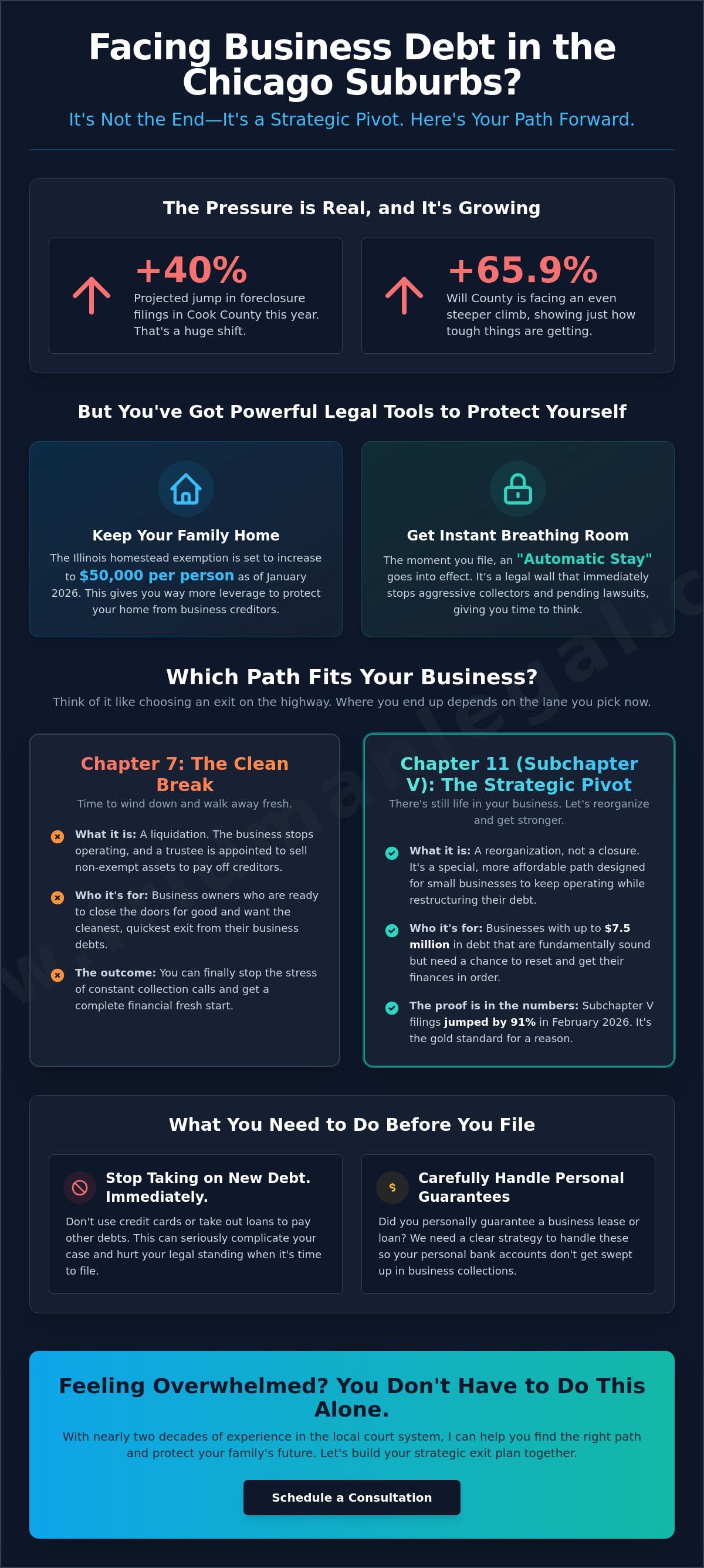

Did you know that foreclosure filings in Cook County are projected to jump by more than 40% this year, while Will County faces an even steeper 65.9% increase? If you are a business owner in the area, these numbers represent the very real pressure of mounting debt and the fear of losing everything you have built. Partnering with a Chicago Suburbs small business bankruptcy attorney is not about admitting defeat. It is a strategic move to protect your family's future. With the Illinois homestead exemption now at $50,000 per person as of January 2026, you have more leverage than ever to keep your home while addressing business liabilities.

I understand how exhausting it is to field calls from aggressive collectors while trying to decipher the difference between a Chapter 7 liquidation and a Chapter 11 Subchapter V pivot. You deserve a clear path that stops pending litigation and keeps your personal savings intact. In this guide, I will show you exactly how to navigate these options and use the new 2026 exemption limits to your advantage. We will walk through the strategic steps to either reorganize under the $7.5 million debt limit or execute a clean exit that preserves your personal assets and your peace of mind.

