay. In 2026, with the speed of digital debt collection and automated legal filings, this shield is more important than ever. It immediately halts foreclosure proceedings on your home and stops car repossessions in their tracks. It's the most direct benefit for suburban families who are currently being squeezed by aggressive debt buyers or constant collection calls. The stay applies to almost all creditors, giving you the breathing room needed to reorganize your life without the constant threat of a knock at the door or a frozen bank account.

Asset Protection for Suburban Lifestyles

There's a common myth that filing for bankruptcy means you'll have to hand over the keys to your house and your car. That simply isn't true for the vast majority of filers. Illinois law provides specific exemptions that allow you to keep your property while still getting rid of your debt. As of 2026, these protections have become even more robust. For instance, the homestead exemption now protects up to $50,000 of equity in your primary residence for individuals, or $100,000 for married couples filing together. You also have a $3,600 exemption for your motor vehicle, which helps ensure you can still get to work and take care of your family. A skilled attorney balances your need for debt relief with the strategic protection of these essential assets, ensuring you emerge from the process with your lifestyle intact.

Breaking Down the 2026 Illinois Median Income Limits

The first stage of the bankruptcy means test illinois is a direct comparison. You take your average monthly income and see how it stacks up against the state median for your household size. It's important to realize these Illinois median income limits aren't static. They change periodically based on Department of Justice updates, so 2026 filers need to be looking at the most recent figures. To calculate your average, the court uses a "six month lookback" period. This means they average your gross income from the six months leading up to your filing date. If you've had a recent drop in income or a job change, timing your filing can be a strategic move to ensure you meet the requirements.

Median Income Estimates for Cook and Lake County

While the cost of living in the Chicago suburbs is notably high, the median income threshold is set at the state level. For cases filed between April 1, 2026, and November 1, 2026, the limits are very specific. A household of one qualifies with an income up to $73,180. For a household of two, the limit is $93,934. Families of three have a threshold of $113,625, and a household of four can earn up to $137,902. If you have more than four people in your home, you can add $11,100 for each additional person. If you're under these numbers, you usually qualify for Chapter 7 immediately. If you're over, we move to the second part of the test, where your actual suburban expenses like mortgage payments and childcare are used to offset that income.

What Counts as Income in the Eyes of the Court?

The court looks at almost every dollar coming into your household. This includes your standard paycheck, any side hustle earnings, and even consistent financial help from family or friends. It's a comprehensive view of your financial life. However, there is a significant silver lining for many filers. Social Security benefits are generally excluded from the bankruptcy means test illinois calculation. This means your retirement or disability income won't count against your ability to pass the test. Correctly identifying what stays in and what stays out is a technical task. A bankruptcy lawyer in Chicago can help you categorize these funds to protect your eligibility. If you're worried your income is right on the edge, you might want to explore how a professional evaluation can clarify your options.

Chapter 7 vs. Chapter 13: Choosing the Best Path for Your Home

Deciding between Chapter 7 and Chapter 13 isn't just a matter of checking boxes on a form; it's a strategic choice about your family's future in the Chicago suburbs. While the bankruptcy means test illinois is the primary tool used to determine your eligibility for a direct discharge, your specific goals for your real estate often dictate which path is actually better for you. Both options provide the immediate relief of the automatic stay, which stops creditor harassment and legal actions the moment you file. However, the way they treat your assets and your long term financial obligations differs significantly.

Chapter 7 is designed for speed and a true "fresh start," typically concluding in just a few months. On the other hand, Chapter 13 is a reorganization that lasts between three and five years. If you're wondering What Happens if You 'Fail' the Means Test? for a Chapter 7, the answer is often a transition into Chapter 13. This isn't necessarily a bad outcome. For many suburban homeowners, Chapter 13 offers protections that a Chapter 7 simply cannot provide, especially when it comes to keeping a house that's currently in the middle of a foreclosure dispute.

Chapter 7: The Strategic Fresh Start

If your primary goal is to eliminate high interest credit card debt or overwhelming medical bills as quickly as possible, Chapter 7 is the most direct route. It's a highly efficient process that wipes out unsecured debt, giving you a clean slate in about 90 to 120 days. For residents in the northern suburbs, understanding how local property values interact with this process is key. You can find more specific details in this Chapter 7 Northbrook guide, which explains how to protect your assets while pursuing a total discharge. As long as your equity stays within the 2026 Illinois exemption limits, you can walk away from your debt without losing your property.