Key Takeaways

- Discover how the updated 2026 Illinois exemption limits can help you keep your family home and personal vehicle even if your business needs to close.

- Learn why working with a Chicago Suburbs small business bankruptcy attorney is the best way to choose between a Chapter 7 liquidation or a Chapter 11 reorganization.

- Find out why you should stop taking on any new debt immediately to protect your legal standing before you start the filing process.

- Get a clear look at how to handle personal guarantees so your private bank accounts don't get swept up in business debt collections.

- See how nearly two decades of experience in the local court system can help you pivot your business through a strategic and professional exit plan.

Understanding Small Business Bankruptcy in the Chicago Suburbs

Filing for bankruptcy in 2026 isn't a sign of failure; it's a calculated business decision. For many local owners, it's the difference between a total loss and a fresh start. Whether you're running a boutique in Northbrook or a construction firm in Cook County, the U.S. Bankruptcy Code offers specific protections designed to help you pivot. You might be looking to "wind down," which means closing the doors and walking away without debt following you home. Or, you might want to "reorganize," using new laws to keep your team employed while restructuring what you owe. Working with a chicago Suburbs small business bankruptcy attorney helps you determine which path protects your future best.

There is a lingering stigma around bankruptcy that often prevents entrepreneurs from acting until it's too late. In reality, many of the most successful Chicago business leaders have used these legal frameworks to shed unmanageable debt and launch even stronger ventures. Think of it as a financial reset button. It allows you to address the 2026 economic realities, like rising interest rates and shifting consumer habits, without losing the personal assets you've worked decades to acquire.

When is it Time to Call a Bankruptcy Attorney?

If you're waking up at 3:00 AM worrying about personal guarantees on your business lease, it's time to talk. When debt moves from something you can manage to a critical threat that prevents you from paying your staff or suppliers, you need a strategy. One of the most powerful tools a chicago Suburbs small business bankruptcy attorney provides is the automatic stay. This legal wall stops debt collectors and pending litigation immediately. It gives you the breathing room to actually think about your next move instead of just reacting to the latest demand letter or court summons.

The Unique Economic Landscape of the Chicago Suburbs

The suburbs have their own rhythm. Commercial real estate in places like Northbrook has shifted significantly recently, and local property taxes in Cook County can be a heavy burden for a small firm. A national firm won't understand how these local pressures affect your bottom line. A specialized bankruptcy lawyer in Chicago knows the local court systems and the specific economic climate of our area. They help you navigate 2026 tax changes while ensuring your filing is optimized for the local regulatory environment, giving you a distinct advantage over generic, one-size-fits-all legal advice.

Chapter 7 vs. Chapter 11: Which Path Fits Your Business?

Choosing the right legal path is like picking the right exit on the I-94; it determines where you end up and how much of your cargo you keep. If you're ready to close the doors permanently, Chapter 7 is often the cleanest break. But if there's still life in your business, Chapter 11 allows you to keep the lights on. For many of my clients, a chicago Suburbs small business bankruptcy attorney will recommend Subchapter V. It's a specialized, more affordable version of Chapter 11 designed specifically for small businesses to move through the process faster. Sole proprietors might even find that Chapter 13 is the best fit, as it allows them to reorganize personal and business debts together while protecting their home.

Chapter 7 Liquidation for Small Businesses

If your business is an LLC or a corporation, Chapter 7 means the business stops operating immediately. A trustee is appointed to sell off assets like equipment, vehicles, and furniture to pay back creditors. For sole proprietors, the process is different because the law doesn't see a separate business entity; your business and personal debts are handled in one case. In Illinois, a Chapter 7 filing typically requires the trustee to take possession of and sell all non-exempt business inventory to satisfy outstanding creditor claims. It's a final step, but it's one that can stop the stress of constant collection calls.

Subchapter V: The Small Business Reorganization Act

This is the gold standard for reorganization in 2026. Traditional Chapter 11 can be expensive, with a filing fee of $1,738 and high legal costs. Subchapter V is different. In February 2026 alone, filings for this path jumped by 91% compared to the previous year. As of March 2026, the debt limit is permanently set at $7.5 million. This makes it accessible to almost any suburban firm. You stay in control of the daily operations. A trustee acts more like a mediator, helping you build a plan that creditors will actually accept. It's a much more collaborative approach than the traditional adversarial court battle. You can read more about Chapter 11 Bankruptcy Basics to see how it usually works, but Subchapter V is the more streamlined choice for most. If you aren't sure which path fits your specific situation, you can explore strategic bankruptcy options to find the right strategy for your firm.

Protecting Your Personal Assets During a Business Filing

The most common question I hear from business owners is simple: "Will I lose my house?" It is a heavy, valid concern. When you poured your life savings into your venture, you probably didn't imagine a scenario where your personal residence or retirement accounts would be at risk. While a corporation or LLC is designed to act as a shield, that "corporate veil" isn't always bulletproof. If you have commingled funds or failed to follow corporate formalities, creditors might try to "pierce the veil" to reach your personal bank accounts. This is why having a chicago Suburbs small business bankruptcy attorney on your side is vital to ensure your legal boundaries remain intact.

Personal guarantees are the most frequent way suburban owners find themselves personally liable. Most commercial landlords in Northbrook and lenders across Cook County require these guarantees before they'll even hand over the keys. When the business can't pay, these contracts allow creditors to bypass the business entity and come after you directly. Bankruptcy is often the only tool powerful enough to discharge these personal obligations. By understanding Chapter 11 Bankruptcy Basics and how they apply to your specific guarantees, you can build a strategy that protects your private wealth while the business debt is resolved.

The Illinois Homestead Exemption and Your Business

As of January 1, 2026, Illinois law has become significantly more protective of homeowners. The homestead exemption has increased to $50,000 for an individual and $100,000 for married couples filing jointly. This means a significant amount of equity in your home is shielded from creditors during a filing. If you're a business owner in the Chicago suburbs, these new limits provide a much larger safety net than we saw in previous years. For a deeper look at how this works in practice, you can review our detailed guide on Chapter 7 bankruptcy in Illinois, which breaks down asset protection for suburban residents.

Addressing EIDL and SBA Loan Defaults

In 2026, many businesses are still grappling with pandemic-era debt. SBA and EIDL loans often carry personal liability if the loan amount was over a certain threshold. If you've received a demand letter from the SBA, do not ignore it. Federal debt is aggressive, but it can be restructured or even discharged through the right bankruptcy chapter. A chicago Suburbs small business bankruptcy attorney can help you negotiate these federal claims, often allowing you to settle for a fraction of the total or incorporate the payments into a manageable reorganization plan that keeps your personal assets out of the government's reach.

Steps to Take Before You File for Bankruptcy

Before you walk into a courtroom, you have to get your house in order. The weeks leading up to a filing are just as important as the filing itself. The first rule is to stop the bleeding. It’s incredibly tempting to take out one last "bridge loan" or use a personal credit card to cover a business expense, but this is a major mistake. Taking on new debt when you know you can't pay it back can lead to allegations of fraud in bankruptcy court. It’s better to pause, preserve what cash you have, and consult with a chicago Suburbs small business bankruptcy attorney to map out a timeline that won't jeopardize your case.

Next, you need to think about communication. You don't need to shout your plans from the rooftops, but you do need a strategy for your employees, vendors, and your landlord. If you plan to reorganize, these people are your future partners. Keeping them in the loop at the right time helps maintain the trust you'll need to keep the doors open. A pre-filing consultation is the best time to decide exactly what to say and when to say it so you don't spark unnecessary panic.

Organizing Your Business Finances

Transparency is the only way this process works effectively. You'll need a comprehensive list of everyone you owe money to, from the big banks down to the local supply shop in Northbrook. Your attorney will need to see your tax returns and profit and loss statements for at least the last two years to build an accurate picture of your financial health. You must ensure that your personal and business bank accounts are entirely separate before filing to prevent the court from viewing your private assets as part of the business estate. Having these documents ready on day one saves time and helps your legal team move quickly.

Choosing Your Legal Team

Not all bankruptcy lawyers are the same. You need someone who understands a Chapter 11 bankruptcy filing and the nuances of the local Cook County courts. During your first meeting, ask how many Subchapter V cases they've handled recently. You should also be clear on how they bill. Some firms use flat fees for certain parts of a business filing, while others stick to hourly rates. Understanding the cost upfront helps you budget for the transition without surprises. If you're ready to start this process with a clear strategy, you can reach out to our team today to schedule your initial consultation.