Chapter 13: Protecting Your Suburban Real Estate

Chapter 13 is frequently the preferred choice for homeowners who have fallen behind on their mortgage payments. This "reorganization" allows you to take your mortgage arrears and spread them out over a three to five year repayment plan. It's a powerful way to stop foreclosure in its tracks while you catch up on missed payments at a pace you can actually afford. During this time, you keep all your assets, including your home and vehicles. In many cases, you'll only pay back a small percentage of your unsecured debt, sometimes as little as pennies on the dollar, while the rest is discharged at the end of your plan. This provides a structured, court protected environment to rebuild your finances without the fear of losing your primary residence.

What Happens if You "Fail" the Means Test?

Finding out your income is above the Illinois median can feel like a setback, but it isn't the end of the road for your Chapter 7 goals. The bankruptcy means test illinois actually consists of two distinct parts. If you don't pass the first part based on gross income alone, we move to a much more detailed calculation. This second phase allows you to subtract specific "allowable expenses" from your earnings to see what your actual disposable income looks like. The court uses a combination of your real world bills and IRS National and Local Standards to determine if you truly have enough left over to pay back your creditors. If your remaining income after these deductions is below a certain threshold, you can still qualify for a total debt discharge.

The math involved here is complex. It requires a steady hand and a deep understanding of how federal standards apply to local lives. High mortgage payments or significant tax debts aren't just financial burdens; in this context, they're strategic tools that can help you pass the test. When you account for the high cost of suburban life, your disposable income often drops significantly, changing your legal outlook entirely. If you are concerned about your specific numbers, you can schedule a professional analysis to see how these deductions apply to your household.

Allowable Expenses: The Suburban Homeowner Advantage

Living in the Chicago suburbs comes with a unique set of financial realities that the court recognizes during the bankruptcy means test illinois. High housing costs in Northbrook or Chicago aren't just accepted; they are often used as valid deductions to offset your income. Beyond your mortgage, you can also deduct health insurance premiums, necessary childcare expenses, and mandatory retirement contributions required by your employer. Other common deductions include term life insurance and even certain education expenses required for your job. You should keep detailed records of all monthly expenses to ensure every possible deduction is captured during the filing process.

The Business Debt Exception

There's another critical path that many entrepreneurs in the Chicago area don't realize exists. If more than half of your total debt comes from business activities rather than personal or consumer spending, the means test might not apply to your case at all. This exception allows business owners to seek relief without the income restrictions that typically govern consumer filings. It's a powerful tool for those who have taken personal risks to support a company. While Chapter 7 is one route, many business owners also find that a Chapter 11 bankruptcy filing provides the necessary structure to reorganize while keeping their operations running.

The Fridman Legal Approach: Professional Guidance with a Human Touch

Choosing the right legal partner is often the most important decision you'll make in this entire journey. At Fridman Legal, we believe you deserve more than just a signature on a form. Many large downtown firms might pass your case off to a paralegal or a junior associate, but here, your case is handled personally from start to finish. With nearly twenty years of experience specializing in both bankruptcy and real estate law, I provide a perspective that many general practitioners simply don't have. This dual expertise is particularly valuable for suburban homeowners who need to ensure their equity is protected while they navigate the bankruptcy means test illinois.

Having a deep familiarity with the local courts in Cook and Lake County also makes a tangible difference. Every jurisdiction has its own nuances, and knowing the specific procedures of local trustees can help speed up your case and reduce unnecessary delays. If, after reviewing your finances, it turns out that a full filing isn't your best option, we can also discuss alternatives like debt settlement. Our goal is to provide a no pressure environment where you can explore every available path to relief. You deserve clarity and confidence throughout this process.

Predictable Pricing with Flat-Fee Services

One of the biggest sources of stress when hiring a lawyer is the fear of an ever growing hourly bill. We've eliminated that anxiety by offering flat fee services for our bankruptcy cases. This means you'll know exactly what your costs are before we even begin. This transparent pricing covers everything in the standard bankruptcy filing process, including the initial preparation, the actual filing, and your representation at the mandatory meeting of creditors. There aren't any hidden surprises or extra charges for standard communication; we want you to feel comfortable asking the questions you need to ask.

Your Next Steps Toward Financial Stability

It's easy to feel isolated when you're struggling with debt, but it's important to remember that you aren't alone. Thousands of people across the Chicago area file for bankruptcy every year to reclaim their financial lives and protect their families. Taking that first step can be daunting, but a simple conversation is often all it takes to start feeling in control again. We're here to help you move from a place of uncertainty to a place of stability. If you're ready to see how the bankruptcy means test illinois applies to your specific situation, please reach out to the Fridman Legal contact page to start your journey toward a more stable future.