Why Fridman Legal is the Right Partner for Your Business Pivot

When your business is facing a financial crisis, the last thing you need is to be handed off to a junior associate who is still learning the ropes of the Cook County court system. At Fridman Legal, you get the direct, personalized attention of O. Allan Fridman. We believe that a business pivot as significant as bankruptcy requires the steady hand of an experienced strategist. Finding the right chicago Suburbs small business bankruptcy attorney means looking for someone who sees you as a partner, not just another case number on a crowded docket. We take the time to strip away the complex legal jargon so you can make informed decisions about your company's future without feeling overwhelmed by the process.

With nearly twenty years of experience practicing in the Chicago and suburban court systems, we have seen almost every possible scenario. We know the local trustees, the judges, and the tactics that aggressive creditors often use to pressure suburban business owners. This deep local knowledge allows us to anticipate hurdles before they become roadblocks. Our approach is strictly results-driven. We aren't here to bill hours; we are here to provide a practical solution that protects your personal assets and gives your business the best possible chance at a successful reorganization or a dignified exit.

A Local Perspective on Global Financial Problems

Our roots are firmly planted in Northbrook and the surrounding Chicago suburbs. We understand that the economic pressures facing a local storefront or a suburban construction firm are unique. Because we also specialize in civil litigation, we are uniquely prepared to handle contested bankruptcy cases where creditors might try to challenge your filing or your exemptions. This litigation background gives us a sharp edge in negotiations. We don't just fill out forms; we advocate for your interests to ensure you find the stability and clear path forward that you deserve.

Ready to Take the Next Step?

Taking the first step toward debt relief is often the hardest part of the journey. When you visit our Northbrook office, you can expect a professional, confidential environment where your concerns are heard and your privacy is respected. During your first visit, we will review your financial records, discuss your goals, and begin mapping out a specific legal strategy tailored to your industry. There is no guesswork involved, just clear, actionable advice from a seasoned professional. If you are tired of the constant stress and ready to regain control, contact Fridman Legal today to discuss your business debt relief options with a dedicated chicago Suburbs small business bankruptcy attorney.

Take Control of Your Business Future Today

Navigating financial distress is one of the most difficult challenges any entrepreneur can face, but it doesn't have to be the end of your professional story. We've explored how a strategic filing can stop aggressive collection efforts and how the 2026 Illinois exemptions provide a robust shield for your family home and personal savings. Whether you're looking for a clean break through Chapter 7 or a streamlined reorganization under Subchapter V, the right plan can turn a crisis into a manageable transition.

With nearly 20 years of Illinois legal experience, our Northbrook based firm has the expertise in both Chapter 7 and Chapter 11 Subchapter V to guide you through these complex choices. You don't have to deal with SBA defaults or personal guarantees on your own. Working with a chicago Suburbs small business bankruptcy attorney gives you the expert guidance you need to protect what you've worked so hard to build. Let's get you back to a place of financial stability. If you're ready to see what's possible, schedule a confidential consultation with Fridman Legal. You've put everything into your business; now it's time to protect your future.

Frequently Asked Questions

Can I keep my business open while filing for bankruptcy in Illinois?

Yes, you can keep your business operating if you choose a reorganization path like Chapter 11 Subchapter V. This specific chapter was designed to allow small business owners to maintain control of their daily operations while restructuring their debts into a manageable three to five year payment plan. It is a strategic way to find stability without shutting your doors.

If you choose to file for Chapter 7, the situation is different. Under Chapter 7, the business must stop all operations immediately so a court appointed trustee can sell off assets to pay back your creditors. Choosing the right path depends on whether you believe the business is still viable once the debt load is reduced.

Will filing for business bankruptcy ruin my personal credit score forever?

Filing for bankruptcy will cause an immediate drop in your credit score, but the impact is not permanent. Most people find that their scores begin to recover significantly within 12 to 24 months as they rebuild their financial history. In many cases, a bankruptcy filing is actually less damaging than years of missed payments, collections, and court judgments.

It's also important to remember that if your business is a separate legal entity and you didn't sign personal guarantees, the filing might not appear on your personal credit report at all. However, most small business owners in the suburbs do have personal liability, making it vital to plan for a personal credit recovery strategy alongside the business filing.

What is the difference between Chapter 7 and Chapter 11 Subchapter V?

Chapter 7 is a liquidation process intended for businesses that are ready to close their doors and walk away with a clean slate. A trustee takes over the business assets and sells them to pay creditors. A chicago Suburbs small business bankruptcy attorney often recommends this when the business model is no longer sustainable or the owner is ready to retire.

Subchapter V is a streamlined version of Chapter 11 meant for small businesses that want to stay in business. It is faster and much less expensive than a traditional corporate reorganization. It allows you to keep your equipment and keep serving your customers while you pay off a portion of your debt over time based on what the business can actually afford.

Do I have to go to court in person for a small business bankruptcy in Cook County?

Most bankruptcy proceedings in the Northern District of Illinois are currently conducted remotely via Zoom or telephone, meaning you likely won't have to visit a physical courthouse. This includes the mandatory "Meeting of Creditors," where you answer questions from the trustee about your financial affairs. While it's a formal legal proceeding, it's often handled from the comfort of your attorney's office.

There are rare occasions where a judge might require an in person appearance for a contested hearing or a trial. Your legal team will manage all the scheduling and ensure you are fully prepared for any virtual or physical appearances required by the court. Remote hearings have made the process much more efficient for busy suburban business owners.

Can bankruptcy stop a landlord from evicting my business in the Chicago suburbs?

Bankruptcy triggers an automatic stay that immediately halts all collection actions, including pending eviction lawsuits. This provides a temporary window of relief where the landlord cannot legally remove you from the property. It gives you the necessary breathing room to decide if the lease is worth keeping as part of your reorganization plan.

To stay in the space long term, you will eventually have to "assume" the lease. This requires you to prove to the court that you can pay future rent and that you have a plan to catch up on any past due amounts. If the lease is too expensive, bankruptcy also allows you to "reject" the lease and walk away from the remaining balance without the landlord suing you personally.

What happens to my employees if I file for Chapter 7 bankruptcy?

In a Chapter 7 filing, the business closes and all employees are unfortunately laid off because the company ceases to exist. However, the bankruptcy code provides some protection for your staff. Unpaid wages, commissions, or vacation pay earned within 180 days before the filing are considered "priority claims" up to a certain dollar limit per employee.

This means your employees are often among the first in line to receive payment once the trustee liquidates the business assets. It is a difficult transition, but handled correctly, it ensures that your team has the best possible chance of recovering the money they are owed. If you plan to keep your staff, a Chapter 11 reorganization is the better path.

How much does it cost to hire a small business bankruptcy attorney?

The cost of hiring a chicago Suburbs small business bankruptcy attorney varies based on the complexity of your debt and which chapter you file. You should also budget for the federal filing fees, which are $338 for Chapter 7 and $1,738 for Chapter 11. Most attorneys will require a retainer upfront to cover the initial filing and the first phase of the case.

For a Chapter 11 Subchapter V case, the legal fees are often higher because the process involves creating a detailed reorganization plan and negotiating with creditors over several months. However, the goal is to save the business, which often outweighs the initial legal investment. It is best to discuss a clear fee structure during your initial consultation so there are no surprises.

Can I discharge taxes owed by my business through bankruptcy?

You can discharge some older income taxes if they meet specific "look back" rules, such as being at least three years old and having been filed correctly. If the taxes are recent or if you failed to file the returns on time, they generally cannot be wiped out. Bankruptcy can, however, provide a way to pay these non-dischargeable taxes over several years without further penalties.

It is critical to know that "trust fund" taxes, like the payroll taxes you withheld from employee paychecks, are almost never dischargeable. The government views this money as belonging to the employees, not the business. If you are facing a massive payroll tax debt, you will need a specific strategy to handle those payments while discharging other types of business debt.

Article by

O. Allan Fridman

O. Allan Fridman has been practicing law since 2001. His practice is unique in that he does not view himself as a litigation attorney or transactional attorney. Rather, he views each area of law as a tool to pursue the best results for his clients. By practicing in both areas of law, he is able to take a 360-degree view of law. This enables the firm to catch potential drawbacks that are readily identifiable.

By practicing in litigation and transactional law and taking a holistic approach in dealing with our clients, he doesn’t put clients in box — rather, as we are all individuals, so too are the legal services we may require.

Whether it is bankruptcy or litigation or transactional, each client brings challenges and does not fit in any one box. Often times, bankruptcy clients end up not filing bankruptcy because we can achieve a better result through litigation or through an out-of-court resolution with the lender, or through a real estate sale. On the other end of the spectrum, a litigation client with multiple issues and lawsuit may fare better in a bankruptcy.

Since 2001, Allan has practiced in states and federal court, and he is a member of the trial bar of the Northern District of Illinois and admitted in the Northern District of Indiana.

We are a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code

The materials on this site are for informational purposes only and do not constitute legal advice. Viewing this site or contacting us does not create an attorney–client relationship, and you should not act or refrain from acting based on any information here without seeking professional legal counsel.