Taking the First Step Toward Lasting Debt Relief

Securing your financial future doesn't have to be a solo effort. We've explored how the 2026 updates to state laws provide better protection for your home and why the bankruptcy means test illinois is actually a tool for relief rather than a barrier. Whether you're pursuing a fresh start through Chapter 7 or a structured reorganization in Chapter 13, the right strategy makes all the difference for your suburban lifestyle. It is about more than just numbers; it's about reclaiming your peace of mind.

I bring nearly 20 years of legal experience to every case, combining deep expertise in both bankruptcy and real estate law. This dual perspective ensures your most valuable assets are handled with precision and care. You won't have to worry about hidden costs either, as we use transparent flat fee pricing for all bankruptcy filings. This approach gives you the predictability you need during a time of transition. It's time to stop the stress of creditor calls and start building a stable foundation for your family. If you're ready to explore your options with a professional who understands the local landscape, schedule a confidential conversation with Fridman Legal today. You have a path forward, and it begins with a single conversation.

Common Questions About Debt Relief in 2026

Can I keep my house and car if I file for bankruptcy in the Chicago suburbs?

You can typically keep your primary residence and your vehicle as long as your equity stays within the state's legal limits. As of January 1, 2026, the Illinois homestead exemption protects up to $50,000 in equity for an individual or $100,000 for a married couple filing jointly. Your car is also protected by a specific motor vehicle exemption, which currently covers up to $3,600 in equity. These updated protections are designed to ensure that families can maintain their stability while they resolve their financial challenges.

How much does a bankruptcy attorney in Chicago or Northbrook cost in 2026?

The total cost involves both court filing fees and professional legal fees. In 2026, the national filing fee is $338 for Chapter 7 and $313 for Chapter 13. While professional fees vary based on the complexity of the bankruptcy means test illinois and the specific needs of your case, many local firms offer flat fee arrangements. This provides you with a predictable cost structure from the start, covering everything from the initial petition to your representation at the mandatory meeting of creditors.

Will my employer find out if I file for Chapter 7 or Chapter 13?

Most employers never learn about a bankruptcy filing unless you happen to owe the company money or you're filing for Chapter 13. In a Chapter 13 case, the court may set up a voluntary wage deduction order to help you stay on track with your repayment plan. This is treated as a routine payroll administrative task, much like a garnishment or a child support payment. In a Chapter 7 case, there's usually no reason for the court or your attorney to ever contact your workplace.

How long does the entire bankruptcy process take in Illinois?

The duration of your case depends on the type of filing you choose. A Chapter 7 case is relatively fast, typically resulting in a debt discharge within three to four months after your petition is filed. A Chapter 13 case is a longer commitment because it involves a structured repayment plan that lasts between three and five years. In both scenarios, the legal protection against your creditors begins the very moment your case is entered into the court system.

Can bankruptcy stop a wage garnishment that has already started?

Yes, filing for bankruptcy triggers an automatic stay that immediately halts almost all collection actions, including active wage garnishments. Once your attorney files the petition, the court issues an order that legally prevents creditors from taking money out of your paycheck. This protection is one of the most immediate benefits of the process, allowing you to keep your full earnings to cover your necessary suburban living expenses while your case moves forward.

What is the difference between debt settlement and filing for bankruptcy?

Debt settlement is a private negotiation where you ask creditors to accept a lump sum for less than you owe, but it doesn't offer legal protection from lawsuits or garnishments. Bankruptcy is a federal legal process that can legally discharge your debt or force a repayment plan on your creditors through the court. While settlement might seem less formal, passing the bankruptcy means test illinois provides a much more certain and legally binding path to a total financial fresh start.

Do I have to file with my spouse, or can I file for bankruptcy alone?

You have the legal right to file for bankruptcy individually, even if you are married. This is a common strategy when the majority of the debt is in only one person's name or if you want to protect the credit score of the non filing spouse. It's important to remember, however, that the court will still look at your total household income when determining your eligibility. We carefully review your specific family situation to decide if a joint or individual filing is the most strategic move for your assets.

Will I ever be able to get a credit card or a mortgage again after filing?

You can absolutely rebuild your credit and qualify for major loans after your bankruptcy case is closed. Many people see their credit scores begin to improve within the first year because they no longer have a high debt to income ratio weighing them down. While a bankruptcy remains on your credit report for several years, most lenders will consider you for a mortgage just two to three years after a successful discharge. With a disciplined approach, you can restore your financial standing quite effectively.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.